Altimmune ($ALT): Best-in-Class Tolerability, One Real Fibrosis Question, and a Serious-Liver-Disease Franchise the Market Is Pricing at Almost Nothing

Disclosure: I hold a bullish position in Altimmune (ALT) through call options expiring January 2027 — a leveraged, directional position that profits if the stock rises. Assume that gives me a financial interest in a favorable outcome and weigh this analysis accordingly. My positions may change at any time without notice. This is my own opinion and analysis, not investment advice; BiostockInfo is a research platform, not an advisory service, and nothing here is a recommendation to buy or sell any security. I don't fabricate numbers — every figure comes from company filings, Altimmune's May 2026 corporate presentation, peer-reviewed literature, or dated news sources.

Here is the contradiction that makes Altimmune worth writing about.

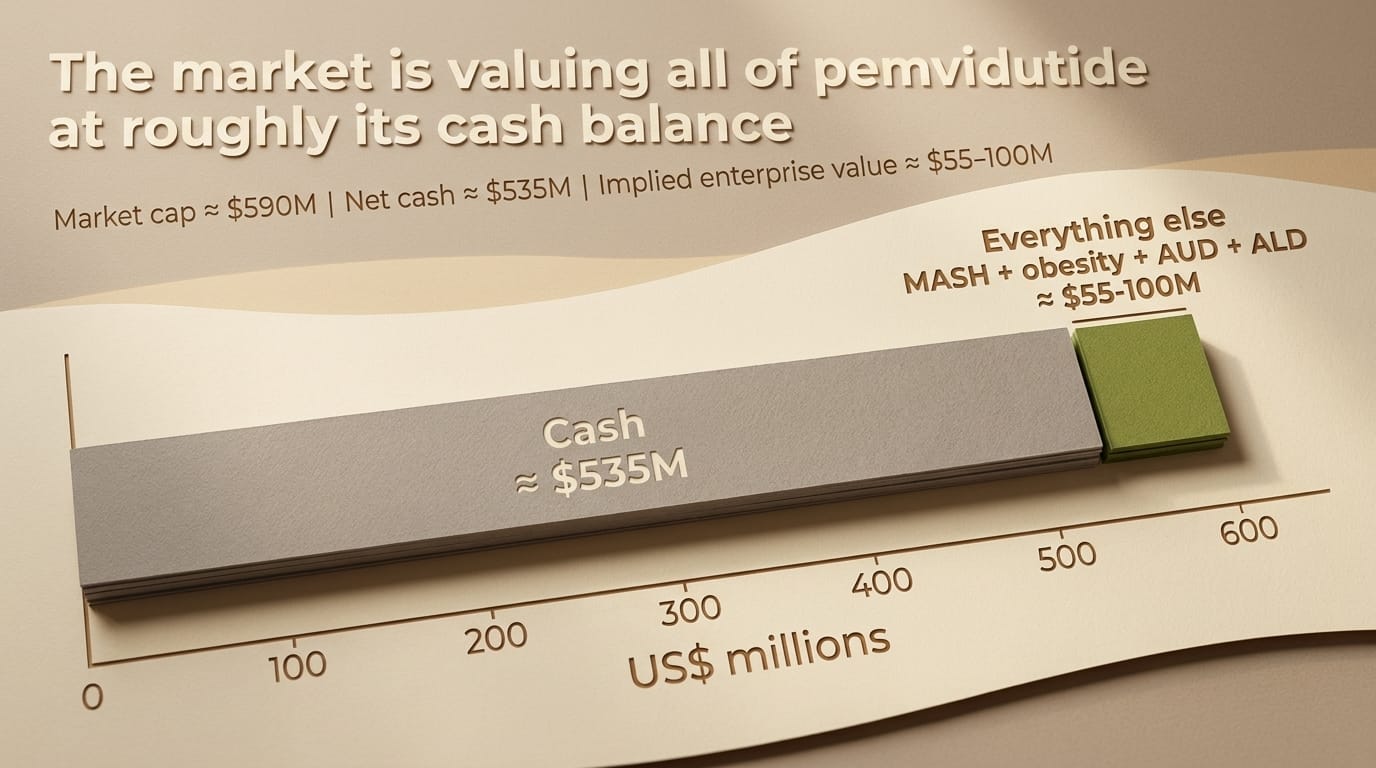

On tolerability, body composition, liver-fat clearance, and MASH resolution, pemvidutide is arguably the most complete metabolic drug in the mid-cap liver space. It puts up a ~1% treatment-discontinuation rate in a disease where its closest mechanistic rival sheds one in five patients to nausea and vomiting. And yet the stock has fallen from a 52-week high of $6.44 to roughly $3, and now trades so close to its cash balance that the market is effectively saying pemvidutide — across MASH, obesity, alcohol use disorder, and alcohol-associated liver disease — is worth almost nothing.

That gap is either a mispricing or a verdict. The whole article is about deciding which. The short version: the market has one legitimate reason to be nervous, and it has extrapolated that one reason into a valuation that ignores three genuinely differentiated assets. I'll try to make the bull case earn itself, because the bear case here is real and deserves a full hearing.

What pemvidutide actually is, and why the mechanism matters

If you already know GLP-1 biology, skip ahead. If you don't, this is the part that makes the rest legible.

Every blockbuster weight-loss drug you've heard of — Wegovy, Zepbound — works primarily through GLP-1, a gut hormone that tells your brain you're full and slows how fast your stomach empties. You eat less, you lose weight. Simple, powerful, and now a $150-billion-plus market. But GLP-1 alone does very little directly to the liver. It helps the liver by making you thinner; it doesn't reach in and clean house.

Pemvidutide adds a second lever: glucagon. Most people know glucagon as the hormone that raises blood sugar, which sounds like the last thing you'd want in a metabolic drug. But glucagon receptors are packed into liver cells, and when you activate them, the liver starts burning its own stored fat, stops manufacturing new fat, and raises the body's overall energy expenditure. In plain terms: GLP-1 is the "eat less" lever (mimicking diet), and glucagon is the "burn more" lever (mimicking exercise). Pemvidutide fires both at a deliberate 1:1 balance.

The catch with glucagon drugs has always been toxicity — unmanaged glucagon makes people violently nauseous, and rival programs have had to titrate doses slowly over months to keep patients on the drug. Altimmune's answer is a piece of molecular engineering it calls the EuPort domain. Think of it as a slow-release valve: instead of the drug spiking into the bloodstream right after injection (the spike is what triggers the nausea), EuPort flattens the peak so the drug enters gently. The practical payoff, which the clinical data confirms, is that pemvidutide can be started at a real therapeutic dose with little or no titration, and patients stay on it. In a chronic, mostly symptom-free disease, staying on the drug is not a footnote — it is the entire commercial game.

The valuation is the hook, so let's put it up front

At roughly $3 per share and approximately 190 million fully diluted shares (including the pre-funded warrants from the April raise), ALT's market capitalization is about $590 million. Against that sits ~$535 million in cash, cash equivalents, and short-term investments as of April 30, 2026, with essentially no debt.

Do the subtraction. The market is assigning somewhere in the range of $55–100 million of enterprise value to the entire pemvidutide franchise. On a narrower share count, the stock has at times traded below its net cash per share. Either way, the signal is the same: after the Phase 2b MASH data, investors marked this company down to its bank account.

Why? Because of one number I'll get to in the next section. The stock did not fall because pemvidutide failed. It fell because pemvidutide missed statistical significance on the single endpoint the entire MASH field has decided is the one that counts. Understanding whether that miss is fatal or fixable is the whole investment.

For context on how unusual this valuation is: Viking Therapeutics (VKTX), a fellow metabolic developer, carries a market cap around $4.35 billion. Madrigal (MDGL), with an approved MASH drug, sits above $11 billion. And in the last 18 months, Big Pharma paid up to $5.2 billion (Novo/Akero), up to $3.5 billion (Roche/89bio), and ~$1.2–2 billion (GSK/Boston Pharmaceuticals) to buy pre-approval MASH assets. Altimmune's entire enterprise value is a rounding error against any of those. Cheap, though, is not the same as wrong — and I'll spend real time on why it might be cheap for a reason.

The IMPACT Phase 2b data, told honestly

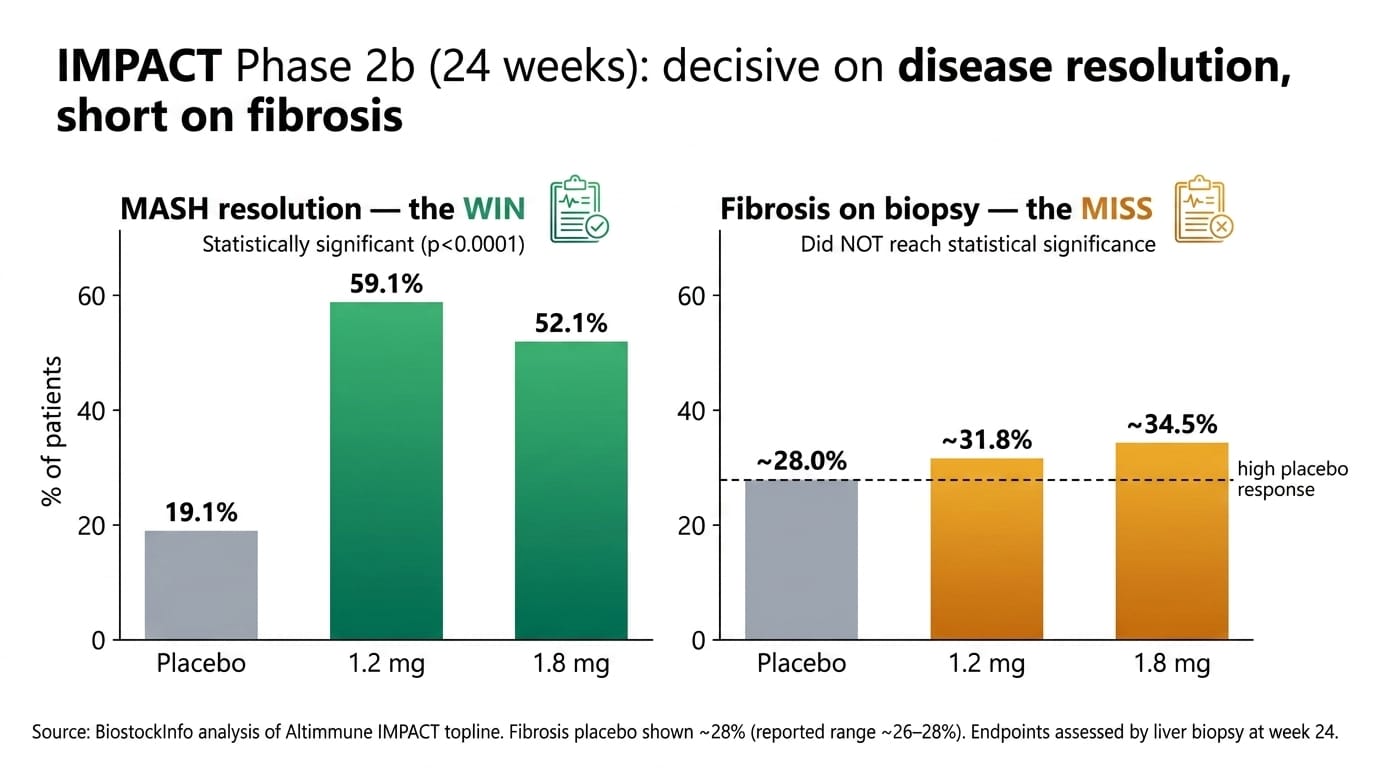

IMPACT enrolled 212 patients with biopsy-confirmed MASH and moderate-to-advanced fibrosis (stages F2–F3), dosing weekly at 1.2 mg or 1.8 mg versus placebo, with no dose titration — an aggressive design choice that stress-tested tolerability. Here is what it produced.

The win: disease resolution. MASH "resolution without worsening of fibrosis" — meaning the active inflammation clears without the scarring getting worse — hit 59.1% at 1.2 mg and 52.1% at 1.8 mg, versus 19.1% on placebo (p<0.0001). That is a decisive, unambiguous result. On the core question of "does this drug quiet the disease," the answer is yes.

The miss, and I'm not going to soft-pedal it. MASH regulators care about two things: resolving the inflammation and improving fibrosis — the scar tissue that actually predicts whether a patient progresses to cirrhosis, liver failure, or cancer. On the biopsy-read fibrosis-improvement endpoint at 24 weeks, pemvidutide posted roughly 32–35% across dose arms against an unusually high ~26–28% placebo response — and did not reach statistical significance. That is the number that broke the stock. In a field where every approved or Phase 3 rival has cleared the fibrosis bar, a fibrosis miss reads as disqualifying.

So the honest question is: was that a drug problem or a trial problem? Three things argue for "trial problem," and one argues for "don't kid yourself."

Arguing for artifact: First, timing. Fibrosis — physical scar tissue — regresses slowly. Twenty-four weeks is early to biopsy for it; resolution shows up first, fibrosis reversal lags. Second, the placebo arm was anomalously high (~28% versus the 14–22% seen in comparable trials), which mechanically crushes the drug-versus-placebo gap regardless of how well the drug worked. Third — and this is the strongest point — the non-invasive markers tell a different story than the single biopsy read.

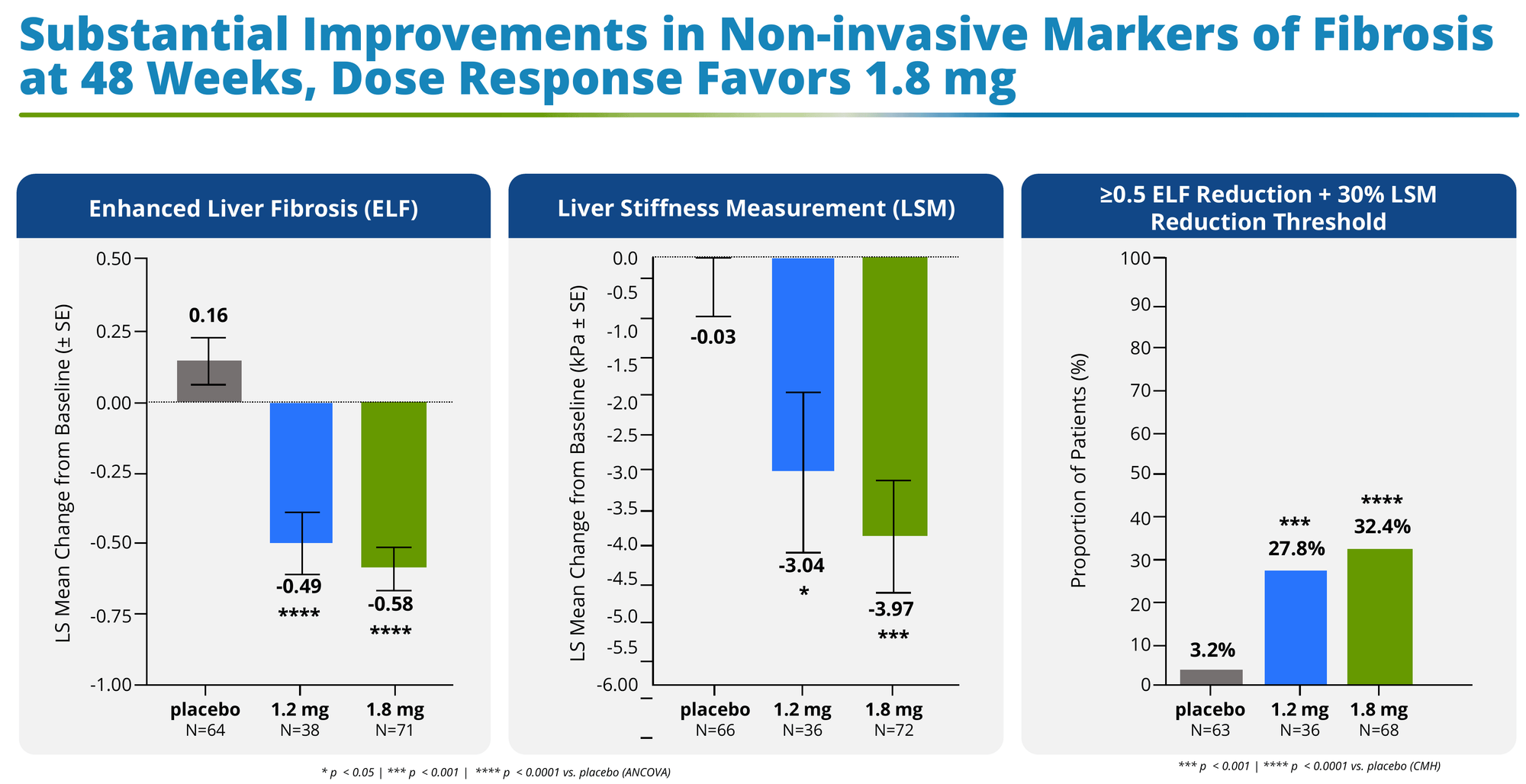

By week 48, the non-invasive tests (NITs) separated cleanly and significantly from placebo:

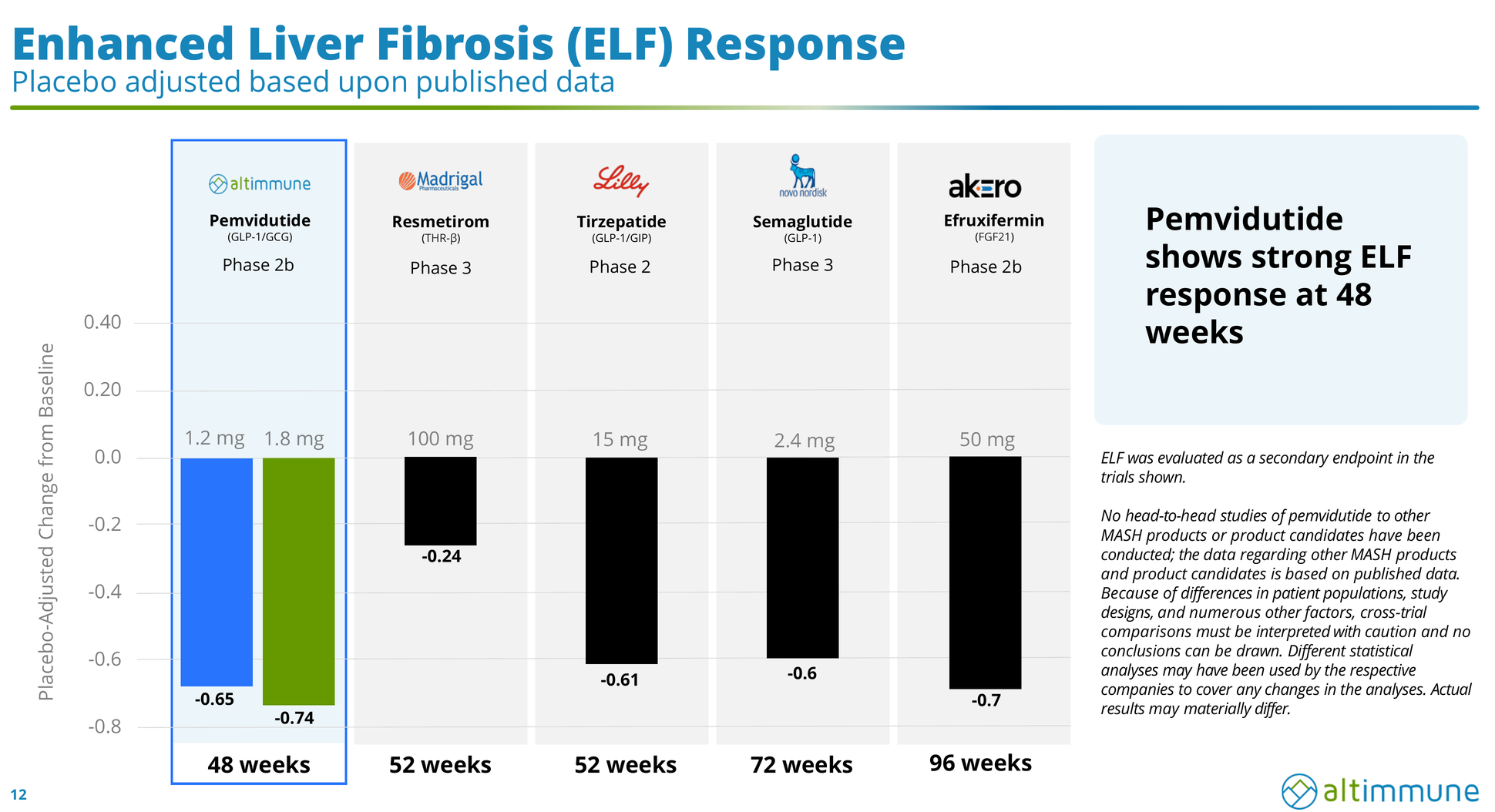

- Enhanced Liver Fibrosis (ELF) — a blood panel of scarring proteins. Placebo worsened (+0.16); the 1.8 mg arm improved by –0.58 (p<0.0001), a placebo-adjusted –0.74.

- Liver Stiffness (FibroScan/LSM) — literally how stiff the liver is, in kilopascals; stiffer means more scarring. Placebo barely moved (–0.03 kPa); the 1.8 mg arm dropped –3.97 kPa (placebo-adjusted –3.94).

- A composite responder threshold (≥0.5 ELF reduction and ≥30% LSM reduction) was hit by 32.4% at 1.8 mg versus 3.2% on placebo — a tenfold separation.

- Liver fat fell 54.7% at 1.8 mg (vs. 8.2% placebo); ALT, the classic liver-inflammation enzyme, normalized (≤30 IU/L) in 72% of patients versus 40% on placebo; and cT1, an MRI marker of liver inflammation, improved well past the threshold associated with meaningful histological gains.

Put simply: five different orthogonal measures of "is the liver getting better" all moved hard in the drug's favor, dose-dependently. That is not what a failed drug looks like. The 24-week data were strong enough to be published in The Lancet.

Arguing for "don't kid yourself": NITs are not the FDA's approval endpoint. Biopsy is. Every incretin that has passed a Phase 3 fibrosis test — semaglutide, tirzepatide, survodutide — did it on histology. "The placebo was high" and "the NITs looked great" are exactly the arguments failed MASH programs have made for two decades. The Phase 3, PERFORMA, is a genuine binary, and the base rate for MASH histology is humbling.

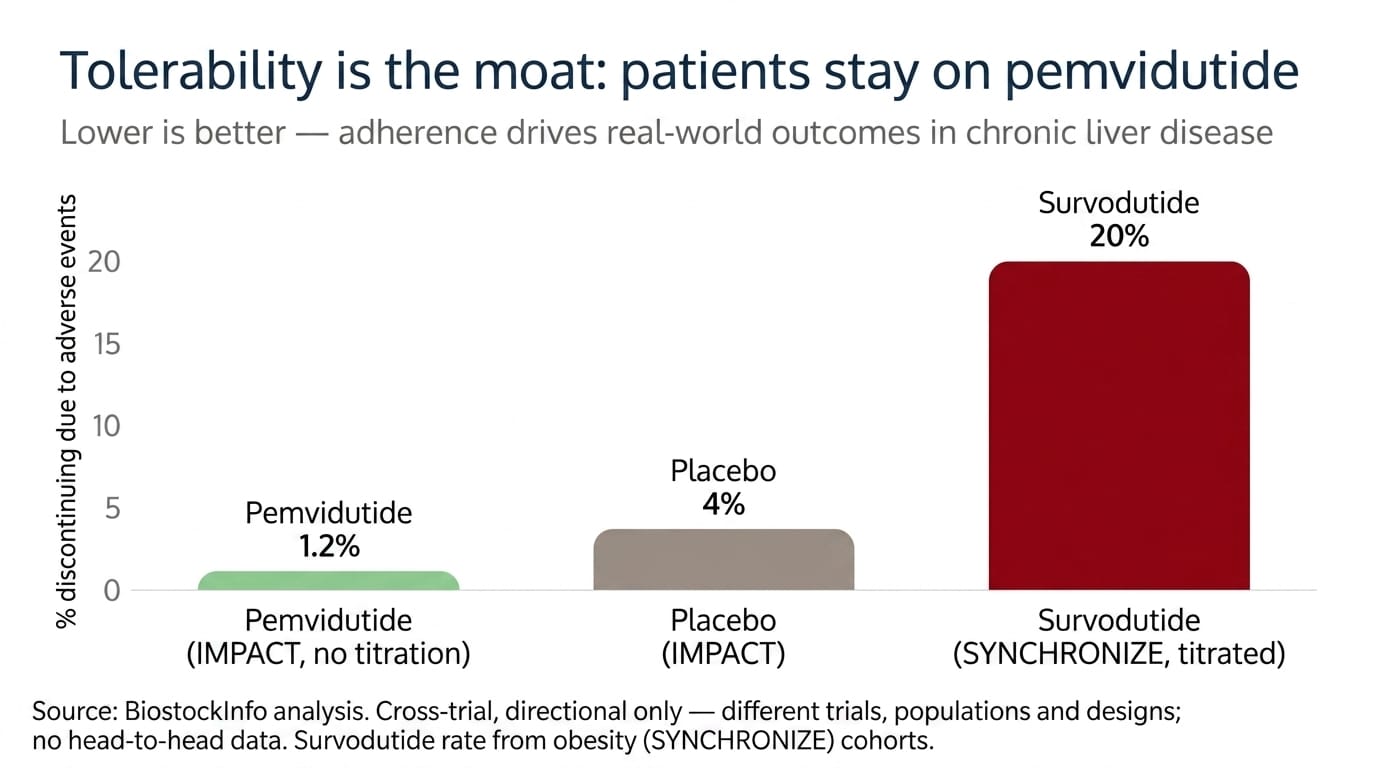

The tolerability, which is the part rivals can't match. At 48 weeks, treatment discontinuation due to adverse events was 0% at 1.2 mg and 1.2% at 1.8 mg — versus 3.5% on placebo. Read that again: fewer patients quit the drug than quit the sugar-pill. Yes, nausea occurred (41% at the higher, un-titrated dose), but it was mild-to-moderate, front-loaded to the first month, and — critically — zero serious or severe adverse events were related to study drug across all arms, with no heart-rate signal and no loss of glycemic control. This is the profile of a drug people will actually take for years.

PERFORMA: the Phase 3 is designed to fix exactly what broke

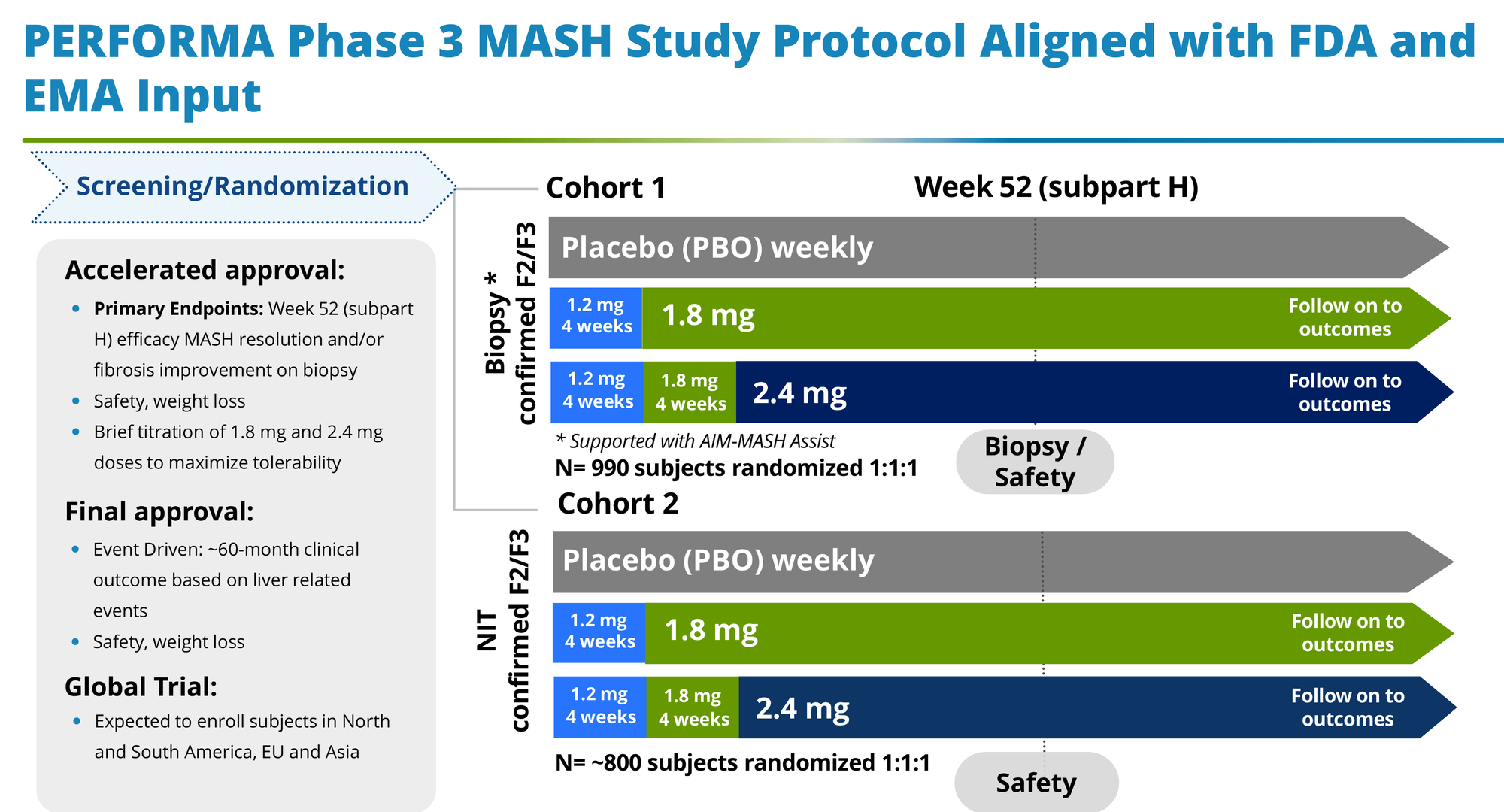

Management didn't ignore the fibrosis miss; they engineered around it. PERFORMA, starting in the second half of 2026, changes four things that matter:

- It biopsies at 52 weeks, not 24 — giving fibrosis the time it needs to show up on histology.

- It adds a 2.4 mg dose (titrated up through 1.2 and 1.8 mg), pushing for more efficacy where the Phase 2 curve never plateaued.

- It uses AIM-MASH AI-assisted digital pathology, which standardizes how pathologists read biopsies and is specifically meant to suppress the reader-to-reader noise and inflated placebo responses that plagued the Phase 2.

- It runs two cohorts — a biopsy-confirmed arm (N≈990) and a larger NIT-confirmed arm (N≈800) — hedging the histology risk with the non-invasive data that already look strong.

Whether that's enough is the 2029 question. But it's a coherent response, backed by FDA Fast Track and Breakthrough Therapy designations and alignment with both the FDA and EMA. The design is on an accelerated-approval path (biopsy at 52 weeks) with full approval tied to a longer outcomes readout.

The competitive landscape: where ALT wins, where it doesn't

MASH is now the most crowded liver market in biotech, and the honest framing is that it's bifurcating into two paradigms — which is good news for a differentiated player and bad news for a me-too.

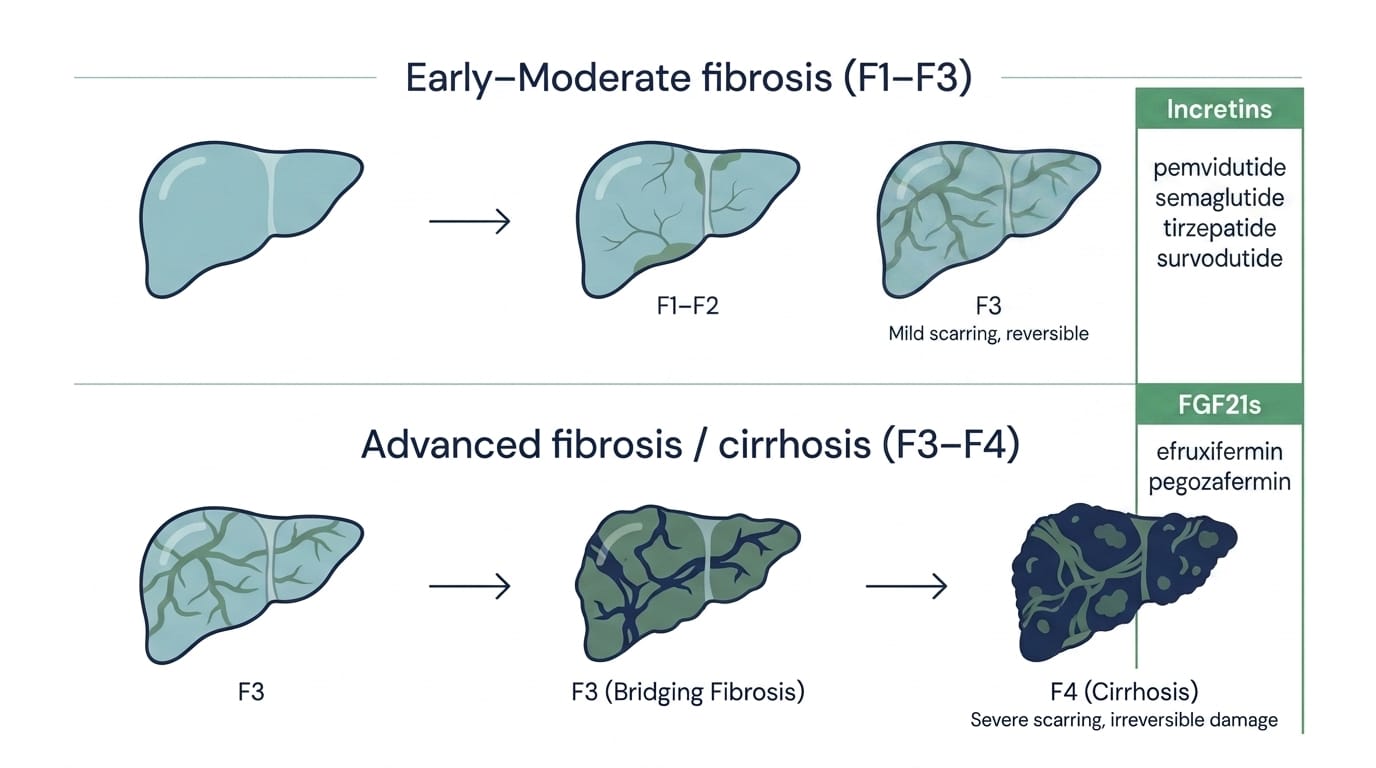

Paradigm 1 — early-to-moderate disease (F1–F3): the metabolic backbone. Here, systemic drugs that fix the upstream drivers (obesity, insulin resistance, bad lipids) do the work. This is incretin territory.

Paradigm 2 — advanced disease (F3–F4): the anti-fibrotic salvage. Once scarring is entrenched, metabolic correction is too slow, and you need drugs that dismantle scar tissue directly. This is FGF21 territory.

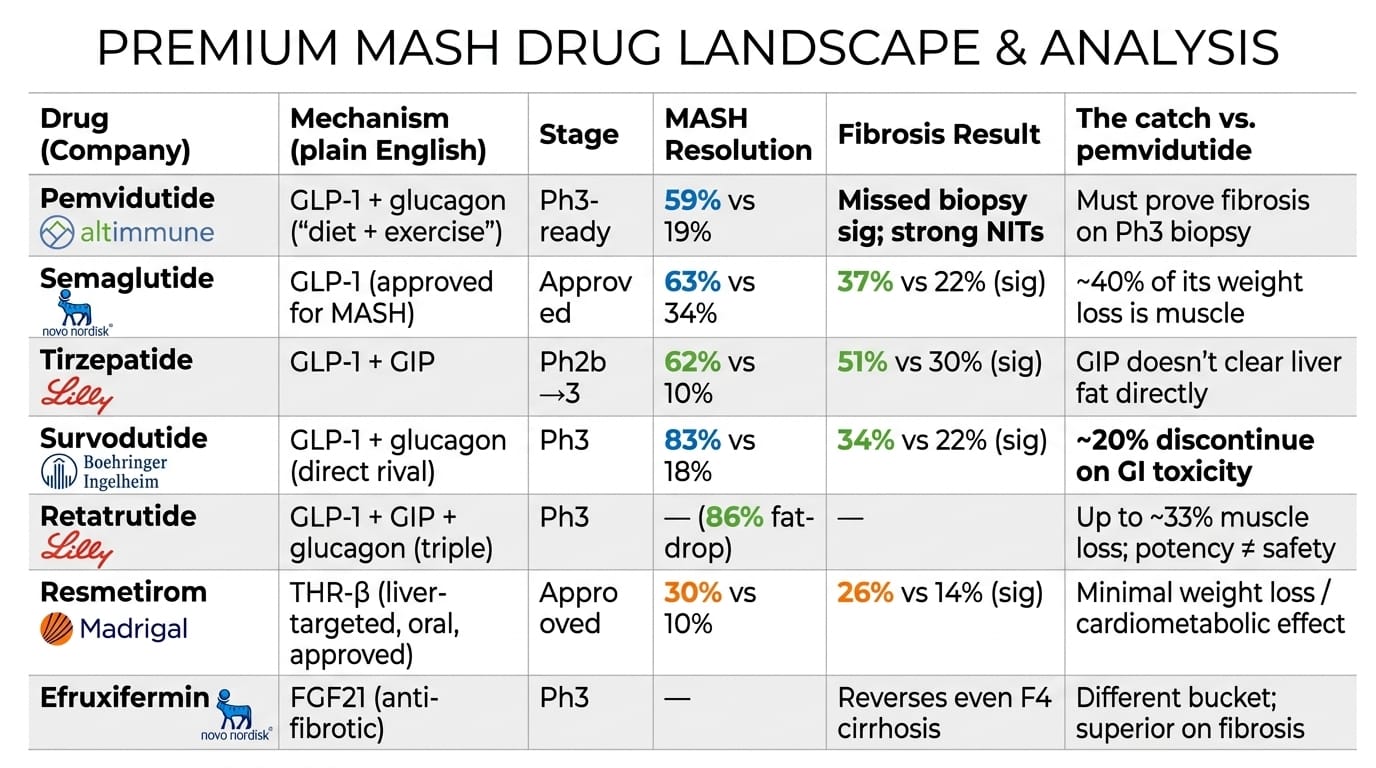

Pemvidutide competes squarely in Paradigm 1. Here's the field:

Where pemvidutide genuinely wins. Against survodutide — the drug with the identical GLP-1/glucagon mechanism — pemvidutide's advantage is stark. Survodutide posts eye-popping efficacy (83% resolution) but sheds ~20% of patients to gastrointestinal toxicity despite rigid titration; that attrition has repeatedly hurt its sponsors' valuation. Pemvidutide gets comparable-caliber liver effects at ~1% discontinuation with no titration. In the real world, a drug that keeps patients on treatment accrues more cumulative benefit than a stronger drug that patients abandon. Against the pure GLP-1s and GLP-1/GIPs, pemvidutide adds two things they structurally can't: direct glucagon-driven liver-fat burning, and class-leading lean-mass preservation (~75–78% of weight lost is fat, versus ~40% muscle loss on semaglutide and up to ~33% on retatrutide). As the field wakes up to drug-induced muscle wasting — a real danger in older, frailer liver patients — that becomes a commercial asset.

Where pemvidutide loses, and this is the uncomfortable part. Every dollar of that $11-billion-plus in recent MASH M&A went to FGF21 anti-fibrotic assets — Akero, 89bio, Boston Pharma. Big Pharma spent a fortune buying the exact mechanism where pemvidutide is weakest: direct, provable fibrosis reversal. So the lazy bull argument — "ALT is absurdly cheap next to a $5.2 billion Akero" — is a trap. Those were fibrosis specialists. Pemvidutide is a metabolic drug that still has to prove its fibrosis credentials on biopsy. The right way to use those comps is narrower: they prove the market is enormous and strategics are paying up, not that ALT deserves an Akero multiple today.

On the horizon, the field also gets orforglipron (Lilly's oral GLP-1 pill, no injection), which could compress the injectable market, and VK2809 (Viking's oral THR-β), which competes with resmetirom. The point is not that pemvidutide is doomed; it's that this is a multi-winner market with room for a differentiated tolerability-and-body-composition play — if the fibrosis question resolves.

The strategy: retreat from obesity is the smart move, not a concession

Here's a framing the bears get wrong. Altimmune is deliberately not chasing the headline obesity market, and that is the correct decision, not a white flag.

Winning in obesity now requires cardiovascular outcome trials enrolling tens of thousands of patients over years — a multi-billion-dollar undertaking only a Lilly or Novo can fund, and those two have lapped the field. A single-asset company with $535 million cannot win a capital war against companies spending that much per quarter. So management repositioned pemvidutide around serious liver disease, where the mechanism is differentiated and the incumbents are weaker or absent: MASH, and then the genuinely underappreciated part of this story — alcohol.

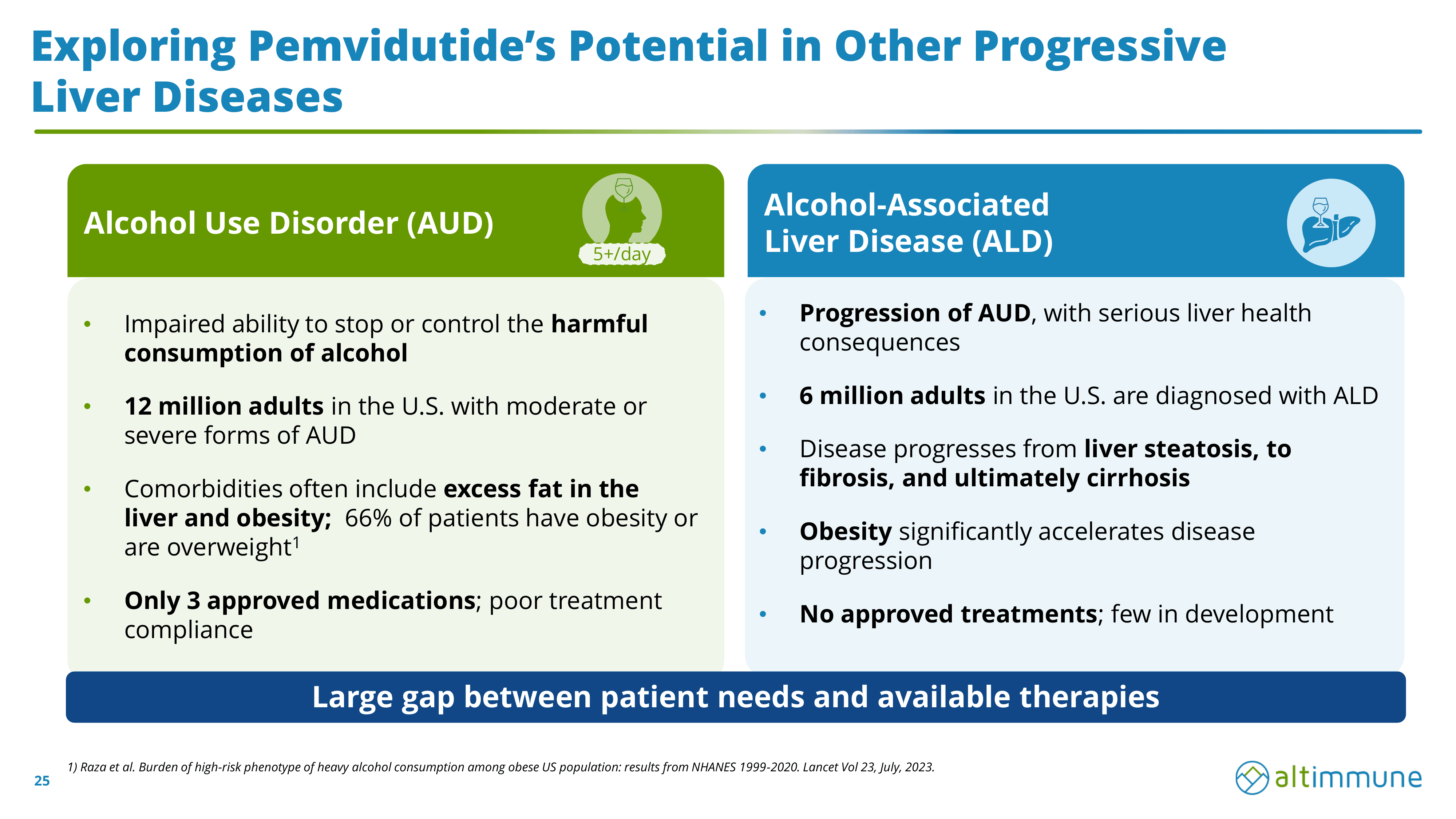

AUD and ALD: the optionality the market values at zero

The alcohol franchise is where the ~$90 million enterprise value looks most detached from reality, because it ascribes essentially nothing to two large, desperate, and nearly untreated markets — and it is the part of the story the market understands least.

The size of the problem. In the U.S., roughly 29 million adults have alcohol use disorder, of whom about 12 million have moderate-to-severe AUD — and only ~2% receive any pharmacological treatment. Alcohol is implicated in an estimated 178,000 U.S. deaths a year. One rung further down the disease ladder, ~6 million U.S. adults carry a diagnosis of alcohol-associated liver disease (ALD), which marches from fatty liver to fibrosis to cirrhosis — and for which there are no approved drug therapies at all. These are not niche indications. They are epidemics with a near-total treatment vacuum.

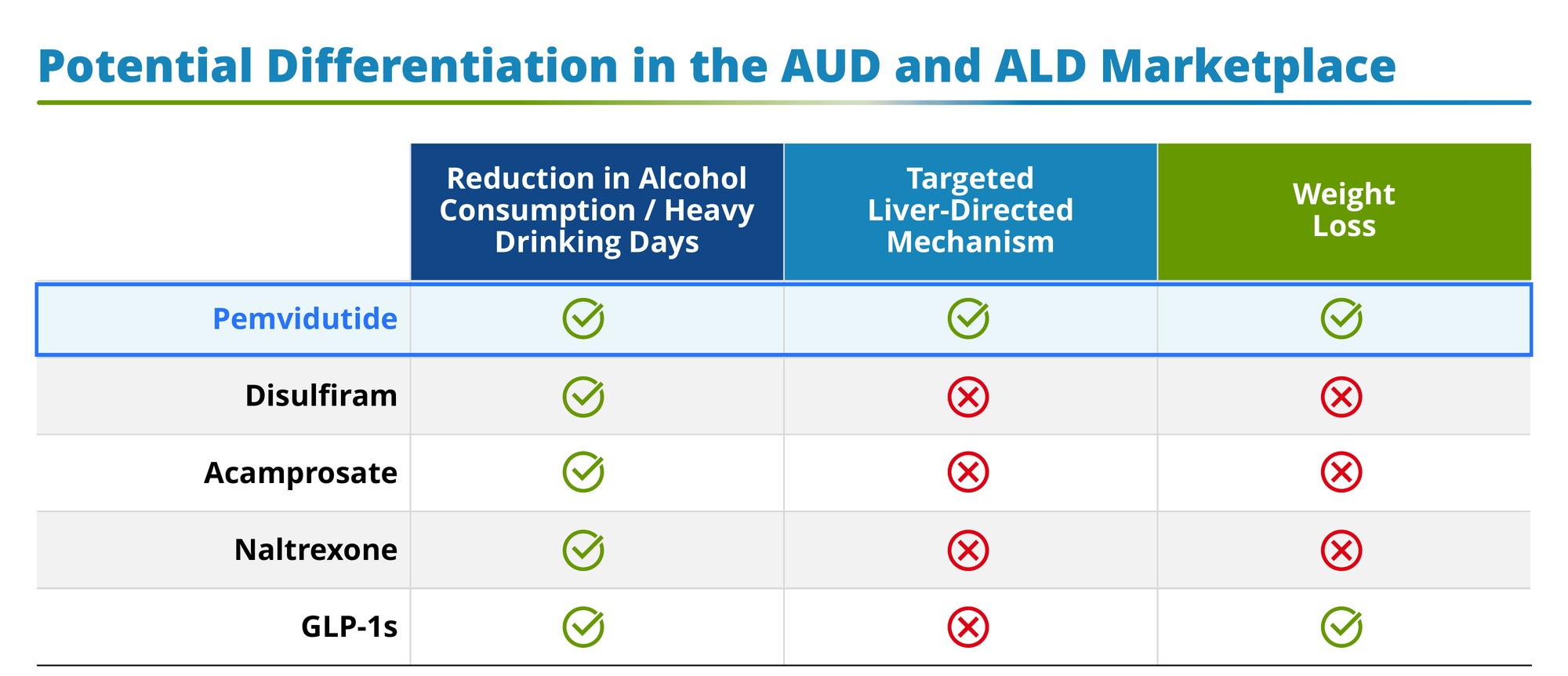

Why existing options fail. AUD has exactly three approved U.S. drugs — disulfiram (makes you sick if you drink, so compliance is dismal), acamprosate (modest effect, three-times-daily dosing), and naltrexone (works for some, but adherence is poor); Europe adds nalmefene. All share the same flaw: weak real-world persistence, and none does anything for the liver damage or the obesity that so often travels with heavy drinking. ALD, again, has nothing.

Why a GLP-1/glucagon drug could actually work here. The science underneath is more than a hunch. GLP-1 receptors sit in the brain's reward circuitry (the ventral tegmental area and nucleus accumbens), and activating them appears to blunt the dopamine hit that makes alcohol reinforcing — i.e., it turns down craving. The clinical read-throughs are accumulating: a randomized trial (Hendershot et al., JAMA Psychiatry 2025) showed semaglutide cut drinks per drinking day, heavy drinking days, and cravings (and even cigarettes) versus placebo; a larger Lancet 2026 trial (SEMALCO) tested semaglutide specifically in AUD patients with comorbid obesity — pemvidutide's exact target population — with a heavy-drinking-days primary endpoint; and real-world data associate GLP-1 use with roughly halved intoxication events (HR ~0.50). Pemvidutide itself cut alcohol intake up to 82% in a preclinical model.

The differentiation. Here is pemvidutide's actual pitch in alcohol, and it's clean: among AUD options, it is the only one that plausibly does all three things at once — reduces drinking (via GLP-1 in the brain), directly repairs the liver (via glucagon clearing hepatic fat), and drives weight loss. Disulfiram, acamprosate, and naltrexone hit only drinking. Pure GLP-1s hit drinking and weight but not the liver directly. Given that two-thirds of AUD patients are overweight or obese and their livers are under assault from both alcohol and metabolic fat, a single drug addressing craving, fat, and weight together is a genuinely novel proposition.

The trials and the timing. RECLAIM (Phase 2 AUD, N=100, pemvidutide 2.4 mg vs. placebo, primary endpoint = change in heavy drinking days) reads out topline in Q3 2026 — which has just begun. RESTORE (Phase 2 ALD, N=100, primary = liver-stiffness change at 24 weeks) completes enrollment in the same window. So a binary catalyst is weeks-to-months away. That's the opportunity and the risk: a positive RECLAIM would validate an entirely new franchise the market is currently pricing at zero; a negative one removes a pillar of the bull case right as it's being built. If you're underwriting ALT partly on alcohol, you are underwriting it directly into that readout.

The competitive caveat. GLP-1-in-alcohol is a class signal, which cuts both ways. It de-risks pemvidutide's biology — but it also means Novo and Lilly can pursue AUD themselves (a VA Phase 3 semaglutide AUD trial is already starting). Altimmune's defense is the dual mechanism and the liver angle; it is not a monopoly.

Management: the Intercept story cuts both ways

In most single-asset biotechs, management is a footnote. Here it's unusually load-bearing.

CEO Jerry Durso took the helm in January 2026. His last job was CEO of Intercept Pharmaceuticals — and Intercept is the single most instructive name you could put in charge of this company, for opposite reasons.

The bull read: Durso spent his career commercializing metabolic and liver drugs. He ran the Global Diabetes commercial organization at Sanofi, then joined Intercept, where he helped build and sell a real liver-disease franchise (Ocaliva in primary biliary cholangitis) and ultimately steered the company through its acquisition by Alfasigma. He knows how to launch a liver drug, negotiate payers, and run a sale process. His CCO, Linda Richardson, came from the same Intercept commercial team. This is a management group that has actually done the thing Altimmune needs to do next.

The bear read — and it's the ghost in this whole thesis: Intercept is also the cautionary tale of MASH regulatory heartbreak. Its lead liver asset, obeticholic acid, was pushed for NASH (MASH's old name) and was rejected by the FDA — twice — despite producing statistically significant fibrosis data, because the agency wasn't satisfied on the totality of benefit-versus-risk. Intercept eventually abandoned NASH and sold itself. So Durso has personally lived the exact nightmare ALT bulls are trying not to think about: a liver drug that hit endpoints and still couldn't get across the FDA finish line.

I read that as a net positive — you want the person who's been burned to be the one designing the Phase 3 and managing the FDA relationship — but it should sober up anyone who thinks approval is a formality. It isn't, in this disease, ever.

Financials: a fortress balance sheet and a diluted cap table

The good news is unambiguous. $535 million in cash as of April 30, 2026, after an oversubscribed $225 million April raise and over $300 million raised in the first half of 2026, with participation from top-tier biotech funds. Management says that funds the company through the 2029 Phase 3 readout — meaning no forced, dilutive financing into the single most important catalyst. Quarterly burn is modest for a late-stage story (Q1 2026 net loss $22.6 million; R&D $16.2 million; G&A $8.1 million), and there's essentially no debt.

The cost of that fortress is dilution. Weighted-average shares roughly doubled year over year (to ~124.5 million from ~75.5 million), and the April raise pushed the fully diluted count higher still. Serial equity issuance is how single-asset biotechs survive, but existing holders paid for the runway. And short interest sits around 21% of the float — a meaningful bet against the fibrosis outcome, which cuts both ways: it's conviction bearishness, but it's also fuel for a squeeze if PERFORMA or RECLAIM surprises to the upside. For what it's worth, sell-side coverage is constructive (recent Leerink Outperform initiation; H.C. Wainwright and others with targets well above the current price), but sell-side targets on binary single-asset names are worth exactly what the next data readout says they are.

The bear case, in one place

I keep the bear case consolidated so it can't be waved away in fragments. Here is what has to worry you:

- The fibrosis binary is existential. PERFORMA has to do on a 52-week biopsy what IMPACT could not do at 24 weeks. If it misses, this is a sub-cash stock with a busted thesis, and the NIT-vs-biopsy debate resolves the wrong way. MASH histology has a long graveyard.

- Single-asset concentration. There is no second product to cushion a pemvidutide failure. Everything — MASH, obesity optionality, AUD, ALD — is one molecule.

- Better-funded competition on both flanks. In the metabolic lane, Lilly and Novo can outspend Altimmune into oblivion and are moving into MASH and even AUD. In the anti-fibrotic lane, the FGF21s that strategics just paid billions for may prove the more important mechanism for advanced disease.

- AUD is unproven and un-owned. The alcohol thesis rests on a Phase 2 that hasn't read out and a mechanism any GLP-1 sponsor can pursue.

- Dilution and a heavy short. The cap table has grown a lot, and ~21% of the float is betting against the story.

- The Intercept precedent. The FDA has rejected a fibrosis-positive liver drug before. Designations and NITs are not approvals.

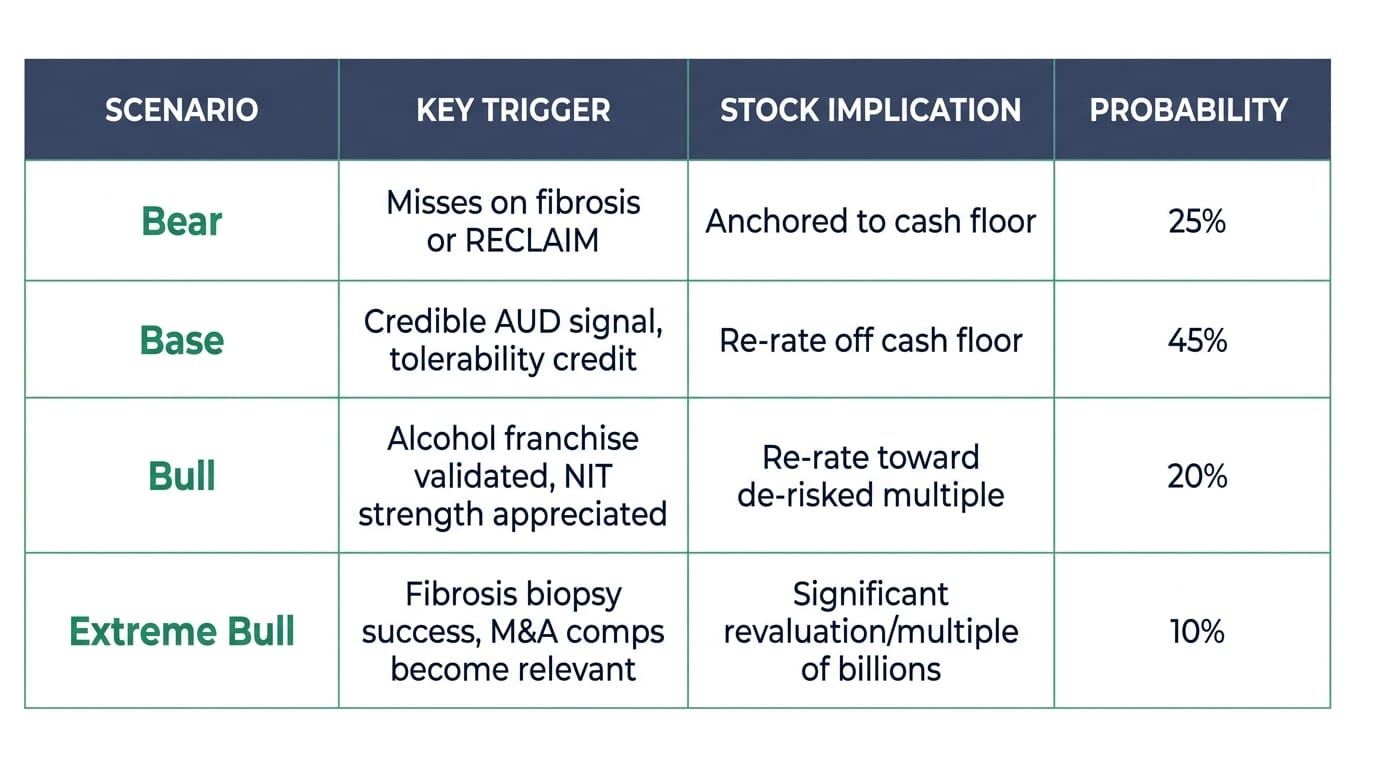

Four scenarios

No mechanical rules here — these are judgment-based ranges tied to the catalysts, in the house four-tier format.

Bear. PERFORMA misses on biopsy fibrosis, or RECLAIM disappoints and the alcohol optionality evaporates. The stock is anchored near its cash floor, and the floor erodes with burn. This is a real, non-trivial-probability outcome, and it's why the market has the stock where it is.

Base. RECLAIM shows a credible alcohol signal and PERFORMA stays on track, but the fibrosis question isn't fully resolved until 2029. The stock re-rates off cash as the market gives partial credit for the AUD/ALD franchise and best-in-class tolerability — a meaningful move from ~$90 million EV, without pricing in a MASH win.

Bull. A clean RECLAIM readout opens the alcohol franchise, the 48-week NIT strength gets re-appreciated, and pemvidutide's tolerability/body-composition edge starts to look like the profile a partner wants. The stock re-rates toward a de-risked-metabolic-asset multiple — think a fraction of where VKTX trades — and an ex-U.S. obesity licensing or MASH partnership becomes the swing catalyst, validating the asset with someone else's balance sheet.

Extreme Bull. PERFORMA ultimately delivers fibrosis on biopsy, and pemvidutide is revalued as what the bulls always claimed: a best-tolerated, muscle-sparing, liver-and-alcohol franchise in a market where strategics have paid multiples of billions. At that point the relevant comps are the M&A prints, not the current cash balance. This is the low-probability, high-magnitude tail — the reason the stock is interesting at all at these levels.

Catalyst calendar

- Q3 2026: RECLAIM Phase 2 AUD topline — the nearest binary, and the cheapest optionality in the story.

- Q3 2026: RESTORE Phase 2 ALD enrollment complete.

- 2H 2026: PERFORMA Phase 3 MASH initiation.

- Ongoing: any ex-U.S. obesity licensing or MASH partnership announcement — an external validation catalyst management has openly said it's pursuing.

- 2029: PERFORMA 52-week biopsy readout — the event the whole equity ultimately hinges on.

The bottom line

Strip away the noise and the market is making a single, aggressive claim: that a fibrosis miss at 24 weeks is enough to value pemvidutide — best-in-class tolerability, class-leading muscle preservation, deep liver-fat and NIT improvements, plus untouched AUD and ALD franchises — at barely more than the cash in the bank. For that verdict to be right, PERFORMA has to fail and the alcohol biology has to disappoint and the tolerability edge has to prove commercially irrelevant. For it to be wrong, you don't need all four assets to hit — you need any one of them (a positive RECLAIM, a partnership, or a credible path through the Phase 3) to remind the market there's a company here, not just a treasury.

That asymmetry — a near-cash floor against multiple independent shots on goal, with a genuine and non-trivial risk that the central one misses — is the entire reason to have an opinion on ALT. The next honest checkpoint arrives in Q3, and it costs the market nothing to keep ignoring it until then.

This article is independent research published on BiostockInfo.com and does not constitute financial advice. The author may hold positions in securities discussed. Always conduct your own due diligence before making investment decisions. Past performance is not indicative of future results.