Beyond the Weight Loss Olympics: Why the Drug Patients Actually Stay On Longer Could Win

Zealand ($ZEAL) Pharma's petrelintide posted among the cleanest safety profiles ever seen in an obesity trial. The market punished it 35%. The data deserves a closer look.

On March 5, 2026, Zealand Pharma reported Phase 2 data from the ZUPREME-1 trial. The stock cratered 35% in a single session — its worst day ever. Roche, Zealand's $5.3 billion partner, slid 3%. Cantor Fitzgerald cut to Neutral. Jefferies called it "disappointing." The headline verdict: 10.7% weight loss isn't enough.

(A quick note for US-based readers: Zealand Pharma (ticker: ZEAL) is listed on the Nasdaq Copenhagen exchange, not on US stock markets. It can be traded via certain US brokers that offer access to the Copenhagen exchange, or through OTC markets under the ticker ZLDPF. Roche trades on the SIX Swiss Exchange and via ADRs in the US under RHHBY.)

The efficacy miss is real and shouldn't be minimised. Analysts had pencilled in 13-20%. The buy-side wanted 15%+. Against Eli Lilly's eloralintide at 20.1% and even Novo's cagrilintide at 11.8%, petrelintide's headline number is objectively behind.

But there's a second dataset in this readout that got steamrolled by the efficacy disappointment — and it may turn out to matter more than the weight loss number. The safety and tolerability profile from ZUPREME-1 is, by any reasonable reading, exceptional.

The question this article explores: in a market where half of patients quit their obesity drug within a year, does the drug with the best tolerability have a commercial path — even if its weight loss headline is modest?

The honest answer is: it might, but it's not proven yet.

What ZUPREME-1 Actually Showed

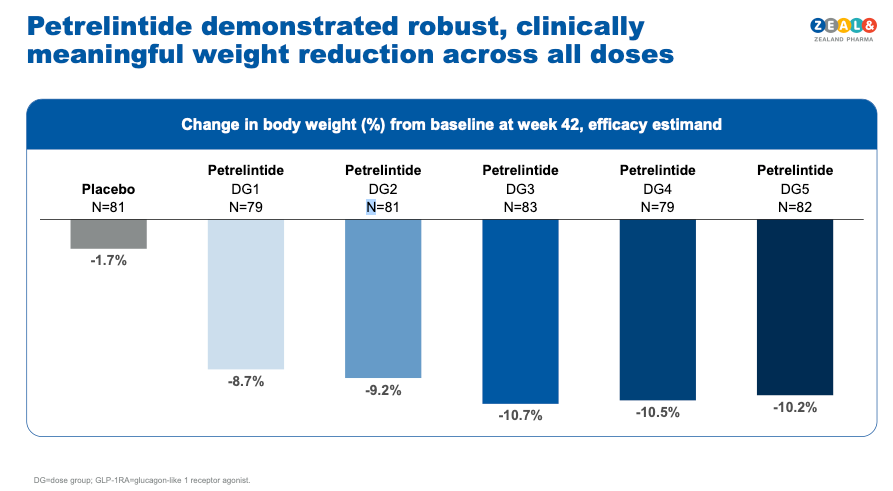

The trial: 493 adults with overweight or obesity (mean BMI 37 kg/m², 53% female), randomized across five petrelintide dose arms and placebo, across 33 sites in the US, Poland, and Romania. Once-weekly subcutaneous injection, dose-escalated every four weeks over 16 weeks, then maintained through week 42.

Efficacy: Up to 10.7% mean body weight loss at week 42 (efficacy estimand) versus 1.7% for placebo — a ~9% placebo-adjusted reduction. The weight loss curve showed no plateau at 42 weeks.

Tolerability — and this is where the data gets genuinely interesting:

In the maximally effective dose arm:

- Zero cases of vomiting. None.

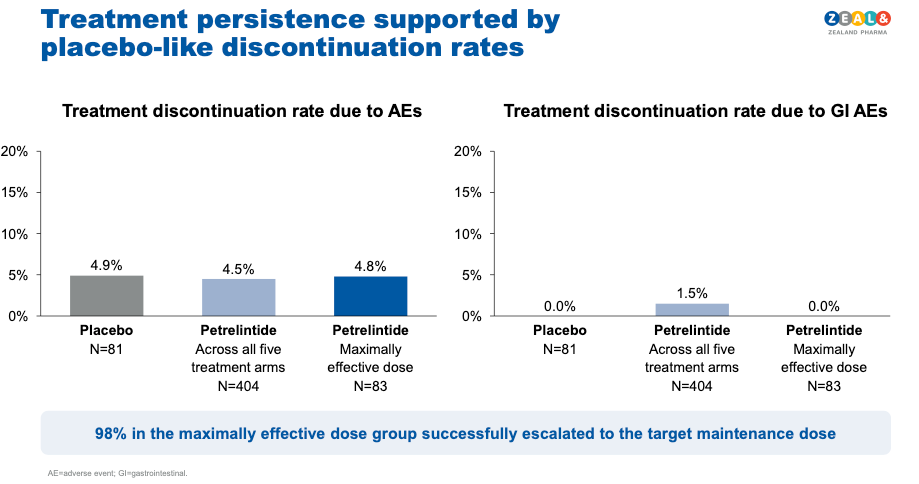

- No GI-related treatment discontinuations. Not one patient stopped because of GI side effects.

- Total discontinuation due to adverse events: 4.8% versus 4.9% for placebo. The drug arm had the same dropout rate as the sugar pill.

- Overall trial withdrawal: 8.4% across all petrelintide arms versus 13.6% for placebo.

- 98% of participants successfully escalated to the targeted maintenance dose.

- No unexpected safety signals — no alopecia, no neuropsychiatric events, no fatigue signals.

David Kendall, Zealand's CMO, described it as "GI adverse events comparable to placebo." The topline data supports that characterisation.

The Efficacy Problem: Why the Bear Case Is Serious

Before making any bull case, let's be honest about what went wrong.

The headline miss. 10.7% at 42 weeks places petrelintide well behind Lilly's eloralintide (20.1% at 48 weeks) and modestly behind Novo's cagrilintide monotherapy (11.8% at 68 weeks, though over a longer treatment period). In a market that has been conditioned to judge drugs by peak weight loss, this is a meaningful shortfall.

The flat dose-response is arguably more concerning than the headline. Weight loss across the top three dose arms clustered between 10.2% and 10.7%. JPMorgan flagged this as suggesting "limited incremental benefit from dose escalation." If you can't push efficacy higher by giving more drug, the ceiling may already be visible — and that ceiling is lower than competitors.

Zealand's management argues Phase 3 will improve. CEO Adam Steensberg pointed to ZUPREME-1's 53% female representation (typical obesity trials enrol ~70-80% women, who consistently lose more weight) and the relatively short 26-week maintenance period as factors that suppressed the topline number. He expressed confidence that an optimised Phase 3 could deliver mid-teens weight loss.

These are plausible factors, but they remain management projections, not evidence. As Barclays analysts noted, the market is "unlikely to credit a Phase 3 fix" two years out. Until Phase 3 data exist, the 10.7% is the number.

Cantor Fitzgerald made a further important point: petrelintide's good tolerability does not, by itself, establish clear differentiation from other amylin monotherapies. Cagrilintide monotherapy in REDEFINE-1 posted a 1.3% discontinuation rate. Eloralintide at lower doses (1mg, 3mg) had adverse event rates similar to placebo. The tolerability advantage may be relative rather than unique to petrelintide, making it harder to argue for a differentiated commercial position on safety alone.

This is a fair critique. Cross-trial comparisons are always imperfect, and the amylin class as a whole appears better tolerated than GLP-1 monotherapy. The question is whether petrelintide's tolerability profile is sufficiently differentiated within the amylin class to justify its position — and that won't be answered until we see all three compounds in comparable Phase 3 settings.

The Tolerability Thesis: Why It Matters Anyway

With those caveats stated, the tolerability data does matter — potentially a great deal. Here's why.

Patients aren't staying on GLP-1 therapy. According to IQVIA data, only about 34% of GLP-1 users remain on therapy at 12 months. By 6 months, roughly half have stopped. The primary reason? GI side effects — nausea, vomiting, diarrhea, constipation. A January 2026 BMJ study found that patients who lost weight with GLP-1 drugs regained weight significantly faster after stopping than those who lost weight through diet and exercise.

This creates a vicious cycle: patients start therapy, lose weight, can't tolerate the side effects, stop, regain the weight (disproportionately as fat), and either restart or give up. For US payers spending $1,000+/month, the economics of 50%+ annual churn are brutal.

Here's how the competitive field looks on tolerability — bearing in mind that cross-trial comparisons have limitations in trial design, population, and duration:

Semaglutide 2.4mg (Wegovy) — STEP 1:

- Nausea: ~44% · Vomiting: ~24% · Diarrhea: ~30%

- Discontinuation due to AEs: ~7%

Tirzepatide 15mg (Zepbound) — SURMOUNT-1:

- Nausea: ~33% · Vomiting: ~12.2% · Diarrhea: ~23%

- Discontinuation due to AEs: ~6.3%

Survodutide 4.8mg (Boehringer/Zealand) — Phase 2 Obesity:

- Nausea: ~63.6% · Vomiting: ~35.1% · Diarrhea: ~19.5%

- Discontinuation due to AEs: ~28.6% (highest dose); GI-related: ~26%

CagriSema 2.4/2.4mg (Novo Nordisk) — REDEFINE-1:

- Nausea: ~55% · Vomiting: ~26.1% · Constipation: ~30.7%

- Discontinuation due to AEs: ~6% (vs 3.7% placebo)

- Total GI AEs: 79.6% vs 39.9% placebo

- Only 57% of patients reached maximum dose at week 68; 6 deaths occurred across both REDEFINE trials (all in CagriSema groups, including one suicide per trial — not determined to be causally related)

Cagrilintide 2.4mg monotherapy (Novo Nordisk) — REDEFINE-1:

- Nausea: ~23.8% · Vomiting: ~7% · Constipation: ~20.5%

- Discontinuation due to AEs: ~1.3% (flexibly dosed monotherapy comparator arm)

Eloralintide (Eli Lilly) — Phase 2:

- Nausea: ~32.7% pooled (64.3% at 6mg; 25% at 3-9mg escalation)

- Fatigue: ~26.9% pooled (42.6% at 9mg) · Vomiting: ~8.2% pooled

- Discontinuation due to AEs: ~10% pooled (21% at 6mg) vs ~8% placebo

- Alopecia: ~9.3% at 9mg

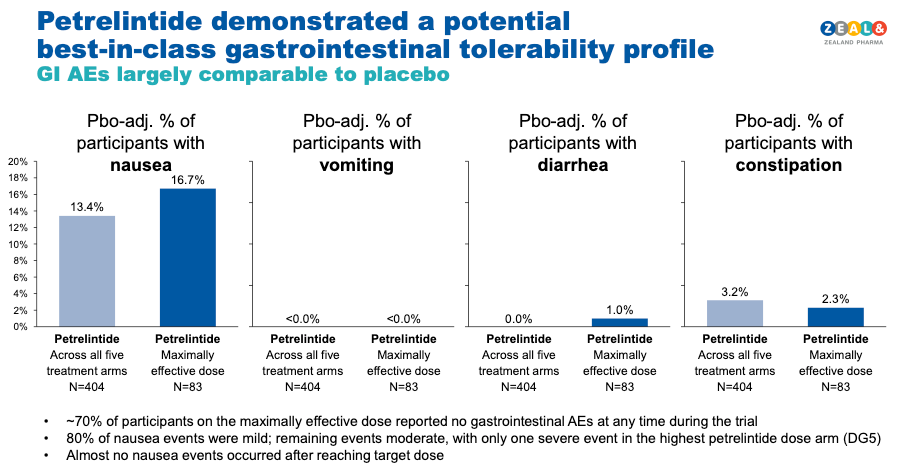

Petrelintide (Zealand/Roche) — ZUPREME-1 (maximally effective arm):

- Vomiting: 0% · GI-related discontinuation: 0%

- Diarhhea: 1.0%

- Constipation: 2.3%

- Total AE-related discontinuation: 4.8% (vs 4.9% placebo)

Even acknowledging cross-trial limitations, petrelintide's profile stands out — particularly the zero vomiting and zero GI discontinuations. Whether that translates into meaningfully better real-world adherence than cagrilintide (which also showed very low discontinuation at 1.3%) remains to be seen. But if tolerability does prove to be the key determinant of long-term commercial success in obesity, the ZUPREME-1 data is a strong credential.

What Is Petrelintide and How Does It Work?

Petrelintide is a long-acting amylin analog — and the mechanism matters for understanding both the safety profile and the combination potential.

Amylin is a 37-amino acid hormone co-secreted with insulin from the pancreatic beta cells in response to food. It works differently from GLP-1:

GLP-1 drugs (semaglutide, tirzepatide) primarily suppress appetite — they reduce hunger signals through receptors in the gut and brain. The aggressive appetite suppression is also what drives the GI side effects: nausea, vomiting, and delayed gastric emptying pushed to uncomfortable extremes.

Amylin analogs (petrelintide, cagrilintide, eloralintide) primarily increase satiety — they make you feel full faster. Instead of suppressing the desire to eat, amylin signals to the brain that you've had enough sooner. It works through different brain regions (area postrema, hypothalamus) and, preclinically, by restoring sensitivity to leptin — the body's master hormone for long-term energy balance.

A useful analogy: GLP-1 is like someone taking the food off your plate. Amylin is your brain recognising earlier that the plate is full enough.

This distinction may also explain the tolerability gap. Amylin analogs are working with the body's natural satiety signaling rather than overriding appetite through a pharmacologically aggressive pathway. The result — at least in clinical data to date — is generally milder GI effects across the class.

Petrelintide specifically is engineered from the human amylin backbone with a 10-day half-life (enabling once-weekly dosing), ~85% bioavailability, and chemical stability at neutral pH. That last point is technically important: stability at neutral pH means petrelintide can potentially be co-formulated in the same syringe with other peptides — a key enabler for combination therapy.

The leptin sensitisation angle deserves a mention with appropriate caution. Preclinical studies showed amylin restored leptin responsiveness in diet-induced obese rodents, and the amylin-leptin combination produced synergistic weight loss beyond what either agent achieved alone. If this translates to humans, it could mean more durable weight loss with less rebound after stopping therapy. But this remains a preclinical hypothesis, not a clinical finding. The ZUPREME program has not yet reported leptin sensitivity data in humans.

The Roche Partnership and the Combination Thesis

Zealand's $5.3 billion collaboration with Roche (announced March 2025) is structured around petrelintide both as a monotherapy and — critically — as a combination with CT-388, Roche's dual GLP-1/GIP receptor agonist.

Deal economics in brief: $1.65 billion upfront ($1.4B at closing + $250M in anniversary payments). $1.2 billion in development milestones (primarily tied to Phase 3 initiation). $2.4 billion in sales milestones. 50/50 profit share in the US and Europe. Roche handles manufacturing — Zealand carries no CAPEX burden. Zealand is eligible for a $575 million milestone upon Phase 3a initiation (expected H2 2026) and a $125 million anniversary payment in Q2 2026.

The combination thesis is strategically plausible but unproven. The logic: maximise the dose of the well-tolerated agent (petrelintide) and add a moderate dose of the more efficacious but less tolerable agent (CT-388, a GLP-1/GIP agonist), targeting 20%+ weight loss with a dramatically cleaner safety profile than pushing GLP-1 monotherapy to maximum dose.

There is proof-of-concept for amylin + GLP-1 combinations: Novo's CagriSema hit 22.7% weight loss in REDEFINE-1. But CagriSema also carried the full GI burden of high-dose semaglutide (55% nausea, 26% vomiting). Whether petrelintide + CT-388 at optimised doses can match that efficacy with better tolerability is the key unanswered question. The Phase 2 combination trial is planned for H1 2026, with data likely in 2027. Until then, this is a forward-looking narrative, not evidence.

There's also a potential use case in MASH (metabolic dysfunction-associated steatohepatitis). A well-tolerated amylin backbone could serve as a combination partner for liver-directed therapies like Madrigal's resmetirom, adding weight loss without stacking GI side effects. But again, this is theoretical.

The Amylin Arms Race: Petrelintide in Context

Petrelintide is competing in an increasingly crowded amylin class. A honest assessment of its competitive position:

Eloralintide (Eli Lilly) is the efficacy leader — 20.1% weight loss at 48 weeks (9mg dose) — and it comes from the company with the deepest obesity pipeline and the largest commercial infrastructure. However, eloralintide's tolerability at the top doses is rougher: nausea hit 64% at 6mg, fatigue 43% at 9mg, and the 6mg arm saw 21% discontinuation. Slower escalation (3-9mg) improved this to 25% nausea and ~16% weight loss. Lilly is preparing Phase 3 enrolment.

Cagrilintide (Novo Nordisk) sits between the two: 11.8% weight loss at 68 weeks with good tolerability (1.3% discontinuation). But Novo may have under-dosed it — a prior Phase 2 showed the 4.5mg dose outperforming 2.4mg, yet REDEFINE-1 capped at 2.4mg. Novo's real strategy is CagriSema, the combination with semaglutide, not cagrilintide as a standalone.

ABBV-295 (AbbVie/Gubra) — Just reported (March 9, 2026) Phase 1 MAD data showing 7.75-9.79% weight loss at 12 weeks. Favourable tolerability. But the trial enrolled mostly males (88.3%) with mean BMI below 30, making comparison difficult. AbbVie acquired the asset from Gubra for $350M in March 2025.

Where does petrelintide fit? Objectively, it's behind eloralintide on efficacy and roughly comparable to cagrilintide. Its clearest advantage is the tolerability profile — particularly the zero vomiting and zero GI discontinuations in ZUPREME-1. Whether that advantage is unique to petrelintide or a feature of its specific dosing/escalation scheme (as Cantor argues) won't be settled until Phase 3 data from multiple amylin programs are available for comparison.

Petrelintide's potential differentiator may ultimately be less about monotherapy superiority and more about its combination potential. Its neutral pH stability allows co-formulation with other peptides — a technical advantage that could matter enormously if the market evolves toward combination regimens, as seems likely.

What to Watch

Rather than fixating on the 10.7% headline, here are the catalysts that will determine whether petrelintide's tolerability story translates into commercial value:

1. Full ZUPREME-1 data presentation (scientific conference, 2026). The MRI body composition data (lean mass vs fat mass), waist circumference, hsCRP, lipids, and HbA1c will reveal far more about petrelintide's metabolic impact than the weight number alone. If lean mass preservation is confirmed, it strengthens the differentiation argument. Its absence from the topline press release is notable — it may simply not have been ready, or it may have been less favourable than hoped.

2. ZUPREME-2 readout (H2 2026) — petrelintide in patients with type 2 diabetes. Amylin analogs have shown competitive weight loss versus GLP-1s in diabetic populations historically. A strong T2D result would validate a second major use case.

3. Petrelintide/CT-388 combination Phase 2 (initiating H1 2026) — This is arguably the most important trial for the investment thesis. If the combination delivers ≥20% weight loss with a cleaner safety profile than CagriSema, petrelintide's value proposition transforms entirely. If it doesn't, the monotherapy profile alone may not support a differentiated commercial position.

4. SYNCHRONIZE-1 survodutide Phase 3 data (H1 2026) — Zealand's other major asset. Survodutide's Phase 3 obesity readout from Boehringer Ingelheim is imminent and could drive significant royalty revenues.

5. The $575M Phase 3a milestone — Will Roche and Zealand initiate Phase 3 in H2 2026 as planned? That milestone payment would signal Roche's continued conviction despite the Phase 2 results.

The Bottom Line

The obesity drug market is at an inflection point. The first wave — the "Weight Loss Olympics" — was about proving that drugs could make people lose significant weight. Semaglutide proved it. Tirzepatide raised the bar. Mission accomplished.

The next wave — what Zealand frames as the "Quality and Durability Era" — will need to solve the problems the first wave created: GI misery, muscle wasting, weight regain, poor adherence, and the stop-start cycle that undermines both patient outcomes and the economics of the entire category.

Petrelintide's ZUPREME-1 data doesn't prove that tolerability alone can build a franchise. What it does is provide the strongest clinical evidence to date that an obesity drug can deliver meaningful weight loss (10.7%, with no plateau) while maintaining a safety profile indistinguishable from placebo — a combination that no other drug in Phase 2 or Phase 3 development has demonstrated in a properly powered trial with a representative obesity population.

That's not enough to declare victory. The efficacy gap is real, the flat dose-response is concerning, and the combination thesis is unproven. But in a market where half of patients abandon treatment within a year, the tolerability data from ZUPREME-1 deserves to be weighted more heavily than a single-day 35% stock selloff would suggest.

The Weight Loss Olympics crowned impressive sprinters. But obesity is a marathon. And right now, petrelintide looks like the drug that might actually finish the race.

Whether that's enough, we'll know when the combination data arrives.

This article is for informational purposes only and does not constitute financial, investment, or medical advice. Always conduct your own due diligence and consult a qualified professional before making investment decisions.