MoonLake ($MLTX): From Collapse to Recovery Play—The Nanobody Rebound Story

The Fall from Grace: A 90% Overnight Collapse

On September 28, 2025, MoonLake Immunotherapeutics (NASDAQ: MLTX) experienced one of biotech's most dramatic single-day collapses in recent memory. The stock plummeted 90%—from $62 to as low as $5.95—as the company announced results from its Phase 3 VELA program for sonelokimab, the company's sole clinical-stage asset. For institutional and retail investors who had championed the company's scientific superiority and claimed acquisition rejections from major pharma, it was a devastating blow that instantly wiped out billions in market capitalization and prompted multiple securities class action lawsuits.

The dramatic reversal encapsulates the existential risk inherent in binary biotech events—an entire company's valuation erased in a single press release. Yet six weeks later, as additional clinical data emerged and management clarified the regulatory pathway forward, a compelling comeback narrative has materialized. This isn't a story of vindication, but of realistic assessment: the data, while disappointing relative to pre-announcement expectations, remains clinically meaningful. More importantly, the company possesses the financial runway, management vision, and upcoming regulatory catalyst that could position it for a remarkable recovery—if execution delivers.

The Pre-Collapse Setup: Irrational Exuberance

To understand the magnitude of the September collapse, one must contextualize the extraordinary market enthusiasm that preceded it. By mid-2025, MoonLake had cultivated an almost mythical status in biotech circles.

The Nanobody Narrative: The company's flagship molecule, sonelokimab (SLK), is a tri-specific IL-17A and IL-17F inhibitor packaged in a humanized nanobody format—a smaller, engineered antibody fragment (~40 kDa versus ~150 kDa for conventional monoclonal antibodies). MoonLake's investor presentations emphasized proprietary advantages: enhanced tissue penetration, manufacturing ease, thermostability, and the ability to target all three relevant IL-17 dimers (IL-17A/A, IL-17A/F, and IL-17F/F) simultaneously. Competitors' monoclonal antibodies, by contrast, were portrayed as narrower in scope.

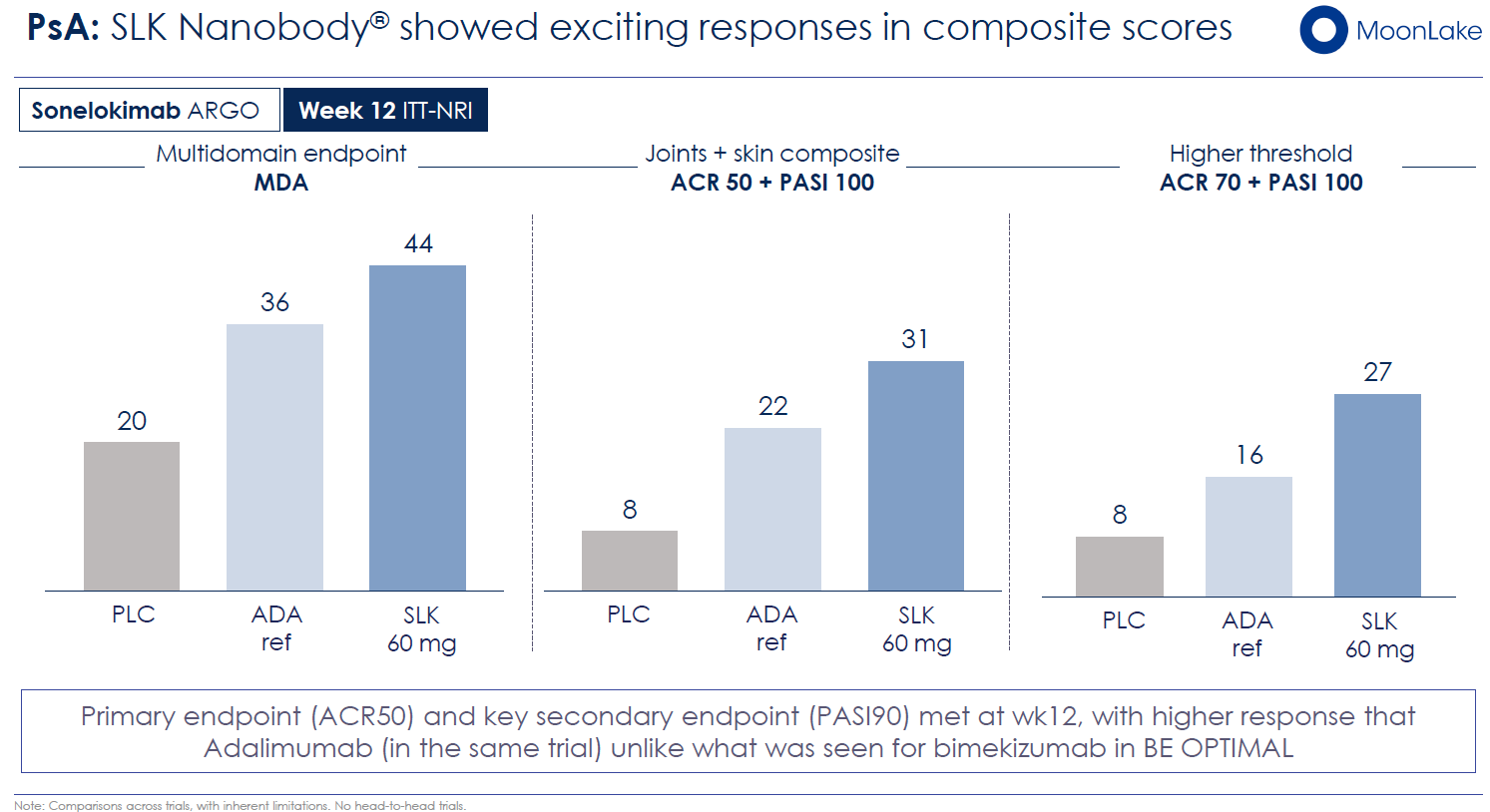

Strong Phase 2 Data: The Phase 2b MIRA trial in hidradenitis suppurativa (HS) enrolled 234 patients and reported a 43.3% HiSCR75 response rate (≥75% reduction in abscess and inflammatory nodule count) compared to 14.7% placebo—a delta of 28.6 percentage points. By current standards in HS, this represented best-in-class performance. The company had explicitly stated that sonelokimab could become the "gold standard" for HS therapy. In psoriatic arthritis (PsA), the Phase 2 ARGO trial reported ~60% ACR50 responses and achieved Minimal Disease Activity (MDA) in a substantial cohort.

Acquisition Rumors and Shareholder Worship: In June 2025, reports surfaced that Merck had approached MoonLake with a $3 billion acquisition proposal—a valuation implying considerable upside from current trading levels. Management allegedly rebuffed the offer, claiming they didn't "need the cash" and preferred to independently guide sonelokimab through the development gauntlet to maximize shareholder value. This bold rejection energized retail and institutional investors alike, creating a sense that management was supremely confident and that major pharma recognized transformative potential.

The Street's Embrace: By September 28, analyst consensus price targets averaged ~$75 per share. The research community had largely accepted management's claims of superiority, with major banks issuing "Outperform" and "Buy" ratings. The implied market consensus seemed to embed a high probability of HS regulatory approval with peak sales exceeding $5 billion.

Into this fervent backdrop, the Phase 3 VELA readout was meant to be a formality—a confirmation of Phase 2's dominance.

Phase 3 Reality: The Placebo Complication and Mixed Efficacy

When MoonLake announced the VELA-1 and VELA-2 results on September 28, the market discovered several uncomfortable truths.

The Two-Strategy Conundrum

The VELA program employed two pre-specified analysis strategies for handling intercurrent events (patients who started rescue medications or discontinued for lack of efficacy), a design approach standard in clinical trials but easily misunderstood by market participants unfamiliar with regulatory nuance.

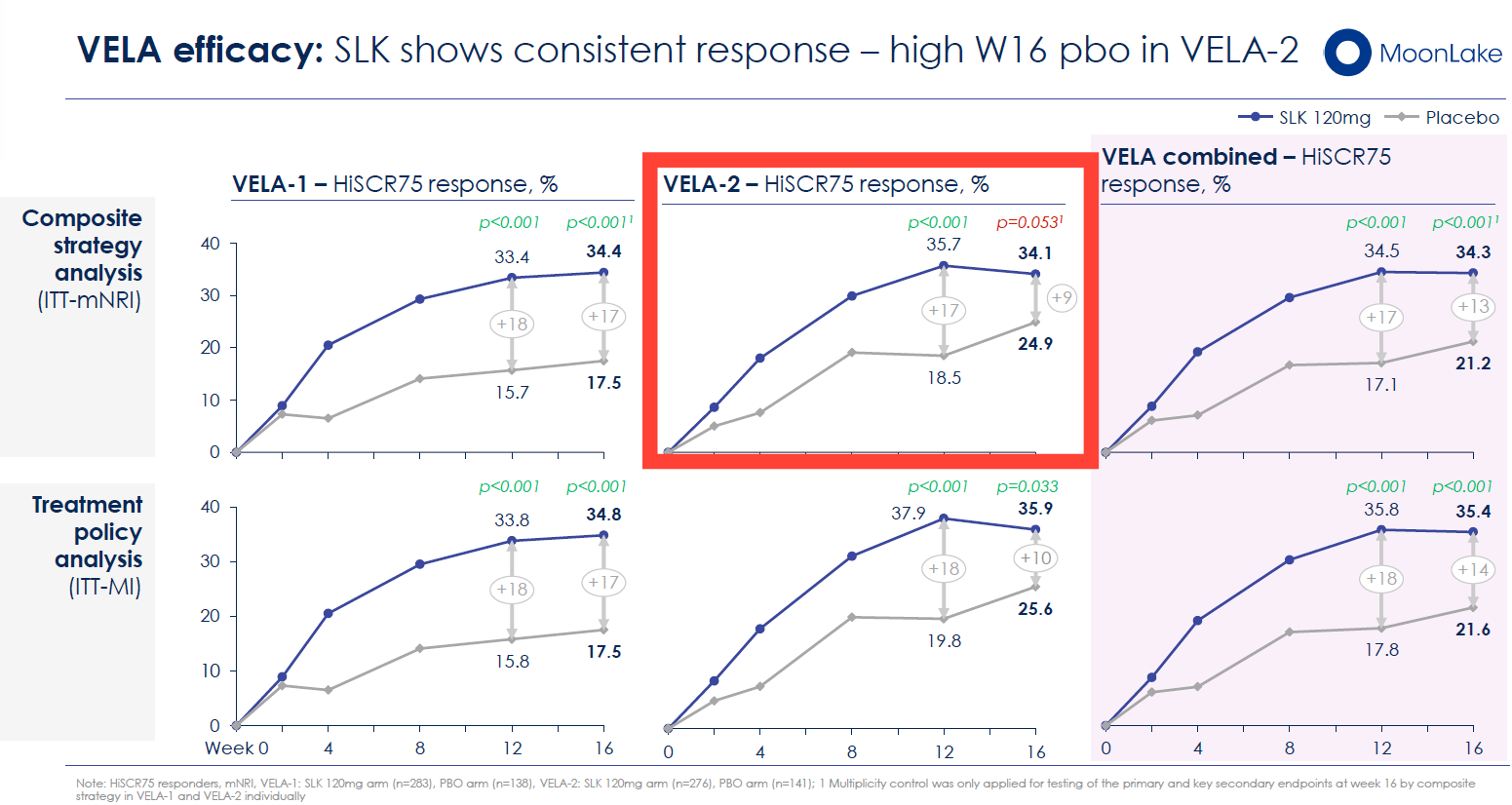

VELA-1 Success: In the first trial, sonelokimab achieved HiSCR75 responses of 35.7% (composite strategy) or 37.9% (treatment policy strategy) versus 18.5% and 19.8% placebo, respectively. Both analyses demonstrated statistical significance (p<0.001), with delta-to-placebo of 17–18 percentage points.

VELA-2 Disappointment: The second trial told a different story. Sonelokimab achieved similar absolute response rates: 34.1% (composite) or 35.9% (treatment policy) versus 24.9% and 25.6% placebo. The critical difference: a higher-than-anticipated placebo response. Under the composite strategy (the pre-specified primary estimand using multiple imputation for intercurrent events), VELA-2 failed to achieve statistical significance on the primary endpoint (p=0.053). Under the treatment policy strategy, VELA-2 did demonstrate significance (p=0.033).

The Wall Street Reckoning

Analysts reacted viscerally. Stifel downgraded to Hold from Buy, slashing the price target to $13 from $77 and cutting the probability of HS regulatory success from 75% to 33%. RBC Capital downgraded to Sector Perform, reducing its target to $10 from $67. The consensus emerged: VELA-2's failure to meet the composite primary endpoint was a "near-miss" and an "arguably worst-case outcome." The placebo response, some whispered, was so elevated as to cast doubt on the trial's design integrity.

Securities litigation followed swiftly, with multiple law firms alleging that management had failed to disclose the risk of elevated placebo responses and had made misleading claims about sonelokimab's superiority to bimekizumab (BIMZELX), the IL-17A/F monoclonal antibody recently approved by the FDA for HS.

The Stock's Fall: The 90% overnight collapse reflected a complete repricing of MoonLake's risk profile. Investors who had believed in the company's narrative suddenly faced the prospect of regulatory rejection, failed pipeline, and capital depletion. The company's market cap plummeted from ~$3.9 billion to ~$377 million—a loss of ~$3.5 billion in market value.

The Critical Reframe: Combining Both Trials and Contextualizing the Data

Yet within weeks, a more nuanced interpretation began to emerge—one grounded in regulatory precedent and statistical reality.

Combined VELA Program Significance

When MoonLake combined the VELA-1 and VELA-2 data across both pre-specified strategies, the pooled result showed clinically meaningful and statistically significant improvement across all primary and key secondary endpoints (p<0.001). The combined HiSCR75 response rate across both trials reached 34.3% (composite) and 35.4% (treatment policy) versus 21.2% and 21.6% placebo—a consistent delta of 13–14 percentage points.

This is an important distinction: while VELA-2 individually narrowly missed the composite primary endpoint, the regulatory agencies (FDA and EMA) typically review the entire dataset package when making approval decisions. The fact that one of two identical trials met the primary under both strategies, and the second trial met it under the treatment policy strategy with a p-value of 0.033, does not automatically spell rejection—particularly when secondary endpoints are robust and the safety profile remains favorable.

Placebo Response: Clinical Context, Not Disqualification

The "higher-than-expected" placebo response in VELA-2 has been scrutinized as evidence of trial failure. However, clinical trial experts have noted that placebo responses in HS are notoriously variable, driven by factors including publication bias in site selection, patient selection effects, and the subjective nature of the primary endpoint (abscess and nodule counting). VELA-2's placebo rate, while elevated, is not unprecedented in HS trials.

Importantly, the active-arm response rates in both VELA-1 (35.7–37.9%) and VELA-2 (34.1–35.9%) are remarkably consistent—essentially identical across the two studies. If trial design were fundamentally flawed, one would expect divergent active-arm responses. The consistency of sonelokimab's effect, despite variable placebo responses, argues for a real pharmacological signal.

Secondary Endpoints: The Differentiating Factor

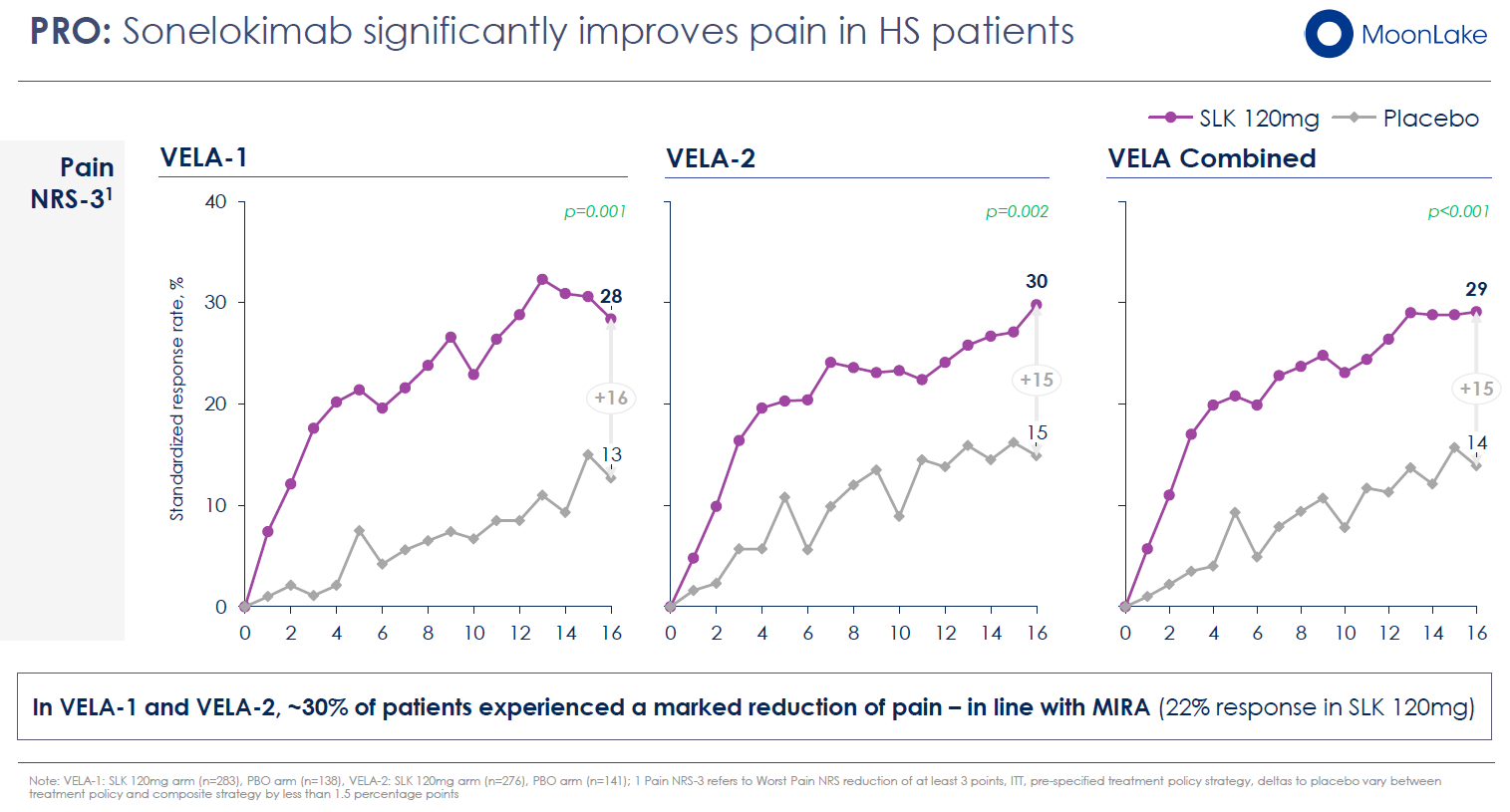

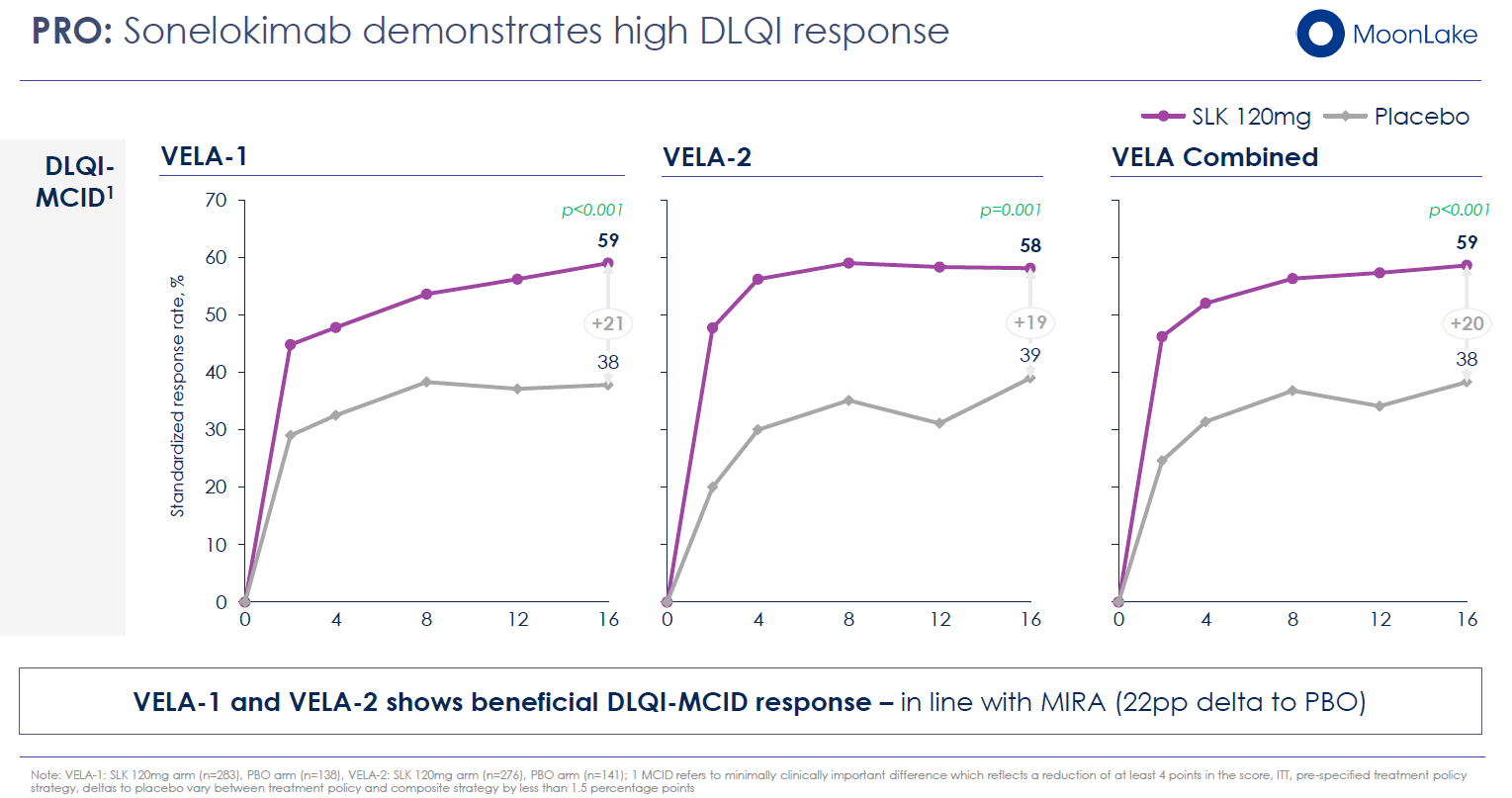

Where sonelokimab distinguishes itself is in patient-reported outcomes and quality of life metrics—the very measures that matter most to patients enduring HS's devastating consequences.

In VELA-1 and VELA-2 combined, sonelokimab demonstrated:

- Pain Reduction: A statistically significant reduction in patients' global assessment of skin pain (NRS50: ≥3-point improvement from baseline), with substantial proportions achieving clinically meaningful improvement

- Draining Tunnel Resolution (DT100): Complete resolution of all draining tunnels in a meaningful subset of patients—lesions that represent irreversible tissue damage and profound functional impairment

- Quality of Life: Significant improvements in Dermatology Life Quality Index (DLQI), with ≥4-point improvements (the minimum clinically important difference) in the majority of treated patients

These secondary endpoints are not peripheral—they directly address why HS patients suffer. The commercial label, if approved, will emphasize these benefits. Moreover, these outcomes remained robust and statistically significant even in VELA-2, where the primary endpoint narrowly missed under one strategy.

Competitive Positioning: Beyond the Perception of Inferiority

The market initially interpreted VELA-2's results as evidence that sonelokimab is clinically inferior to bimekizumab (BIMZELX), the IL-17A/F monoclonal antibody competitor. Yet a careful examination of published data reveals a more nuanced picture.

Bimekizumab's Published Data: In the BE HEARD I and II Phase 3 trials, bimekizumab achieved HiSCR75 response rates of 33.4% and 35.7% at week 16 versus 15.7% and 18.5% placebo (deltas of 17.7 and 17.2 percentage points, respectively). These are strikingly similar to sonelokimab's 35.8% and 17.1% in the pooled VELA analysis (delta of 18.7 percentage points).

While bimekizumab has since generated three-year follow-up data demonstrating durable efficacy and high draining tunnel resolution rates, sonelokimab has only reported 16-week and interim 52-week data. The narrative of inferiority stems more from market expectations misalignment than objective superiority of one molecule over another.

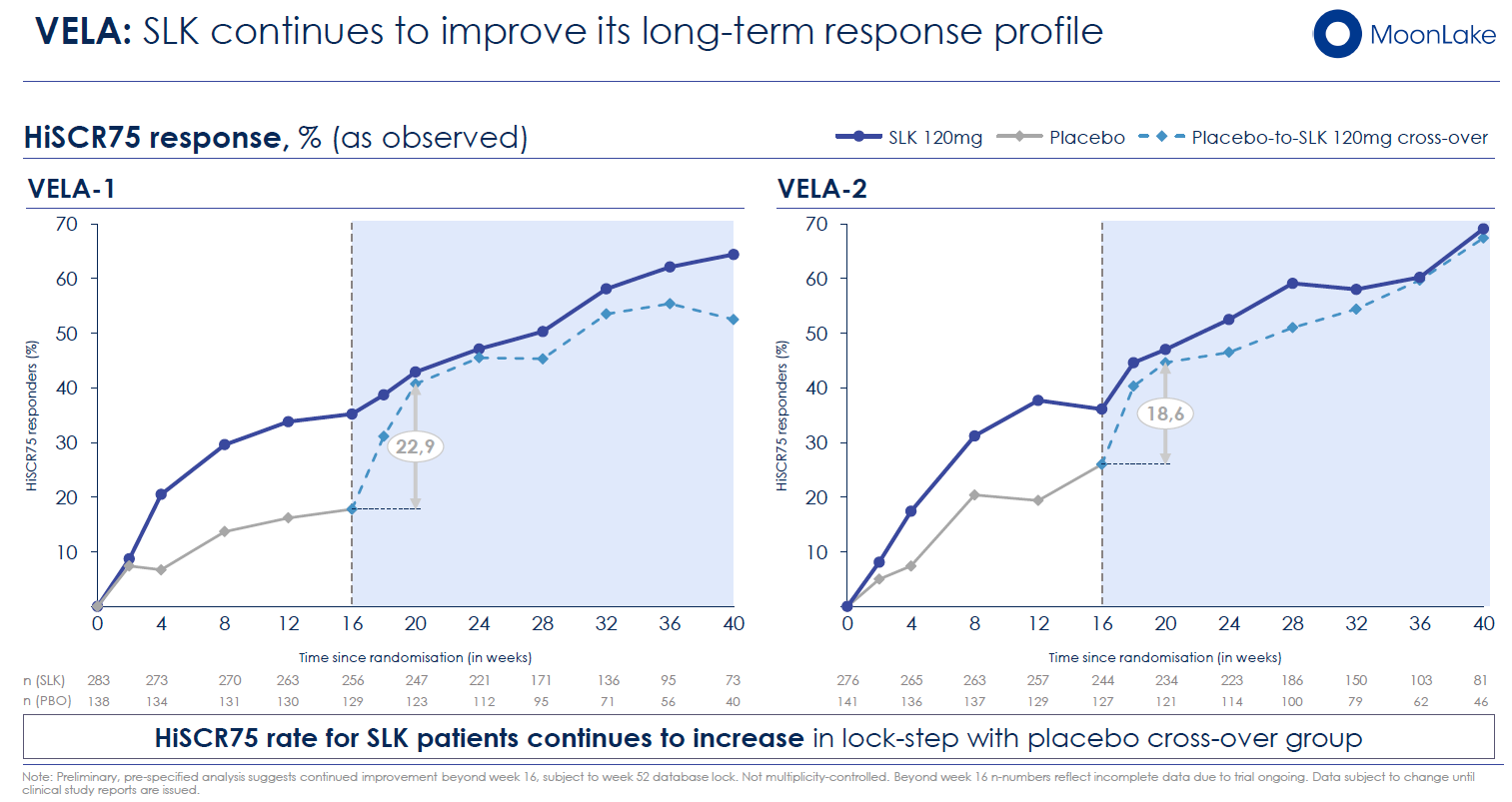

The 52-Week Trajectory: MoonLake's preliminary data presented in November 2025 show that sonelokimab's HiSCR75 response rate continues to build beyond week 16, reaching approximately 50%+ by week 24 in preliminary analyses. If this trajectory holds through 52 weeks (expected in Q2 2026), sonelokimab may demonstrate competitive or superior long-term efficacy compared to bimekizumab's established profile. The key point: final judgments should await the full 52-week dataset rather than being made on 16-week snapshots.

The Financial Fortress: Runway to Regulatory Clarity and Beyond

A critical factor distinguishing MoonLake from numerous failed biotech ventures is its exceptionally strong balance sheet—strength that management has deliberately maintained throughout the development crisis.

Cash Position and Capital Raise

As of September 30, 2025 (immediately before the Phase 3 announcement), MoonLake held $380.5 million in cash, cash equivalents, and short-term marketable debt securities. The company also secured a committed debt facility with Hercules Capital, providing additional capital access.

In early November 2025, with the stock trading in the $10 range (versus $62 pre-announcement), MoonLake executed a $75 million underwritten equity offering at $10.50 per share. While the dilution stings, the capital raise demonstrates that investors still see value sufficient to participate at these depressed levels. The net proceeds bring the total accessible capital to approximately $455+ million, providing runway well into H2 2027.

Burn Rate and Runway Mathematics

MoonLake's Q3 2025 R&D expenses totaled $60.6 million, up from $49.8 million in Q2 as the company ramped the Phase 3 VELA program and prepared for upcoming trials (IZAR-1/2 in PsA, LEDA in PPP, S-OLARIS in axSpA, and VELA-TEEN in adolescent HS). With operating expenses (R&D + G&A) trending toward $70–75 million per quarter at peak investment, the current cash runway extends approximately 18–24 months, easily covering critical catalysts through H2 2026.

This runway is not merely sufficient—it's luxurious by biotech standards. Most clinical-stage companies operating Phase 3 programs face constant capital constraints and dilution pressures. MoonLake's fortress balance sheet removes one of the most common risks: bankruptcy before regulatory clarity.

Capital Discipline

Management has explicitly stated they expect no major organizational growth following the VELA primary endpoint readout and view partnerships as unnecessary ("distractions"). This disciplined approach to capital allocation—spending what's needed to advance programs but not burning cash recklessly—is a hallmark of serious biotech stewardship. The company is not on a dilution treadmill despite the setback; it can afford to wait for longer-term data.

The Pipeline: A Multi-Indication Asset with Emerging Catalysts

Critically, MoonLake's story transcends hidradenitis suppurativa. Sonelokimab is being evaluated across multiple large-market indications, each with its own near-term catalyst and commercial potential.

Hidradenitis Suppurativa (HS): The Regulatory Gambit

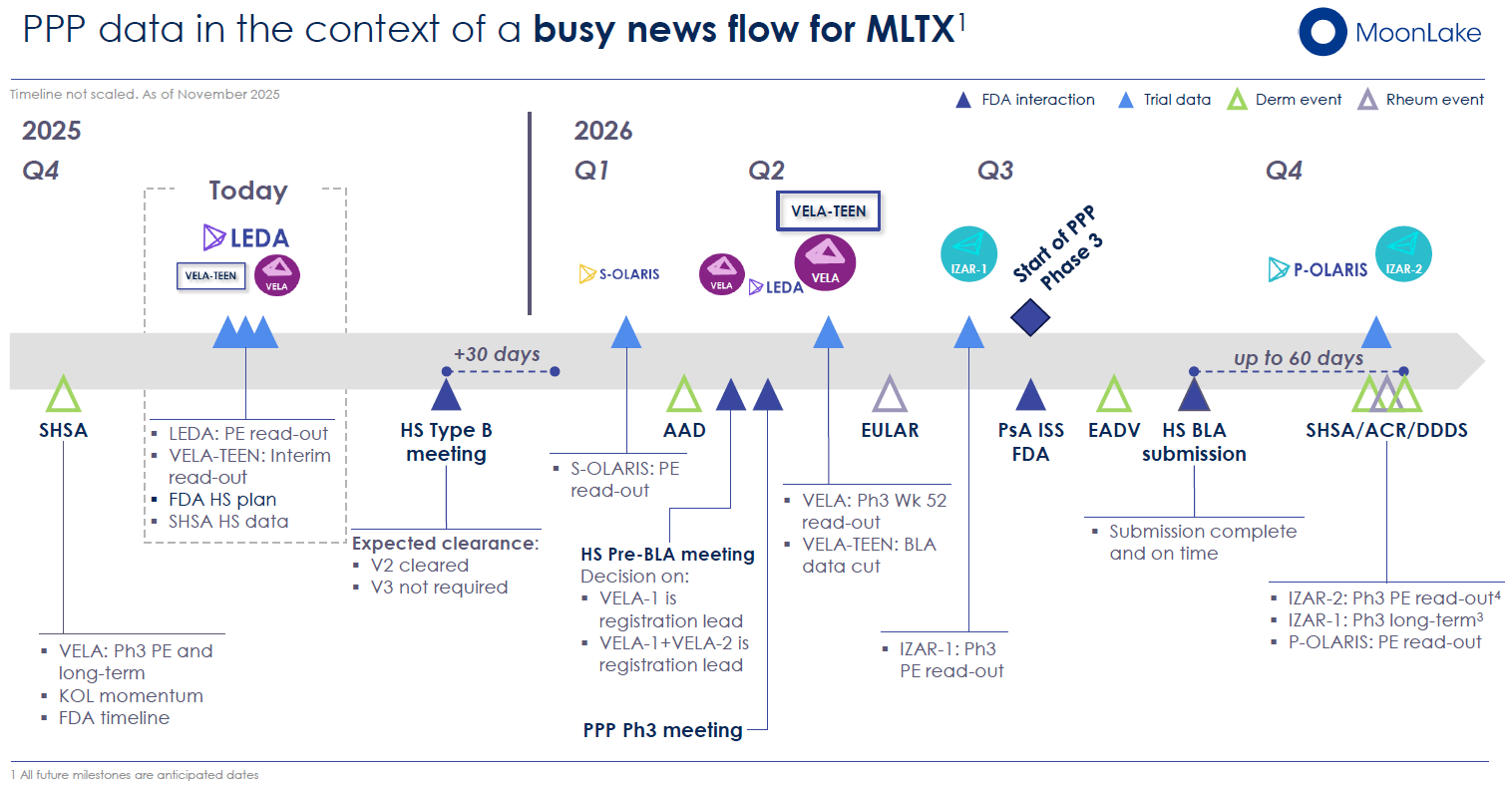

Upcoming FDA Type B Meeting (December 15, 2025)

MoonLake has scheduled a Type B meeting with the FDA for December 15, 2025, to discuss the adequacy of the clinical evidence package to support a Biologics License Application (BLA) in HS. Type B meetings, in FDA terminology, address specific scientific issues during drug development—in this case, whether the VELA dataset (combining VELA-1, VELA-2, and the Phase 2 MIRA trial) constitutes adequate evidence of efficacy and safety.

The meeting minutes (due within 30 days) will be pivotal. If the FDA signals confidence in the evidentiary package and provides guidance on an approvable regulatory pathway, the market could view this as a de facto green light for eventual BLA submission. Conversely, if the FDA raises concerns about VELA-2's primary endpoint failure or requests additional studies, expectations will reset downward.

Management has stated its belief that "the HS package should be approvable based on all relevant SLK data to date (incl. VELA and MIRA trial data), internal and external assessments, and precedents in HS." This is neither boastful nor dismissive—it reflects genuine legal and regulatory precedent. The FDA has previously approved drugs where one of multiple Phase 3 trials failed to meet the primary endpoint, provided the totality of evidence demonstrated efficacy and the failure could be explained (e.g., by methodological factors like elevated placebo response).

BLA Submission Timeline: Q3/Q4 2026

MoonLake plans to submit the BLA in Q3 2026 at the earliest, following 52-week data readout (expected Q2 2026). This timing provides the company with additional evidence of durability and long-term efficacy—critical factors in a regulatory submission. FDA review timelines for BLAs typically span 10–14 months (standard review) or 6 months (priority review), implying potential approval in mid-2027.

Market Opportunity: The HS market is estimated to reach $15 billion by 2035, with an addressable population of 2+ million patients in the US alone. Even a minor market share in this indication would generate substantial peak sales.

Psoriatic Arthritis: The Rheumatology Expansion

IZAR-1 and IZAR-2 Phase 3 Trials

MoonLake is advancing two large Phase 3 trials in PsA—IZAR-1 (targeting biologic-naïve patients) and IZAR-2 (targeting TNF-α inhibitor-inadequate-response patients). Combined, these trials enroll approximately 1,500 patients across multiple geographies. IZAR-1 is expected to report its primary endpoint (ACR50 response at week 16) in Q2 2026.

The Phase 2 ARGO trial demonstrated ~60% ACR50 response rates and robust MDA achievement—performance that positioned sonelokimab among leading IL-17 agents in PsA. If Phase 3 confirms these Phase 2 results, a supplemental BLA (sBLA) for PsA could follow, potentially filed in Q3 2027.

Market Opportunity: The PsA biologic market exceeds $8 billion annually and is growing. Sonelokimab could secure a meaningful share if it demonstrates superior pain control, joint preservation, and skin clearing compared to competitors.

Palmoplantar Pustulosis: The Orphan Jewel

Phase 2 LEDA Trial Success

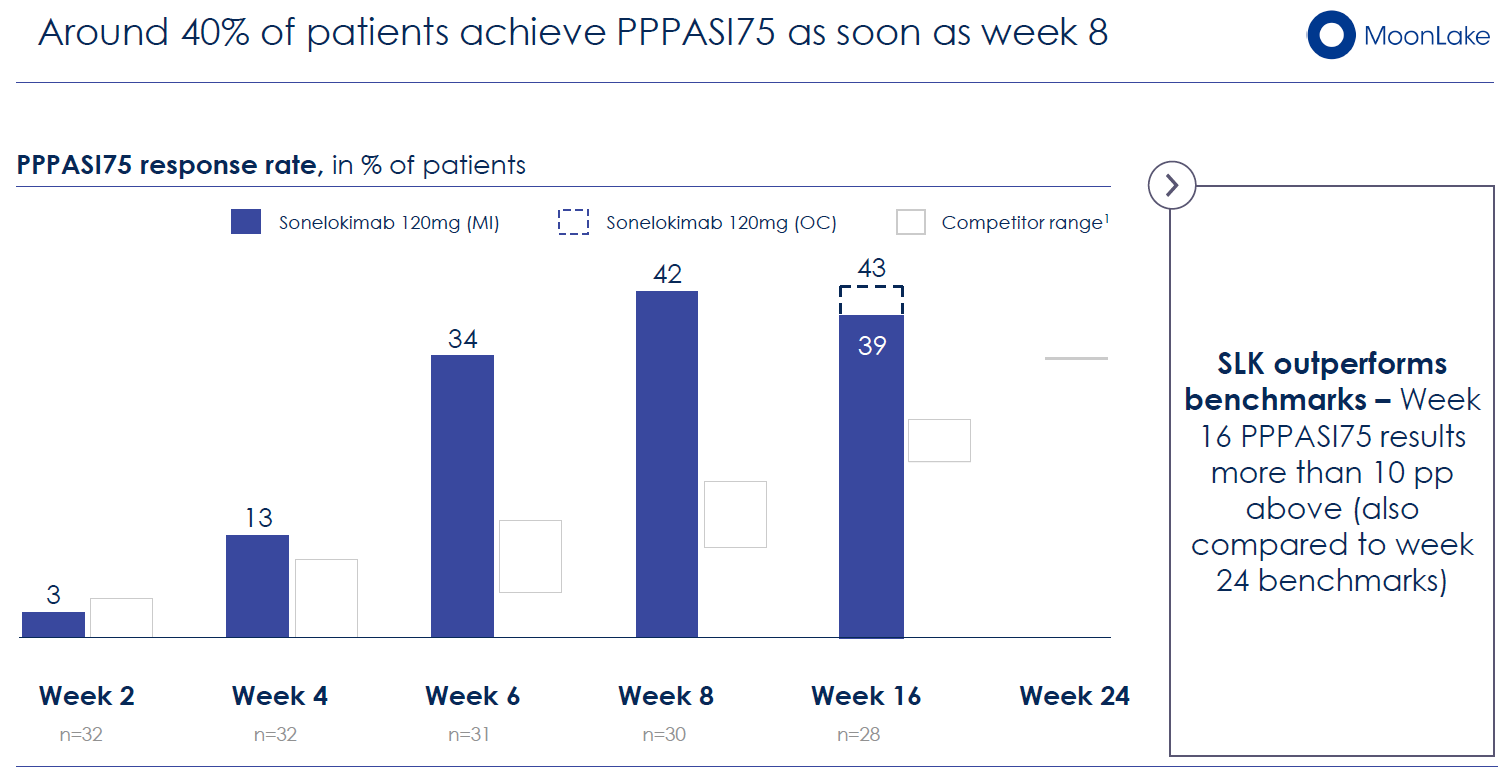

In November 2025, MoonLake presented compelling Phase 2 LEDA data in palmoplantar pustulosis (PPP)—a severely debilitating dermatologic condition affecting ~170,000 unique patients in the US. This indication represents perhaps the most compelling regulatory story within the pipeline.

Clinical Efficacy: In the open-label, 32-patient LEDA trial, sonelokimab demonstrated:

- 64% mean reduction in Palmoplantar Pustular Psoriasis Area and Severity Index (PPPASI) at week 16

- 39% of patients achieving ≥75% reduction in PPPASI (PPPASI75)—substantially exceeding historical benchmarks for competing molecules

- Rapid onset: reductions evident by week 4, with continuous improvement through week 24

Competitive Context: PPP has no approved therapies in the US or Europe. Previous Phase 2/3 trials of IL-36 inhibitors, TNF-α inhibitors, and other biologics have failed or produced modest results. Sonelokimab's ~40% PPPASI75 rate at week 16 compares favorably to competitor historical data (~20–35%).

Regulatory Pathway: MoonLake plans to initiate a Phase 3 trial in PPP in Q3 2026 and submit a BLA in Q3/Q4 2026 (potentially a separate indication or consolidated filing). For a rare indication with high unmet need and strong Phase 2 data, accelerated approval pathways (Breakthrough Therapy Designation, Fast Track) are plausible.

Market Opportunity: While PPP is smaller than HS or PsA, the market is projected to reach $4–5 billion by 2038 (assuming annual new patient diagnosis growth of ~6%). As the first-approved therapy, sonelokimab could capture a meaningful share of a nascent, rapidly expanding market.

Axial Spondyloarthritis: The S-OLARIS Innovation

Phase 2 S-OLARIS Study

The Phase 2 S-OLARIS trial represents a cutting-edge clinical trial design, incorporating PET imaging of sacroiliac joints and spinal inflammation alongside traditional clinical endpoints. This mechanistic, biomarker-rich approach will generate critical data about sonelokimab's ability to halt inflammatory bone formation—a hallmark of advanced axial spondyloarthritis.

The trial is expected to report its primary endpoint (change in 18F-NaF PET uptake) in Q1 2026. If positive, S-OLARIS could support an sBLA in axSpA and further differentiate sonelokimab in rheumatology based on imaging evidence of disease arrest.

Adolescent HS: VELA-TEEN

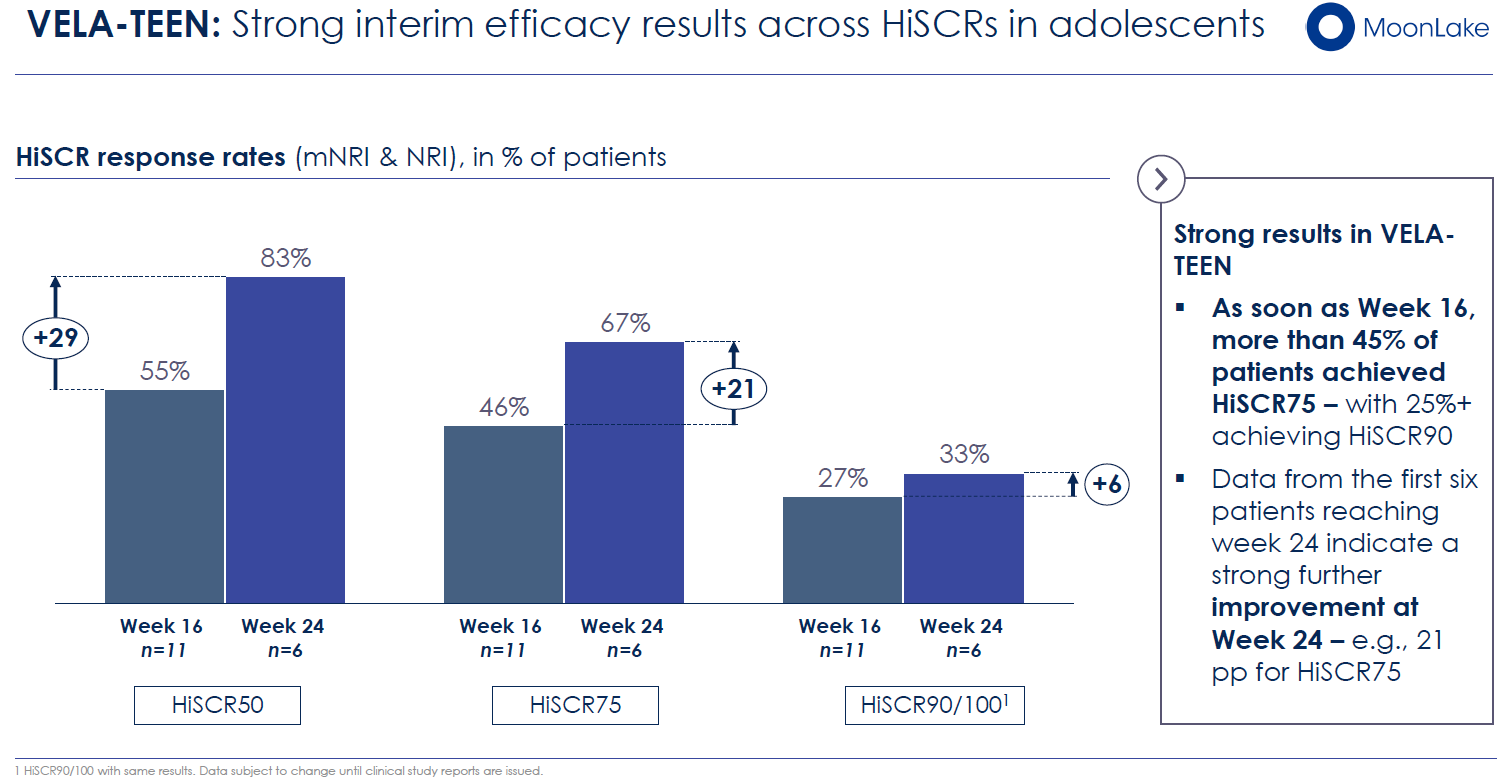

The Phase 3 VELA-TEEN trial, enrolling 30–35 adolescents (aged 12–17) with moderate-to-severe HS, represents an important pediatric expansion. An interim analysis presented in November 2025 showed 46% HiSCR75 response rates in 11 patients enrolled—consistent with adult VELA efficacy. Full results expected in Q2 2026, with the adolescent indication potentially included in the initial HS BLA submission.

The Catalyst Roadmap: A Clinical Trial Factory

MoonLake's forward calendar is densely packed with potential value drivers:

Immediate (Q4 2025)

- December 15, 2025: FDA Type B Meeting (HS)

Near-term (Q1–Q2 2026)

- Q1 2026: S-OLARIS Phase 2 primary endpoint (axSpA)

- Q2 2026: IZAR-1 Phase 3 primary endpoint (PsA)

- Q2 2026: VELA 52-week data (HS)

- Q2 2026: VELA-TEEN Phase 3 primary endpoint (adolescent HS)

Medium-term (Q3–Q4 2026)

- Q3 2026: Initiation of Phase 3 PPP trial

- Q3/Q4 2026: HS BLA submission (contingent on FDA feedback and 52-week data)

Mid-term (2026–2027)

- H2 2026: IZAR-2 Phase 3 primary endpoint (PsA)

- Mid-2027: Potential HS approval (if BLA approved on priority review timeline)

- Q3 2027: Potential HS sBLA approval (with adolescent and long-term data)

- Q3 2027: Potential PsA sBLA submission

This roadmap provides multiple inflection points where positive data could drive re-rating, while simultaneously reducing binary risk through portfolio diversification.

Risk Factors: Why the Comeback Narrative Could Derail

Despite the compelling thesis, substantial risks remain.

Regulatory Uncertainty

The FDA's December 15 meeting outcome is not guaranteed to be favorable. If the FDA signals concern about the VELA-2 primary endpoint miss and requires additional Phase 3 data, the BLA timeline could slip by 12–24 months, and the probability of eventual approval would decline materially. Securities litigation could also create distractions and regulatory uncertainty.

Clinical Trial Risk

Phase 2 success does not guarantee Phase 3 success, particularly in indications where patient selection, site variability, and placebo response can diverge between studies. The LEDA PPP trial enrolled only 32 patients; a larger Phase 3 trial may not replicate the robust efficacy observed.

Competitive Pressure

Bimekizumab (BIMZELX) has already achieved FDA approval and is generating real-world efficacy data. If bimekizumab demonstrates clear clinical or commercial superiority, sonelokimab may face a challenging competitive position even if approved. Additionally, other IL-17 or IL-23 competitors are advancing in HS, PsA, and other indications.

Capital Depletion

While MoonLake has substantial cash, a major trial failure or unexpected clinical hold could accelerate burn rates and force an unfavorable financing, diluting shareholders significantly.

Management Execution

The company's track record is short (founded in 2021, public since April 2022). While the team includes experienced biopharma veterans, execution risk remains higher than for established organizations.

Financial Valuation: From Rubble to Opportunity

At the September 29 low of $5.95 per share, MoonLake's market capitalization dwindled to roughly $377 million, marking the nadir following its dramatic Phase 3 data disappointment. As of early November 2025, the company’s market cap has stabilized at approximately $650 million, presenting investors with a profound inflection point for recalibrating expectations and reassessing risk versus reward.

Bull Case Valuation (Risk-Adjusted Scenario):

- HS (Hidradenitis Suppurativa) Approval: If sonelokimab secures FDA approval for HS by mid-2027 and achieves peak sales of $2–3 billion by 2032, the asset could deliver a net present value (NPV) in the range of $1.5–2 billion.

- PsA (Psoriatic Arthritis): Successful sBLA filing in late 2027 with projected peak sales of $1–1.5 billion would add another $400–700 million in NPV.

- PPP (Palmoplantar Pustulosis): With a BLA targeted for Q3/Q4 2026 and potential peak sales between $500 million and $1 billion, PPP could represent $200–400 million NPV.

- axSpA and Other Pipeline Assets: Early-stage assets (like axial spondyloarthritis) and future programs carry additional value, estimated at $100–200 million in NPV.

- Total Risk-Adjusted NPV: Aggregating these prospects, MoonLake’s pipeline could be valued between $2.2 and $3.3 billion, under optimistic but plausible assumptions. Given the current valuation of only $650 million, this suggests an upside potential of over 200–400% if key catalysts materialize.

Bear Case Valuation (Downside Scenarios):

- HS Approval Fails or Faces Major Setbacks (40% probability):

- If sonelokimab is rejected for HS or regulatory/commercial challenges prove insurmountable, the share price could fall to $1–2, corresponding to a market cap of $150–300 million.

- Modest Progress with Competitive/Regulatory Headwinds (30% probability):

- With a more conservative regulatory path and challenging competition, MoonLake could trade in the $8–15 range (market cap of $1.1–2 billion).

- Successful Execution Across Multiple Indications (30% probability):

- Outstanding clinical and regulatory execution could drive the share price to $25–50 and market cap toward $3.5–7 billion.

Probability-Weighted Outcome:

Weighting these scenarios, the expected return leans positive but continues to hold substantial downside risk. Investors must accept the stark binary nature of the upcoming regulatory and data catalysts. With an ample cash runway and a depressed valuation, MoonLake offers an asymmetric risk/reward landscape—potentially significant upside if it executes, but with notable risk if setbacks persist, especially for its lead HS asset.

Investment Thesis: The Asymmetric Opportunity

MoonLake presents a compelling asymmetric risk/reward opportunity for investors with moderate-to-high biotech risk tolerance and a multi-quarter investment horizon.

The Bull Case Synthesis

- Clinical Data Is Strong: While VELA-2's primary endpoint miss was disappointing, the combined VELA program demonstrates consistent, clinically meaningful efficacy across both trials. Secondary endpoints—pain, draining tunnel resolution, quality of life—differentiate sonelokimab and address the true patient burden of HS.

- Regulatory Pathway Is Plausible: The FDA Type B meeting in December will provide critical clarity. Historical precedent supports BLA approval even with one-of-two Phase 3 trial missing the primary endpoint, provided the totality of evidence is compelling. MoonLake's Phase 2 MIRA data and robust secondary endpoints in VELA strengthen the case.

- Financial Fortress Enables Patient Capital: With $380M+ in cash and a $75M capital raise completed, MoonLake can afford to wait for 52-week data, FDA feedback, and additional trial readouts. No forced financing or dilution should occur unless clinical trials fail catastrophically.

- Multi-Indication Pipeline De-Risks Execution: Sonelokimab's performance in PPP (Phase 2 success with first-mover advantage), PsA (large Phase 3 trials underway with strong Phase 2 precedent), and axSpA (mechanistic biomarker trial) provides optionality. Even if HS approval faces setbacks, the portfolio mitigates downside.

- Catalyst-Rich Roadmap Provides Near-Term Inflection Points: The December FDA meeting, Q1 2026 axSpA data, Q2 2026 PsA Phase 3 results, and subsequent 52-week HS data offer multiple opportunities for positive re-rating before any formal approval decisions.

- Valuation Reflects Extreme Pessimism: At $650M market cap, the stock prices in substantial failure risk. If management executes and achieves even modest regulatory success, 100–300% upside is plausible.

The Key Risks to Monitor

- FDA Meeting Outcome (December 15): An unfavorable meeting could trigger another significant selloff.

- Securities Litigation: While unlikely to derail the company fundamentally, litigation creates regulatory and management distraction.

- Competitive Dynamics: If bimekizumab establishes clear superiority and market dominance, sonelokimab's commercial prospects narrow.

- Phase 3 Trial Failures: Any major Phase 3 failure (e.g., IZAR-1 PsA miss) could force strategic reassessment.

The Broader Lesson: Binary Risk in Biotech

MoonLake's extraordinary rise and collapse encapsulates the extreme volatility inherent in clinical-stage biotech. The company's situation is not unique; similar dynamics have played out recently with companies like aTyr Pharma ($ATYR) and numerous others where binary clinical events create 70–90% single-day downside moves.

For investors, the lessons are clear:

- Pre-announcement euphoria often reflects unjustified confidence in clinical outcomes, particularly when external validation (activist investors, rumors of acquisition interest) creates tribal belief.

- Phase 2 success is not destiny. Phase 3 trials frequently produce unexpected results due to placebo response variability, site effects, and patient selection biases.

- Post-collapse re-rating can overcorrect. Markets often swing from irrational exuberance to irrational despair, creating opportunities for disciplined, contrarian investors.

- Management credibility, once lost, is not quickly recovered. However, strong clinical data and credible regulatory progress can rebuild confidence over time.

MoonLake's September 2025 collapse serves as a stark reminder that biotech investing requires conviction-based analysis decoupled from consensus euphoria—and willingness to reassess when data changes. The subsequent recovery narrative, however, demonstrates that setbacks don't always spell doom; sometimes they're simply recalibrations of expectations toward more realistic outcomes.

Conclusion: The Comeback Story Unfolds

MoonLake stands at a critical juncture. The September 28 Phase 3 announcement destroyed $3 billion in market value and triggered multiple securities investigations. Yet within weeks, additional clinical data, management clarity, and regulatory progress have begun to reshape the narrative.

The company's financial fortress, robust clinical secondary endpoints, multi-indication pipeline, and imminent FDA Type B meeting provide genuine catalysts for recovery. Sonelokimab may not be the "gold standard" for HS that management once claimed, but it appears to be a clinically meaningful treatment option in a severely underserved patient population—with potential in multiple other large-market indications.

For investors with conviction in the science, patience for regulatory timelines, and risk tolerance for binary outcomes, MoonLake at current valuations offers a compelling risk/reward asymmetry. The December FDA meeting will be the first major inflection point; successful outcomes there could trigger a significant re-rating and reestablish credibility with institutional investors.

The biotech comeback story may yet be written. Success, however, will require impeccable execution, regulatory alignment, and perhaps most importantly, a market willing to separate clinical reality from pre-announcement hype. The next six months will determine whether MoonLake's narrative is one of redemption or continued decline.

Disclaimer

The information provided on this website is for informational purposes only and should not be construed as

financial, investment, legal, or professional advice. While efforts are made to ensure accuracy, no guarantee

is given regarding completeness or reliability. Visitors should conduct their own research or consult a qualified

advisor before making any decisions. External links are provided for convenience and do not imply endorsement.