MoonLake (MLTX) Thesis Update: The Data Is Speaking — And It's Getting Louder

Last autumn, we published our original thesis on MoonLake Immunotherapeutics a month or so after the aftermath of a brutal selloff. The stock had cratered from $60s to under $7 following a messy Phase 3 VELA readout in September 2025 that confused the market — despite underlying science that looked fundamentally sound. Our thesis was simple: the market was pricing in failure, but the biology said otherwise.

Six months later, with Week 40 durability data, a blockbuster axSpA readout, FDA regulatory clarity, and a BLA submission on track for Q3 2026, the evidence has compounded in MoonLake's favour. This update lays out where the investment case stands today — the bull case, the bear case, and the catalysts that will decide which one wins.

Shares Outstanding: ~72.2 million Cash Position (Est. Q1 2026): ~$340 million Monthly Burn Rate: ~$20 million Analyst Consensus: Buy (12 Buy, 2 Sell) | Avg. PT: ~$27–$30 Next Earnings: May 7, 2026

The Original Thesis — Revisited

When we first covered MLTX, the stock had just experienced one of the most violent single-day collapses in recent biotech memory. The Phase 3 VELA-1 and VELA-2 trials of sonelokimab in hidradenitis suppurativa (HS) delivered mixed topline results: VELA-1 met its primary endpoint of HiSCR75 at Week 16, but VELA-2 did not — and the market sold first and asked questions later.

Our contrarian view was that investors were fixating on a binary primary endpoint miss while ignoring what the totality of the data showed: consistent efficacy signals across all secondary endpoints, quality-of-life improvements, and a safety profile that looked cleaner than anything else in the IL-17 class. The Nanobody platform was not broken. It just needed more time to show what it could do.

That time has now arrived.

Chapter 1: The Week 40 VELA Data — Science Speaks

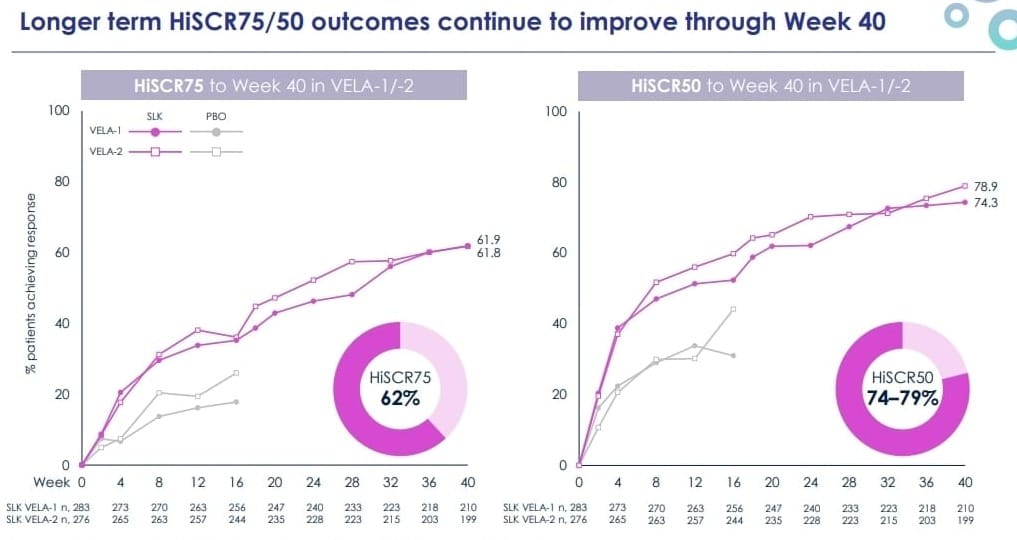

The most important development since our last coverage is the release of Week 40 data from the VELA-1 and VELA-2 Phase 3 trials during AAD 2026. For investors who held through the chaos, this data is the payoff.

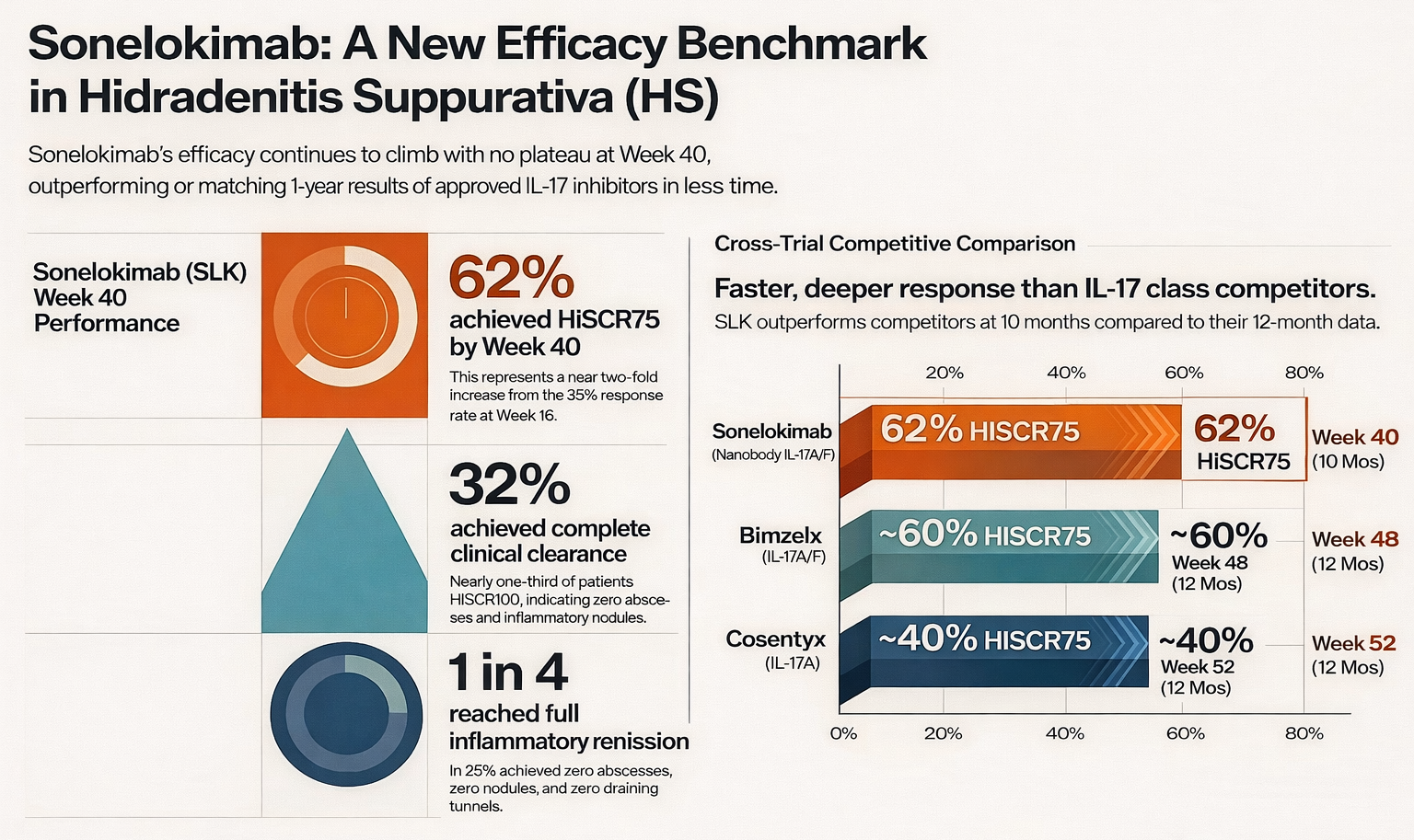

At Week 40 (approximately 10 months of treatment), 62% of sonelokimab-treated patients achieved HiSCR75 — a nearly two-fold increase from the ~35% response rate seen at Week 16. For context, HiSCR75 measures a 75% or greater reduction in abscesses and inflammatory nodules, which is a far more stringent bar than the HiSCR50 endpoint that was used to approve both Cosentyx and Bimzelx.

What makes this number compelling is not just its magnitude — it is the trajectory. Sonelokimab's efficacy is still climbing at Week 40. There is no plateau effect visible in the data, which is the single most important signal for durability. If this upward curve holds through the full 52-week readout expected around mid-2026, it will place sonelokimab firmly in best-in-class territory for HS.

Beyond the headline HiSCR75 number, the depth of response is notable. Up to 32% of patients reached HiSCR100 — meaning complete clinical clearance of abscesses and inflammatory nodules. One in four patients achieved full inflammatory remission (zero abscesses, zero nodules, zero draining tunnels). And 65% of patients reported a clinically meaningful improvement in their quality of life as measured by the Dermatology Life Quality Index (DLQI).

For HS patients — many of whom cycle through years of painful, disfiguring flares with inadequate treatment options — these are not abstract statistics. They represent a potential step-change in what treatment can deliver.

How Does This Compare to Approved Therapies?

Cross-trial comparisons always carry caveats (different patient populations, different baseline severities, different statistical methods). With that disclaimer clearly stated, the directional picture is informative.

Novartis' Cosentyx (secukinumab), an IL-17A inhibitor, achieved approximately 40% HiSCR75 at Week 52 in its pivotal SUNSHINE/SUNRISE trials. Sonelokimab is already at 62% at Week 40 — outperforming at an earlier timepoint on the same endpoint.

UCB's Bimzelx (bimekizumab), which like sonelokimab targets both IL-17A and IL-17F, achieved approximately 55–60% HiSCR75 at Week 48 in its BE HEARD trials (observed case analysis). Sonelokimab is matching or exceeding this threshold two months earlier, and responses are still deepening. Bimzelx excels in long-term data — its 3-year extension showed 81% HiSCR75 among responders — but sonelokimab's trajectory at 10 months suggests it could match or exceed these numbers at maturity.

The long-term data from MoonLake's own trials reinforces this. As-observed HiSCR75 response rates at the end of the VELA parental trial stood at 69% for VELA-1 and 67% for VELA-2, compared to 56% and 64% in Bimzelx's BE HEARD I and II trials, and 43% and 38% in Cosentyx's pivots.

The takeaway: sonelokimab is producing deeper, faster responses than the only two approved IL-17 class competitors in HS.

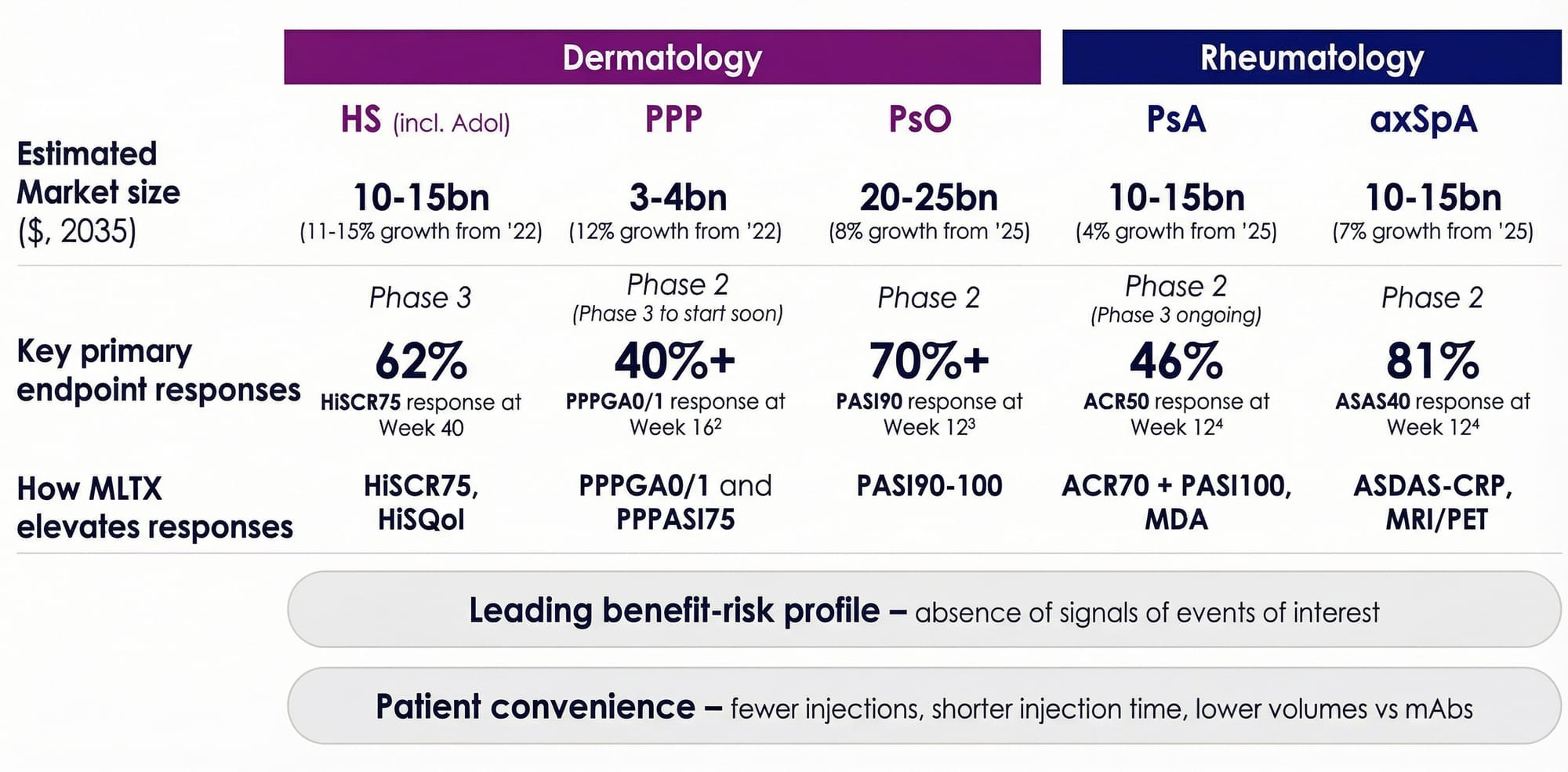

Chapter 2: Beyond HS — The Pipeline-in-a-Product Thesis Strengthens

One of the most compelling aspects of MoonLake's investment case is that sonelokimab is not just an HS drug. It is a single molecule targeting a combined addressable market that the company estimates at over $40 billion across five indications. MoonLake's February 2026 Investor Day laid out the multi-indication opportunity with striking clarity.

Axial Spondyloarthritis (axSpA): The S-OLARIS Stunner

The S-OLARIS Phase 2 readout in axSpA may be the single most impressive dataset MoonLake has generated to date — yet it has received relatively little attention from the market.

Axial spondyloarthritis is a chronic inflammatory condition affecting the spine and sacroiliac joints. It causes chronic back pain, stiffness, and in severe cases, irreversible spinal fusion. About 1.2 million unique patients have been diagnosed in the US over the past decade, but only 14% currently receive biologic treatment. Existing therapies achieve less than 50% symptom improvement in most patients, and none of them are truly disease-modifying.

In the S-OLARIS trial (n=26), sonelokimab produced results that genuinely stand out against the approved competition:

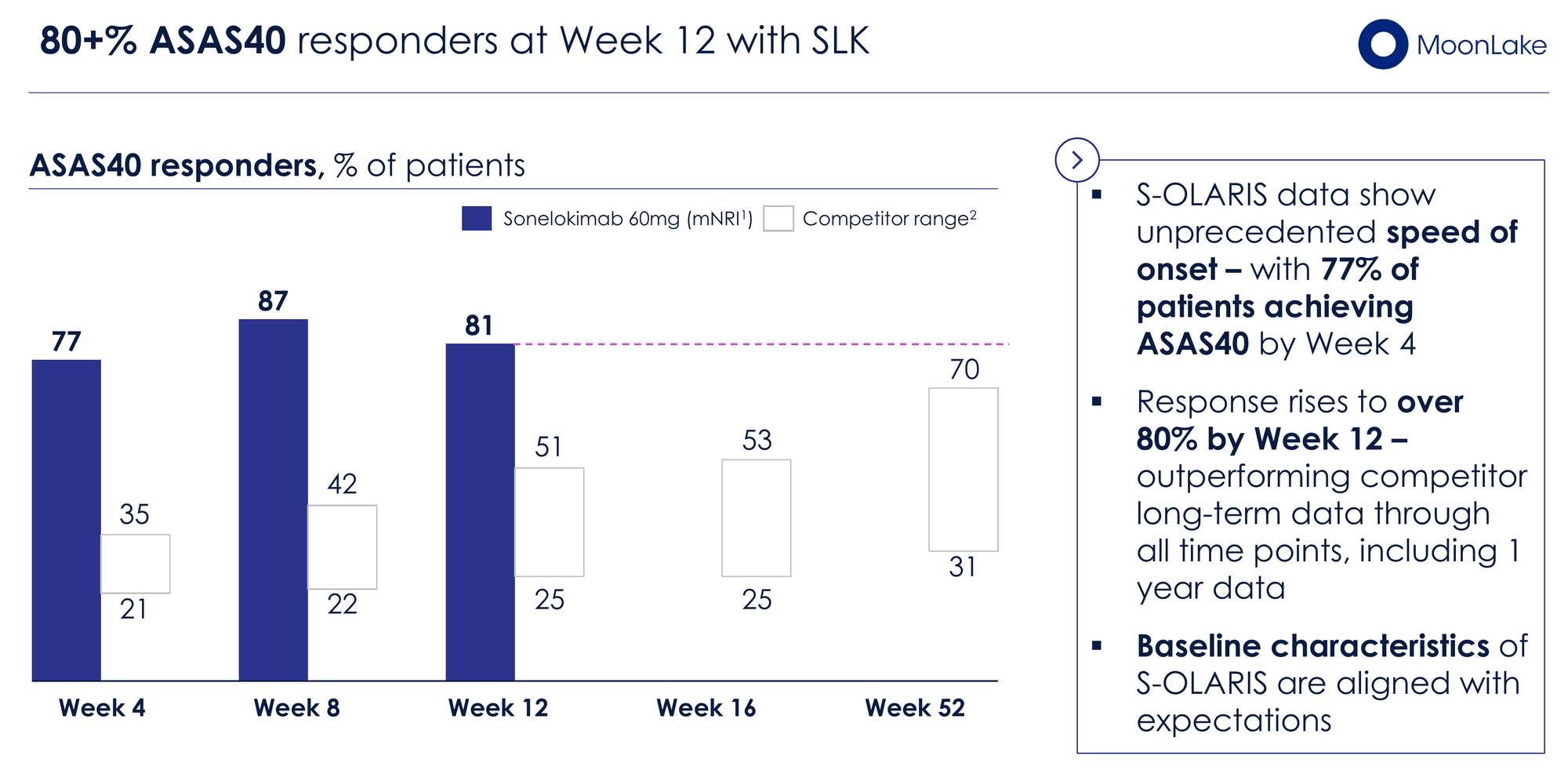

81% of patients achieved ASAS40 (a 40% improvement in symptoms) at Week 12 — compared to a range of 42–52% for approved biologics (Humira, Bimzelx, Cosentyx, Rinvoq, Taltz) at their primary endpoint timepoints of Week 12–16. Even more striking, 77% of patients hit ASAS40 by Week 4 — faster than any approved comparator's primary endpoint response.

~90% achieved a clinically important improvement in ASDAS-CRP score by Week 12, and 81% shifted to inactive or low disease activity by Week 4 — a level approximately 20 percentage points higher than 1-year open-label data from competitors in the same mechanism class.

But the real headline from S-OLARIS was the imaging data. Sonelokimab achieved a 21.8-point reduction in SPARCC MRI score in the sacroiliac joints — approximately a 90% reduction in inflammatory lesions, with 92% of patients achieving a decrease. Competitor MRI reductions at comparable timepoints ranged from 2.5 to 6.3 points.

Perhaps most significantly, PET imaging showed a 43% reduction in osteoblastic activity (bone remodeling) in the sacroiliac joints by Week 12. This is a signal for potential disease modification — addressing not just symptoms but the underlying structural damage that eventually leads to irreversible joint fusion. No other approved biologic in axSpA has demonstrated this in a clinical trial setting.

The small sample size (n=26) and open-label design are legitimate caveats. But the magnitude of the effect — 81% ASAS40 when the best approved drug manages 52% — is difficult to dismiss as an artifact of trial design.

The axSpA market alone is projected to reach $10–15 billion by 2035. If these results hold in larger trials, sonelokimab could become a paradigm-shifting therapy in the space.

Psoriatic Arthritis (PsA): The IZAR-1 Catalyst

The Phase 3 IZAR-1 trial in PsA (bio-naive and radiographic patients) has completed recruitment, with a primary endpoint readout expected in Q2/Q3 2026. This is one of the most significant near-term catalysts for MLTX.

Phase 2 ARGO data was encouraging: 46% ACR50 at Week 12 for both the 60mg and 120mg doses, compared to 20% placebo — a robust placebo-adjusted delta. For reference, Bimzelx achieved 44% ACR50 at Week 16 in its BE OPTIMAL trial (vs. 10% placebo).

However, PsA is a crowded space. There are over 12 approved therapies spanning TNF inhibitors, IL-12/23 blockers, IL-17A inhibitors, JAK inhibitors, and IL-23 inhibitors. Sonelokimab's commercial positioning depends on demonstrating superiority across multiple domains simultaneously — joints (ACR), skin (PASI), and composite endpoints like Minimal Disease Activity (MDA). MoonLake is betting that dual IL-17A/F inhibition can be the first therapy to break the treatment ceiling across all PsA domains.

IZAR-2 (bio-experienced patients, with a risankizumab reference arm) has a Q4 2026 readout. Together, these two trials will determine whether sonelokimab can claim a piece of the $10–15 billion PsA market.

PPP, Psoriasis, and the Full Platform

The LEDA Phase 2 trial in palmoplantar pustulosis (PPP) delivered strong results with over 40% of patients achieving PPPGA 0/1 at Week 16 and PPPASI75 response rates exceeding competitor benchmarks by more than 10 percentage points. PPP has no approved therapy in the US or Europe — this is a true greenfield opportunity in a market projected to reach $3–4 billion by 2035. Phase 3 is expected to start Q3 2026 with a faster Week 12 primary endpoint, backed by FDA Fast Track designation.

In psoriasis, Phase 2 data showed 70%+ PASI90 response at Week 12. In the VELA-TEEN adolescent HS trial, interim data showed 67% HiSCR75 at Week 16 — efficacy data in teenagers that no competitor has yet matched. UCB's Bimzelx is only now recruiting for a Phase 1 PK study in adolescents.

Across every indication MoonLake has tested, sonelokimab is producing leading or near-leading efficacy with a consistently clean safety profile. No signals for suicidal ideation (a Bimzelx label warning), no hepatic events, no IBD, and no dermatitis/eczema — areas where competitors carry explicit label warnings.

Chapter 3: The Regulatory Path Is Clear

One of the biggest overhang questions following the VELA-2 primary endpoint miss was whether MoonLake would need to run additional trials. The answer, confirmed via FDA Type B meeting in December 2025, is no.

The FDA provided clear guidance that MoonLake can establish Substantial Evidence of Effectiveness (SEE) using VELA-1 and MIRA (the Phase 2 trial in HS), with VELA-2 submitted for safety. All three trials are considered adequately and well-controlled — a regulatory advantage that competitors lack. Bimzelx's Phase 2 HS trial used a different dose than the approved commercial dose, and Cosentyx had no Phase 2 trial in HS at all, relying instead on an investigator-initiated trial to proceed to Phase 3.

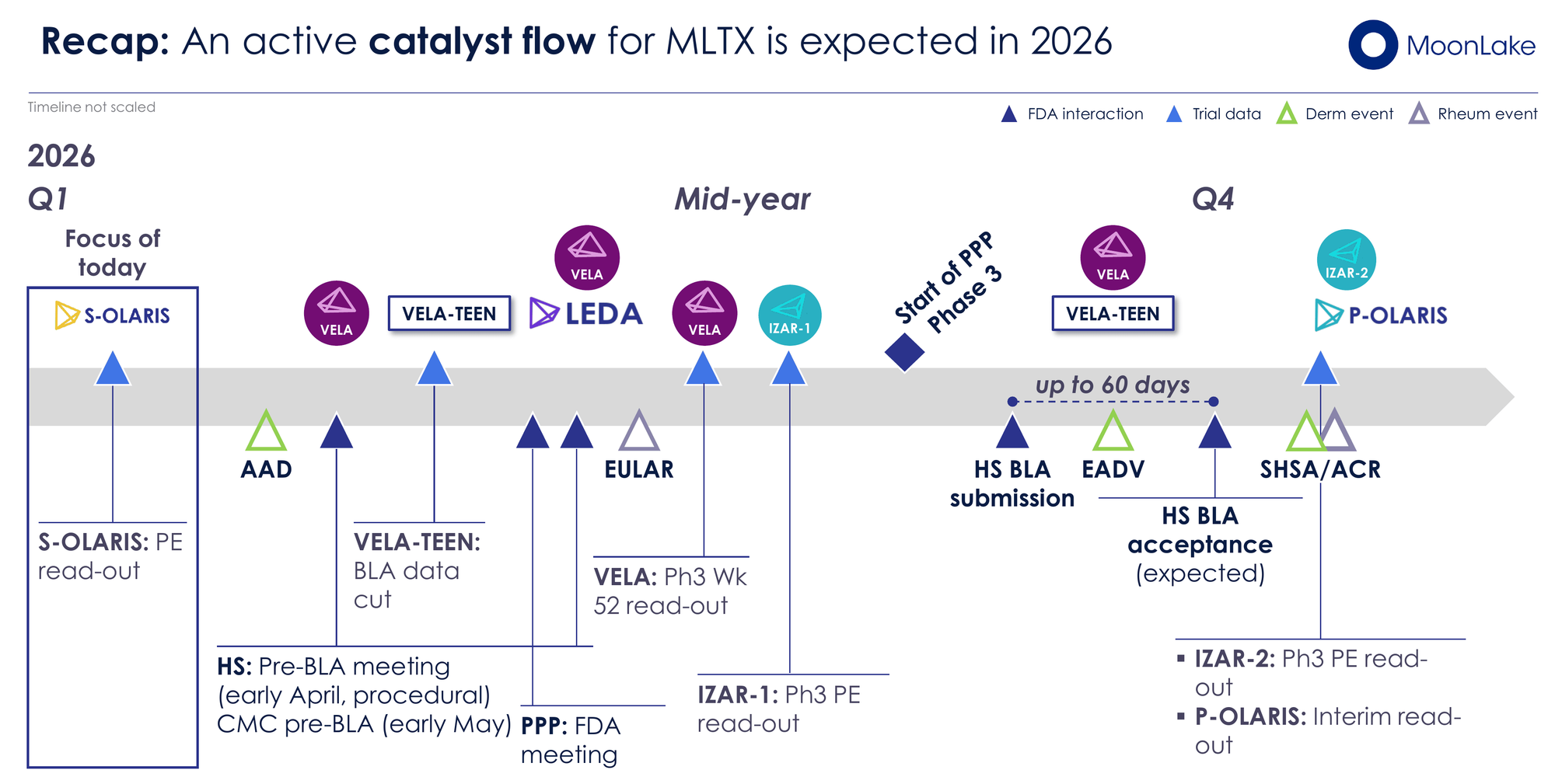

The BLA submission timeline remains on track for Q3 2026, with a pre-BLA meeting in early April and a CMC pre-BLA in early May. If accepted, FDA review would target a commercial launch in Q3 2027.

The potential label is where things get interesting. MoonLake's base case for Section 14 (Clinical Studies) includes HiSCR75 and HiSCR50 data from both VELA-1 and MIRA — numerically leading the comparable data on both Bimzelx's and Cosentyx's labels. In an upside scenario, additional endpoints (IHS4-55, Pain NRS-3, HiSQOL) could appear in the label, giving sonelokimab a richer efficacy section than any competitor. Bimzelx's HS label only includes HiSCR data.

On the dosing and safety sections, sonelokimab has meaningful differentiation potential: a shorter induction period (8 weeks vs. 16+ weeks for Bimzelx), lower injection volume (120mg vs. 320mg), fewer induction injections, and a cleaner safety profile without the suicidal ideation warning that weighs on Bimzelx's label.

Chapter 4: Financial Reality Check

This is where the cautious part of our cautiously positive thesis comes in. MoonLake is a pre-revenue clinical-stage company burning approximately $65 million per quarter (including non-cash expenses like stock-based compensation). At our estimated Q1 2026 cash balance of approximately $340 million, that provides roughly 5 quarters of operational runway — aligning with management's stated guidance of cash runway into the second half of 2027.

The company has been disciplined on capital management relative to peers. R&D expense peaked in Q3 2025 at $60.6 million and declined to $56 million in Q4 2025, with the VELA and S-OLARIS trials winding down. However, new expenses are coming: PPP Phase 3 initiation, pre-commercial build-out, and the BLA submission itself.

The Hercules Capital debt facility, amended in February 2026, provides significant non-dilutive firepower. The total facility offers up to $500 million, structured in milestone-based tranches: $75 million drawn at closing, $25 million at amendment, $50 million upon clinically meaningful VELA Week 52 data (with a minimum market cap of $1.5 billion), $50 million upon IZAR readouts, $100 million upon FDA BLA approval, and $200 million in additional capital subject to lender approval. The interest rate of 8.45% (WSJ Prime + 1.45%) is not cheap, but it preserves equity and provides a bridge to commercialisation.

That said, additional dilutive funding later this year or early 2027 to prepare for the SLK commercial launch remains a realistic scenario. At the current market cap of ~$1.2 billion, any equity raise would be meaningful. Investors should watch the Q1 2026 earnings call in May for updated cash guidance.

Chapter 5: The Competitive Landscape — And Why Buyout Logic Applies

Sonelokimab is entering an HS market that is growing rapidly. Bimzelx generated €2.22 billion ($2.6 billion) in total sales in 2025 — up from just €607 million in 2024 — and has already captured over 32% of the HS biologic market share within 10 months of its HS launch. UCB projects the HS market alone will reach $5 billion between 2025 and 2030. The HS biologics market grew 24% between October 2024 and October 2025.

MoonLake estimates peak sales of approximately $3 billion in the US alone for HS and PsA combined. Across the full platform (HS, PsA, axSpA, PPP, psoriasis), the company is targeting a combined addressable market exceeding $40 billion by 2035.

This brings us to the acquisition thesis. A clinical-stage company with a best-in-class or near-best-in-class molecule across five major inflammatory disease indications, a clean safety profile, a differentiated technology platform (Nanobody vs. traditional monoclonal antibody), and a BLA on file — sitting at a $1.2 billion market cap — is the textbook definition of a takeout candidate.

Consider: Bimzelx alone generated $2.6 billion in 2025 sales. If sonelokimab can capture even a fraction of that trajectory across multiple indications, the current market cap severely undervalues the platform. Large pharma companies with immunology franchises — Novartis, AbbVie, Eli Lilly, Johnson & Johnson, even UCB itself — would all have strategic rationale for acquiring this asset.

The key variable is 52-week VELA data. If Week 52 confirms durable, deepening responses without a plateau, the best-in-class narrative becomes very difficult for acquirers to ignore. If it disappoints — or if IZAR-1 in PsA fails — the acquisition premium shrinks considerably.

Chapter 6: The Bear Case — What Could Go Wrong

A balanced analysis requires confronting the risks directly.

IZAR-1 Execution Risk. PsA is highly competitive. Bimzelx achieved 44% ACR50 vs. 10% placebo in bio-naive patients (BE OPTIMAL). Sonelokimab's Phase 2 showed 46% ACR50 vs. 20% placebo — strong, but against a higher placebo rate. Phase 3 could compress this delta, particularly if the placebo rate in IZAR-1 trends higher than expected. A failure here would not kill the HS thesis but would significantly narrow the TAM story.

52-Week Plateau Risk. The entire thesis hangs on continued durability of VELA study for HS. If Week 52 data shows a levelling-off or decline in response rates, the best-in-class narrative weakens. HS is a disease characterised by flares — long-term response maintenance is critical.

Competitive Intensity. Bimzelx already has a head start in the HS market and is building commercial momentum rapidly. By the time sonelokimab launches (projected Q3 2027), Bimzelx could have 2+ years of real-world prescribing data and established payer relationships. Second-mover advantage only works if the clinical differentiation is clear enough to motivate physician switching.

Cash Runway and Dilution. At ~$20M/month burn, MoonLake has approximately 17 months of cash from current reserves. The Hercules facility provides non-dilutive bridge capital, but milestone tranches are conditional. The $50M tranche tied to Week 52 data requires a minimum market cap of $1.5 billion — which is above the current level. An equity raise at current prices would be dilutive.

Regulatory Uncertainty. The BLA pathway appears clear, but the FDA could request additional data, extend the review timeline, or issue a Complete Response Letter. The VELA-2 primary endpoint miss, while addressed via the MIRA-based SEE strategy, remains a potential point of contention during review.

Litigation Overhang. Multiple securities class action lawsuits were filed following the VELA readout stock decline. While these are common in biotech and rarely existential, they create noise and potential management distraction.

Chapter 7: Valuation — $10B+ Is Not Aspirational, It's What Pharma Pays

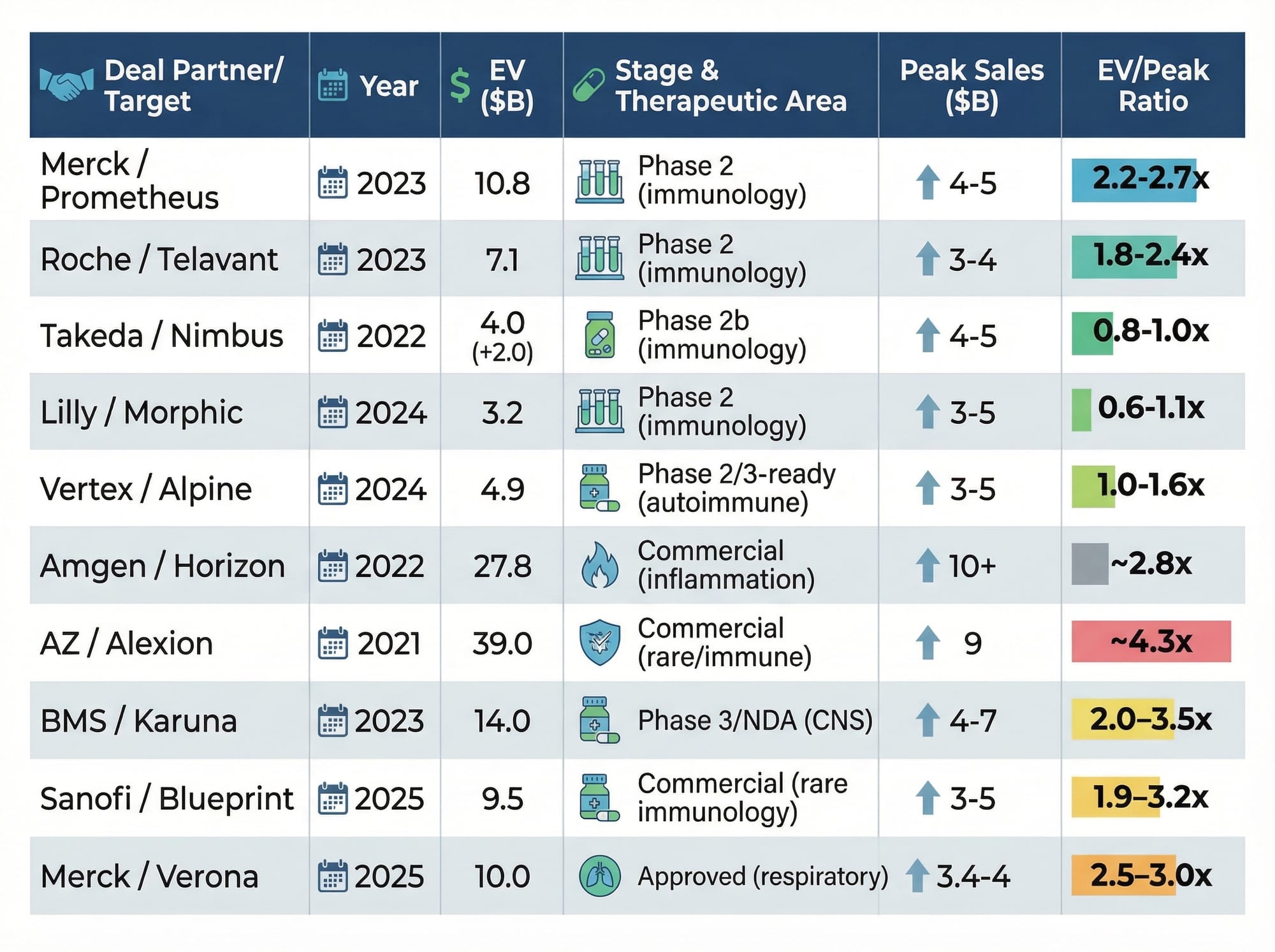

Let's ground this in what large pharma actually pays. Merck acquired Prometheus Biosciences (Phase 2, anti-TL1A) for $10.8 billion in 2023 — roughly 2.5x peak sales. That same year, Roche paid $7.1 billion for Telavant's competing asset, and BMS paid $14 billion for Karuna at Phase 3 stage. In 2025, Merck paid $10 billion for Verona Pharma at approximately 3x peak sales. The pattern is consistent: late-stage immunology assets transact at 2.5–3.5x peak sales.

MoonLake estimates approximately $3 billion in US peak sales from HS and PsA alone — before counting axSpA, PPP, or psoriasis. At a conservative 2.5x multiple on just that $3 billion figure, you arrive at $7.5 billion. At 3.0x on a fuller $4 billion multi-indication estimate, $12 billion. The current enterprise value of roughly $750 million prices sonelokimab at approximately 0.25x peak sales — a fraction of what every comparable transaction has commanded.

This is not theoretical. In June 2025, the Financial Times reported Merck submitted a non-binding offer exceeding $3 billion, which MoonLake rejected. That bid came before FDA regulatory clarity, before the Week 40 durability data, and before the S-OLARIS axSpA results. Every one of those catalysts has since moved in MoonLake's favour.

Our base-case target valuation is $10 billion+ by 2028 (~$140/share), assuming HS FDA approval (70–80% probability), initial commercial traction consistent with Bimzelx's launch trajectory, and at least one additional indication advancing toward registration. Bimzelx generated $2.6 billion in just its second full year across indications. If sonelokimab's best-in-class profile translates to even comparable uptake, $10 billion by its first full year of HS sales is what pharma routinely pays — not an aspiration.

Even in a downside scenario — narrower label, PsA failure, no M&A — the math implies $4–5 billion on HS alone, or roughly $56–70/share. The bull case, with best-in-class confirmation across HS, PsA, and axSpA, could push well above $15 billion.

Our Updated Assessment

The investment case for MLTX is meaningfully stronger today than when we first wrote about it. The Week 40 VELA data removes significant clinical risk. The S-OLARIS axSpA data validates the multi-indication platform thesis. FDA regulatory clarity de-risks the BLA timeline. And the Hercules facility provides a non-dilutive bridge toward commercialisation.

At a $1.2 billion market cap, the market is essentially pricing sonelokimab's HS opportunity alone at a steep discount — and attributing near-zero value to the axSpA, PsA, PPP, and psoriasis opportunities. If any two of these indications succeed, the current valuation looks very conservative.

The key catalysts to watch in 2026, in order of significance:

- VELA Week 52 Data (mid-2026) — The make-or-break readout for the best-in-class HS narrative

- IZAR-1 PsA Phase 3 Readout (Q2/Q3 2026) — Validates or narrows the multi-indication story

- HS BLA Submission (Q3 2026) — Regulatory milestone that triggers Hercules tranches and starts the FDA review clock

- IZAR-2 PsA Phase 3 Readout (Q4 2026) — Second confirmatory PsA dataset

- Pre-BLA and CMC FDA Meetings (April/May 2026) — Procedural but confirms no surprises

We maintain a cautiously positive stance. The science is increasingly undeniable. The financial constraints are real but manageable. And the acquisition logic only gets stronger with each positive data readout. In biotech, clinical data is the ultimate truth-teller — and MoonLake's data is speaking loudly.

The stock is trading near its 52-week lows at ~$16.80 against our base-case target valuation of $10 billion+ (~$140/share) by 2028. For investors with appropriate risk tolerance and a 12–18 month horizon, the risk/reward setup is asymmetric in a favourable direction. Merck's rejected $3 billion bid now looks like a lowball attempt to exploit a temporary dislocation — the real question is not whether sonelokimab gets acquired, but at what price. Our valuation target is conditional on successful FDA approval and continued validation of positive clinical outcomes with upcoming trial readouts. Moreover, retail investors must always acknowledge the inherent risks associated with biotech investments. Even minor deviations in future data readings can lead to market disappointment. Therefore, it’s crucial to set exit strategies and consider hedging to minimize potential losses in worst-case situations.

This article is independent research published on BiostockInfo.com and does not constitute financial advice. The author may hold positions in securities discussed. Always conduct your own due diligence before making investment decisions. Past performance is not indicative of future results.

Original thesis: MoonLake (MLTX): From Collapse to Recovery Play — The Nanobody Rebound Story

Data sources: MoonLake Investor Day Presentation (February 23, 2026), MoonLake press releases, SEC filings, ClinicalTrials.gov, UCB annual results (FY 2025), Novartis public disclosures, FDA labels for Bimzelx and Cosentyx.