T-Cell Engagers (TCE): The Race to Reset the Immune System — And the Biotechs Positioning to Win

Big Pharma is betting $10B+ that T-cell engagers can reboot the immune system. Here's the science, the money trail, and the biotechs worth watching.

Billions of dollars are flooding into a single idea: that a short course of an off-the-shelf biologic drug could induce durable, drug-free remission in diseases like lupus, rheumatoid arthritis, and multiple sclerosis — not by suppressing the immune system, but by rebooting it entirely. Here's the science, the money trail, the companies worth watching — and the risks nobody wants to talk about.

The $110 Billion Problem That Nobody Has Solved

Your immune system is the most sophisticated defence network in biology. It identifies and eliminates viruses, bacteria, and malignant cells with extraordinary precision. But in roughly 50 million Americans — and an estimated 800 million people globally — this system suffers a catastrophic miscalibration. The body's own healthy tissues get flagged as foreign invaders. The immune system launches a relentless, chronic assault on the host.

At the centre of this "friendly fire" are B cells. In a healthy immune system, B cells are factories that produce antibodies to neutralise threats. But in autoimmune diseases — systemic lupus erythematosus (SLE), rheumatoid arthritis (RA), Sjögren's disease, multiple sclerosis, myasthenia gravis — corrupted B cells produce autoantibodies. These pathogenic proteins bind to the patient's own DNA, joint tissue, or organs, triggering cascading inflammation and irreversible damage.

For decades, the medical response has been crude. Broad-spectrum immunosuppressants like prednisone and methotrexate act like carpet-bombing campaigns — suppressing the entire immune system to dampen the autoimmune attack while leaving patients vulnerable to infections, osteoporosis, cardiovascular disease, and secondary cancers. Even the arrival of targeted biologics like rituximab (anti-CD20) in the early 2000s didn't solve the problem. Rituximab kills mature circulating B cells, but the CD20 protein it targets is absent on early stem cells and, critically, on the long-lived plasma cells that actually produce the pathogenic autoantibodies. Rituximab acts like a lawnmower — trimming the visible disease while leaving the biological roots intact. Patients relapse. They cycle through therapies. The disease grinds on.

The autoimmune therapeutics market exceeds $110 billion annually. Humira alone peaked at $21 billion per year. Yet most patients never achieve sustained, drug-free remission. The unmet need is staggering, the patient population enormous, and for decades, the therapeutic ambition was limited to management, not cure.

That ambition just changed.

The Immune Reset: When Rheumatology Met Oncology

In the fall of 2022, a rheumatologist named Dr. Georg Schett at the University of Erlangen-Nuremberg did something audacious. He took a technology designed to cure terminal blood cancers — CAR-T cell therapy — and gave it to young lupus patients who had run out of options.

CAR-T is cellular engineering. You extract a patient's own T cells (the immune system's assassins), ship them to a specialised lab, genetically reprogram them to seek and destroy cells expressing a specific surface protein, then infuse the "living drug" back into the patient. Schett's team engineered CAR-T cells to target CD19 — a protein expressed across a much broader range of the B cell lifecycle than CD20, from early precursors through to plasmablasts. The goal was total B-cell annihilation.

The results were extraordinary. Following a single infusion, patients achieved complete, drug-free remission. Disease activity scores dropped to zero. Autoantibodies disappeared. And here's where it got truly remarkable: several months after the engineered T cells cleared the corrupted B-cell population and naturally faded from the body, patients' bone marrow began producing new, naive B cells. These fresh B cells were healthy — they didn't carry autoimmune programming. The patients could mount normal responses to vaccines. The immune system had been rebooted.

This introduced the concept of the "immune reset" — the theory that if you achieve B-cell depletion so deep and absolute that the disease-causing immunological memory is wiped out, the immune system effectively reinstalls a clean operating system. The implication was profound: autoimmune diseases, long considered chronic and incurable, might be sent into lasting drug-free remission with a one-time treatment.

But here's the problem. CAR-T is a logistical and financial nightmare. Manufacturing is bespoke — each patient's cells must be extracted, genetically engineered over weeks, and shipped back. A single infusion costs north of $500,000. Patients require harsh lymphodepleting chemotherapy beforehand — a massive ethical barrier for non-terminal autoimmune patients. And because CAR-T cells are alive and replicating, their activity can spiral out of control, triggering Cytokine Release Syndrome (CRS) — a massive inflammatory storm that can cause organ failure — or ICANS (neurotoxicity causing seizures and brain swelling). You can't simply "stop the dose" when the drug is a living cell multiplying in the bloodstream. Large-scale meta-analyses of CAR-T recipients have found an overall secondary malignancy rate of approximately 6% — and while the specific risk of lentiviral insertional oncogenesis proved exceedingly rare, it's a risk category that protein-based drugs like TCEs bypass entirely.

CAR-T strongly validated the biology. But it can't scale. The autoimmune market needs millions of treatments, not thousands. Enter the T-cell engager.

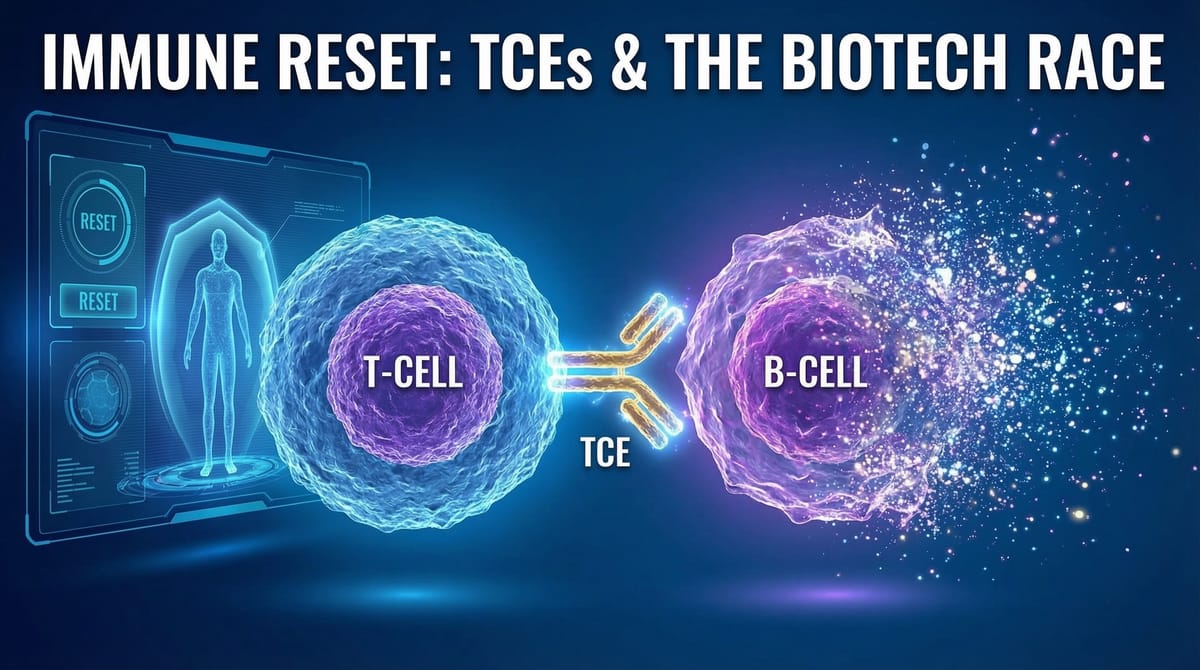

T-Cell Engagers: The Off-the-Shelf Immune Reset

A T-cell engager (TCE) is a bispecific antibody — a laboratory-engineered protein with two distinct arms designed to grab two completely different targets simultaneously. One arm binds to a surface antigen on the pathogenic B cell (CD19, CD20, or BCMA). The other arm binds to a receptor on the patient's own circulating T cells (typically CD3).

By physically tethering a T cell directly to a rogue B cell, the TCE forces the formation of an immunological synapse — an artificial kill junction. The T cell, tricked into believing it's found a valid target, punches holes in the B cell membrane with perforins and injects granzymes that trigger immediate apoptosis.

The advantages over CAR-T are dramatic. TCEs are mass-produced in bioreactors — standard pharmaceutical manufacturing, available off-the-shelf. They're administered via IV infusion or subcutaneous injection. No cell extraction. No genetic engineering. No weeks of waiting. No chemotherapy preconditioning. And critically, because a TCE is a standard protein drug with a predictable half-life, if a patient develops CRS, the physician simply stops the infusion and the drug clears from the system. You control the off-switch — something CAR-T fundamentally lacks.

Estimated treatment costs for a TCE course: $5,000–$50,000 versus $400,000+ for CAR-T. The scalability difference alone represents a potential 100x expansion of the addressable patient population.

The market has noticed.

Follow the Money: $10 Billion and Counting

Since mid-2024, over $10 billion in deal value has been committed to TCE and bispecific autoimmune assets. Over 40% of all pharma multispecific antibody deals from July 2024 through June 2025 targeted autoimmune and inflammatory diseases. The deal pace is accelerating.

Several patterns stand out. Upfront payments are large and rising — Merck paid $700M before a single autoimmune patient was dosed. That's pharma expressing conviction, not hedging. The China-to-global licensing pipeline is dominant: most TCE assets originated from Chinese biotechs (Curon, Chimagen, Antengene, Genrix, Harbour BioMed), reflecting China's early investment in bispecific engineering. And the diversity of approaches — CD19, BCMA, dual-target trispecifics, masked TCEs, myeloid cell engagers — signals pharma is hedging across strategies rather than converging on a single winner.

The Target Debate: CD19, BCMA, CD20, or All Three?

This is where the science gets really interesting for investors — and where the wrong bet could mean the difference between a blockbuster and a write-off. The choice of what protein your TCE grabs on the B cell surface is the single most consequential design decision in this entire field. Here's why.

B cells mature through stages: pro-B cells → pre-B cells → immature B cells → mature naive B cells → memory B cells → plasmablasts → long-lived plasma cells. Different surface proteins appear and disappear at different stages, and the target your TCE binds determines which stages get eliminated.

CD19 is the gold standard for broad depletion. It's expressed from the earliest pro-B cell stage through plasmablasts — nearly the entire B-cell lineage. CD19 was the target in Schett's landmark CAR-T trials. The limitation: CD19 is absent on most long-lived plasma cells. In the Erlangen blinatumomab programme (expanded to 14 patients with refractory RA by ACR 2025), CD19 TCE treatment achieved remission in 9 of 14 at month 3 — but 12 of 14 relapsed at a median of ~5.5 months, likely because surviving CD19-negative plasma cells continued producing pathogenic autoantibodies. That near-universal relapse rate raises a hard question: can single-course CD19 targeting alone deliver durable RA remission without sequential BCMA treatment? CD19 TCEs are also the most crowded space, with at least seven companies pursuing clinical programs.

BCMA (B-Cell Maturation Antigen) targets the other end of the spectrum — almost exclusively expressed on plasmablasts and long-lived plasma cells. Think of BCMA as a sniper rifle aimed directly at the autoantibody factories. Academic data with J&J's teclistamab (BCMA×CD3, approved for myeloma) in 10 patients with six different refractory autoimmune diseases showed clinical benefit in 9 of 10, with 6 of 10 achieving drug-free remission (with follow-up of up to ~15 months so far) and autoantibody seroconversion across conditions including lupus, scleroderma, Sjögren's, and inflammatory myopathy. CRS occurred in 8 of 10 patients but was mild; no neurotoxicity was reported. All patients developed hypogammaglobulinemia requiring monitoring. More durable than CD19-only results in RA, but small numbers and short follow-up demand caution.

CD20 targets mature circulating B cells — the same target as rituximab but achieving deeper depletion by recruiting T cells. Considered insufficient for curative immune reset in severe disease given its narrow expression range.

Multi-target approaches represent the emerging frontier. GSK's CMG1A46 hits both CD19 and CD20 simultaneously. Candid Therapeutics is developing both a dual CD19/CD20 trispecific and a BCMA+CD19 combination.

The investment implication: companies with both CD19 and BCMA TCEs are strategically positioned to tailor therapy by disease mechanism. Single-target companies face greater risk of being suboptimal for certain indications.

The CD3 Bottleneck: The Elephant in the Room

Here's where understanding the science gives investors a genuine edge.

Almost every TCE in clinical development grabs T cells via the CD3 receptor on conventional alpha-beta (αβ) T cells — roughly 95% of circulating T cells. This creates two problems.

Problem 1: Cytokine Release Syndrome. When αβ T cells are artificially activated by CD3-binding TCEs, they dump massive quantities of IL-6 into the bloodstream. To prevent lethal CRS, engineers are forced to "de-tune" the CD3 binding arm — intentionally weakening the TCE's grip. This creates a narrow therapeutic window: too weak and B cells survive; too strong and the patient crashes. Constantly pushing sub-optimal stimulation also risks T-cell exhaustion — the effector cells become fatigued and stop killing before the job is done.

Problem 2: Tissue Penetration. αβ T cells patrol the blood and lymphatic system but are notoriously poor at penetrating dense organ tissues. In autoimmune disease, the most destructive B cells aren't floating in the blood — they're sequestered deep inside inflamed organs: joints in RA, kidneys in lupus nephritis, salivary glands in Sjögren's. If your TCE relies on αβ T cells, you're running highway patrol while the real threat is hiding in the buildings.

Companies are engineering around these limitations — Merck's CN201 achieved only 7% CRS via ultra-low-affinity CD3 binding; UCB's ATG-201 uses steric masking that only activates the CD3 arm when CD19 binds first; subcutaneous formulations create gentler immune activation. These are clever solutions to a fundamental biological constraint.

But some developers are asking a different question entirely: what if you skip CD3 altogether?

Beyond CD3: Gamma-Delta T Cells and Why They Matter

Gamma-delta (γδ) T cells represent just 1–5% of circulating T cells. They're rare — but in biology, rare often means specialised.

Unlike conventional αβ T cells, γδ T cells are MHC-independent — they directly recognise markers of cellular stress without waiting for formal antigen presentation. Immunologists call them "nature's CAR-T cells" — and the nickname isn't just cute, it's functionally accurate. Critically, γδ T cells secrete vastly lower levels of IL-6 when activated, potentially eliminating the CRS bottleneck. And while the Vδ2+ subtype circulates in blood, the Vδ1+ subtype is programmed for tissue residency — naturally homing deep into epithelial and organ tissues where autoimmune B cells hide. This directly addresses both CD3 limitations in one biology.

IN8bio (NASDAQ: INAB) is the most advanced company pursuing the γδ-T cell engager approach. Its lead asset, INB-619, is a preclinical CD19-directed pan-γδ T cell engager designed to activate the γδ-TCR rather than CD3, with a proprietary Gamma Delta Expansion Domain (GDED) intended to expand both Vδ1 and Vδ2 γδ T-cell subsets and address the natural scarcity of these effector cells. Company-presented preclinical data suggest INB-619 can drive deep B-cell depletion, including in lupus patient-derived PBMC settings referenced across its materials, while showing relatively low induction of cytokines such as IL-6 and IL-10 compared with the cytokine liability typically associated with CD3-based TCEs.

The science is genuinely differentiated. But INB-619 is preclinical only, IND not expected until 2027, and IN8bio's cash runway extends only to H1 2027 after a $20.1M financing tranche. IGM Biosciences — which also had compelling preclinical theory — saw its TCE completely fail to deplete B cells in humans, forcing the company to halt all autoimmune programs and cut 73% of staff. The γδ approach is still a theory, a good one but needs a proof.

The Risk Register: What Could Go Wrong

Every compelling biotech thesis comes with an asterisk. Here's the honest accounting.

CRS remains the gating safety concern. Early autoimmune data is more favourable than oncology (lower target antigen burden), but Grade 3 events have occurred. KOLs consider Grade 2 CRS rates ≤10% acceptable for autoimmune populations. The Q2 2026 Cullinan readout will be the first real test.

Infection risk from deep B-cell depletion is real. In myeloma patients treated with BCMA TCEs, all-grade infections affected 50% — though myeloma patients have deeply compromised immune systems by definition, making this a poor direct proxy for autoimmune populations receiving short-course treatment. Hypogammaglobulinemia requiring IgG supplementation is expected regardless, adding cost and logistics that partially offset the "cheaper than CAR-T" narrative.

The regulatory pathway is uncharted. No TCE has been approved for any autoimmune indication. It's unclear whether FDA will accept biomarker-driven endpoints for accelerated approval or require traditional multi-year outcome trials.

Durability of response is the critical unknown. Expanded ACR 2025 data from the Erlangen blinatumomab RA programme showed remission in 9 of 14 patients at month 3, but 12 of 14 relapsed over time at a median of ~5.5 months — a near-universal relapse rate that raises serious questions about whether single-course CD19 TCEs are viable for RA at all without sequential BCMA treatment. Whether re-dosing, sequential strategies (CD19 followed by BCMA), or maintenance approaches are needed remains the defining clinical question for the field.

Competition is extraordinarily intense. Seven-plus large pharma companies and numerous biotechs are pursuing TCEs simultaneously, plus CAR-T competitors and in vivo CAR-T approaches. Not all formats will work — the IGM Biosciences collapse proved that. Differentiation via safety profile, subcutaneous convenience, and target selection will determine winners.

Not every autoimmune patient is equally B-cell driven. Diseases like SLE and RA are biologically heterogeneous — some patients are predominantly driven by pathogenic B cells and autoantibodies, others by T-cell or innate immune mechanisms. Response durability may vary significantly by disease biology and patient subset, so early readouts may not generalise across all autoimmune settings.

Biotechs Worth Following in the TCE Autoimmune Space

Here's the landscape mapped by tier — from the clinical pure-plays with the most asymmetric upside to adjacent competitors pushing different modalities toward the same goal.

Tier 1: Clinical-Stage Pure Plays

Cullinan Therapeutics (NASDAQ: CGEM) —The bellwether. Only public company targeting both CD19 and BCMA for autoimmune diseases. Lead asset CLN-978 (CD19×CD3, subcutaneous) running Phase 1 OUTRACE trials in SLE, RA, and Sjögren's. Second asset velinotamig (BCMA×CD3) creates the dual-target portfolio. Management pedigree: CEO led Keytruda commercialisation; scientific advisor invented the BiTE technology. $340M cash, runway to 2029. Market cap ~$880M. Q2 2026 data readout is the defining catalyst for the entire class.

Candid Therapeutics (Future NASDAQ: CDRX via RallyBio/RLYB merger - Not Yet Listed) — Most aggressive pipeline breadth. Four TCE programs across 10 indications, 87 patients dosed. BCMA lead cizutamig has declared clinical proof-of-concept, advancing into global Phase 2 in myasthenia gravis and ILD in 2026. CEO Ken Song sold RayzeBio to BMS for $4.1B. ~$700M pro forma cash, runway through end of decade.

Tier 2: Large Pharma

Roche/Genentech (SIX: ROG) — Most committed large pharma. Two TCEs in autoimmune trials (mosunetuzumab CD20×CD3 in Phase 1b SLE; RG6382 CD19×CD3 in early development). $10B+ bispecific franchise. Unmatched manufacturing scale.

Amgen (NASDAQ: AMGN) — Furthest-advanced company-sponsored trial (Phase 2a subcutaneous blinatumomab in SLE/RA). The OG BiTE inventor with decades of safety data. The subcutaneous reformulation is the key unlock here — IV blinatumomab's 2-hour half-life requires continuous infusion, a non-starter for outpatient autoimmune care. If the subQ format delivers equivalent B-cell depletion with manageable CRS, Amgen's commercial infrastructure makes them a formidable late-stage competitor.

Merck (NYSE: MRK) — Biggest financial commitment ($700M upfront for CN201 from Curon Biopharmaceutical, $1.3B total). CN201's 7% CRS rate in NHL trials is best-in-class — significantly below the 30–60% range typical of CD3-based TCEs. Autoimmune trials not yet started, making this a medium-term play, but the low-CRS profile could prove decisive in a space where safety is the gating concern.

AstraZeneca (NASDAQ: AZN) — The dark horse. Surovatamig (CD19×CD3, acquired from TeneoTwo) already in Phase 1 for RA and SLE with strong oncology data behind it (77% ORR in DLBCL). Also acquired EsoBiotec's in vivo BCMA CAR-T platform for up to $1B — one of the few pharma players running a genuine dual-modality strategy across both TCEs and engineered cell therapy.

GSK (NYSE: GSK) — Only dual CD19/CD20 trispecific in pharma (CMG1A46 from Chimagen Biosciences, $300M upfront, $850M total). Targeting both antigens simultaneously in a single molecule could deliver the broadest B-cell coverage of any TCE in development. Also backing Ouro Medicines and leveraging deep immunology expertise from the Benlysta franchise.

Tier 3: Differentiated Higher-Risk Watches

IN8bio (NASDAQ: INAB) — First-in-class pan-γδ TCE (INB-619). Genuinely differentiated science addressing the CD3/CRS bottleneck — if γδ biology works as advertised, it leapfrogs the entire CD3 field on both safety and tissue penetration. But: preclinical only, IND not expected until 2027, micro-cap with cash runway only to H1 2027 after a $20.1M tranche (with another $20.1M tied to milestones). The funding gap vs competitors is stark, IN8bio will almost certainly need a pharma partnership or significant financing event to advance INB-619 through clinical development. The near-term proof point: animal model data that validates the in vivo expansion and B-cell depletion thesis. Until that lands, this is pure speculation — but it's the kind of early-stage bet that could deliver outsized returns if the biology translates.

Janux Therapeutics (NASDAQ: JANX) — Purpose-built ARM platform for autoimmune, distinct from their oncology TRACTr technology. JANX011 (CD19×CD3) dosed first patient February 2026 — claims CAR-T-like T-cell expansion/contraction from a subcutaneous injection. ~$940M cash against an ~$855M market cap means the autoimmune program and Merck / BMS partnered oncology pipeline are effectively valued at zero before adjusting for burn. Data expected year-end 2026.

Xencor (NASDAQ: XNCR) — XmAb657 (CD19×CD3) with deep preclinical B-cell depletion data, advancing to first-in-human. Diversified pipeline, Phase 1 interim data expected in H2 2026 . Market cap ~$878M.

UCB (EBR: UCB) — Licensed ATG-201 (masked CD19×CD3) from Antengene for $1.18B. First-in-human Q1 2026. The steric masking approach (CD3 arm only activates upon CD19 binding) is distinct from oncology tumour-activated masking — this is about CRS mitigation, not tissue selectivity.

Tier 4: Adjacent Competitors (CAR-T / Alternative Modalities)

Kyverna Therapeutics (NASDAQ: KYTX) — CD19 CAR-T for autoimmune. BLA filing planned H1 2026 for stiff person syndrome. Most advanced regulatory path but faces CAR-T scalability constraints. ~$520M market cap.

Cabaletta Bio (NASDAQ: CABA) — CD19 CAR-T with registrational cohort in dermatomyositis. ~$320M market cap.

Adicet Bio (NASDAQ: ACET) — Allogeneic Vδ1 γδ CAR-T (prula-cel) targeting CD20 across seven autoimmune indications. Early lupus nephritis data: 100% renal response, zero Grade 2+ CRS. Three FDA Fast Track designations. But: cell therapy (not TCE), requires lymphodepletion, micro-cap (~$70M) trading below cash (~$145M) after reverse stock split. Runway to H2 2027.

Sanofi (NASDAQ: SNY) — $4B+ committed to autoimmune bispecifics via a fundamentally different approach: myeloid cell engagers (MCEs). Instead of redirecting T cells to kill B cells, MCEs tether B cells to tissue-resident macrophages, which physically consume and digest them through a process called phagocytosis — no T-cell activation, meaning potentially zero CRS and zero ICANS. That's the theory; Phase 1 data will test whether macrophage-mediated killing achieves depletion deep enough for immune reset. If it does, Sanofi leapfrogs the entire TCE field on safety.

Tier 5: Private / Pre-IPO (Not Yet Tradeable)

Ouro Medicines (Private) — BCMA×CD3 (gamgertamig) targeting rare autoimmune cytopenias (AIHA, ITP) with FDA Fast Track + Orphan Drug designations — potentially the fastest regulatory path to a TCE autoimmune approval. $120M Series A backed by GSK, TPG, NEA. CEO sold HI-Bio to Biogen for $1.8B. IPO candidate 2026–2027.

Prolium Bioscience (Private) — CD20×CD3 (PRO-203) targeting systemic sclerosis. $50M Series A. First patients dosed March 2026. Differentiated indication with essentially no good treatments.

Catalyst Calendar: Mark These Dates

If you're going to follow one sector in biotech this year, the TCE autoimmune space has more binary catalysts packed into the next nine months than almost anything else in the market.

Q2 2026 is the single most important window. Cullinan's CLN-978 initial data in SLE and RA — the first company-sponsored CD19 TCE dataset in autoimmune disease. Watch for CRS rates, B-cell depletion depth, and autoantibody trends. A clean safety profile with deep depletion validates the class.

Q3 2026: Cullinan repeat-dosing RA data with paired synovial biopsies — the critical test of tissue-level B-cell depletion, arguably the most important dataset in the field.

Mid-2026: Candid/RallyBio merger close and CDRX public listing. Candid Phase 2 initiations. Roche mosunetuzumab SLE primary data. IN8bio animal data for INB-619.

H2 2026: Amgen blinatumomab Phase 2a data. UCB/Antengene ATG-201 first-in-human data. Ouro Medicines gamgertamig data in AIHA/ITP. Janux JANX011 initial readouts.

Conference venues: EULAR 2026 (June), ACR Convergence 2026 (November), and the dedicated 2nd TCE for Autoimmune Disease Summit (October 28–29, Boston).

The Bottom Line

2026 is the inflection year. The field is transitioning from academic case series to company-sponsored clinical trials, and the data readouts arriving over the next nine months will determine whether TCEs become a transformative autoimmune modality or hit unexpected walls.

For pure-play exposure, Cullinan (CGEM) offers the one of the best risk-reward today. Candid (CDRX) will be the most aggressive play upon listing. Janux (JANX) is the most intriguing value setup — ~$940M cash against an ~$855M market cap, with the autoimmune program and partnered oncology pipeline effectively priced at zero. Among large pharma, Roche is the most committed. And for those with genuine venture-stage risk tolerance, IN8bio (INAB) is the highest-risk, highest-reward long-shot on the board — if γδ T cell biology delivers on its preclinical promise, it solves the exact problems the rest of the field is still engineering around.

The key risk remains binary clinical outcomes. Size positions accordingly. Diversify across targets and stages. And keep your calendar clear for Q2 2026 — because when that Cullinan data drops, you'll want to be paying attention.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial or investment advice. BiostockInfo receives no compensation from any company discussed. Always conduct your own due diligence before making investment decisions.