The $10 Billion Hidden Killer: Why Lp(a) Could Be the Next Great Cardiovascular Drug Franchise

The most dangerous number you've never heard of may be quietly sitting in your blood — and for the first time in history, the pharmaceutical industry is just months away from proving it can do something about it.

Lipoprotein(a), or Lp(a), is a cholesterol-carrying particle that affects roughly 1 in 5 adults worldwide — approximately 1.4 billion people — and dramatically elevates their risk of heart attacks and strokes. Until recently, medicine had no approved drug to lower it. No major clinical trial had proven that doing so saves lives. And fewer than 0.5% of adults had ever been tested for it.

That is about to change — in a big way.

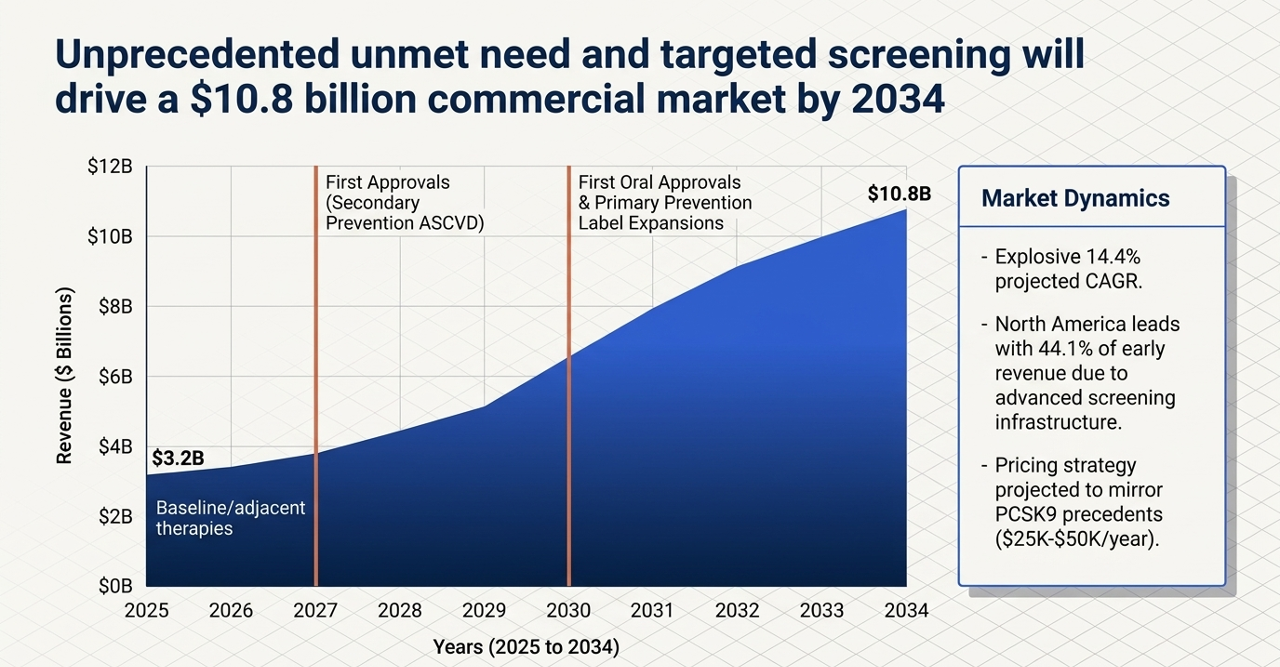

In H1 2026, Novartis will report results from the most anticipated cardiovascular trial in years. Multiple Phase 3 programs are now running simultaneously. New American guidelines now require that every adult be screened at least once. And a competitive race with real commercial stakes — potentially a $4–10 billion+ peak annual sales market — has drawn pharma's biggest names alongside a handful of smaller, high-risk/high-reward biotech players.

This is your complete guide to the Lp(a) landscape: the science, the commercial opportunity, the players, and the catalysts that could reshape cardiovascular medicine.

What Exactly Is Lp(a), and Why Should You Care?

To understand Lp(a), you first need to understand LDL — the "bad cholesterol" that decades of cardiology have targeted with statins. LDL particles carry cholesterol through the bloodstream. When there are too many of them, they can embed in artery walls, triggering inflammation and buildup (plaque) that eventually causes heart attacks and strokes.

Lp(a) is like LDL, but with an extra protein attached — a sticky, uniquely problematic molecule called apolipoprotein(a), or apo(a). This attachment gives Lp(a) several dangerous properties that LDL alone doesn't have:

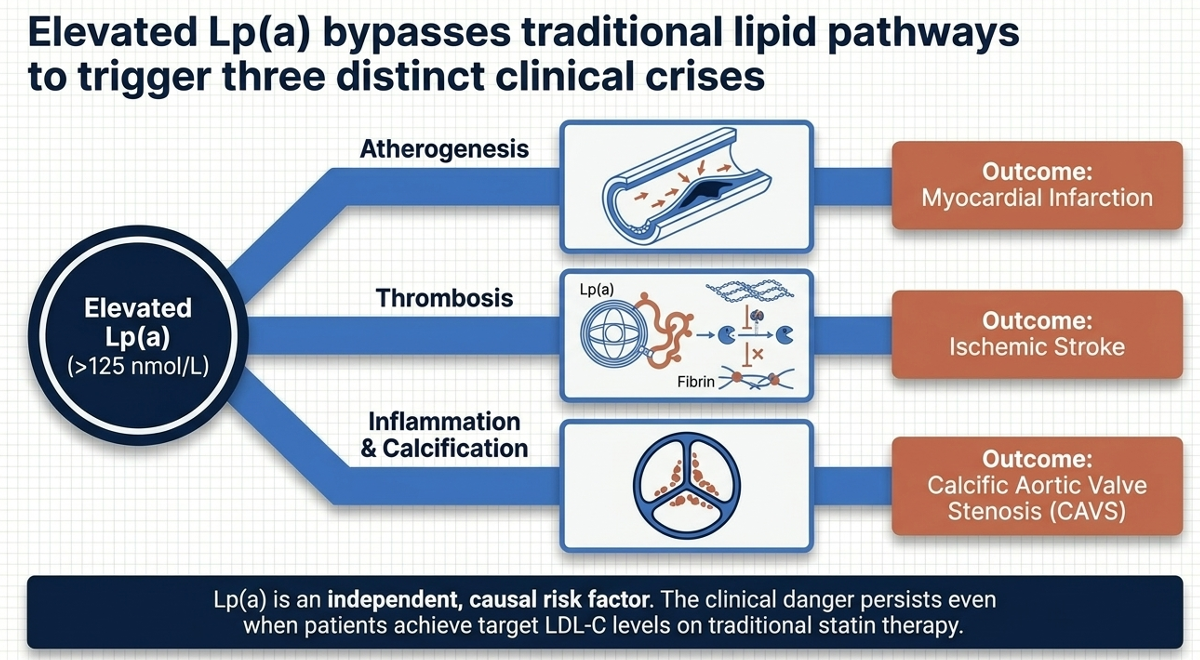

- It carries oxidized phospholipids (OxPL) — inflammatory molecules that accelerate atherosclerosis (artery hardening and plaque buildup)

- It promotes thrombosis — blood clot formation — because apo(a) structurally resembles plasminogen, a key component of the body's clot-dissolving system

- It contributes to aortic valve calcification, which can lead to aortic stenosis — a narrowing of the heart's main valve

The result: people with high Lp(a) face 1.4× to 2× or more elevated cardiovascular risk depending on levels, even when their LDL cholesterol is well-controlled on statins. At extremely high levels (300–400 nmol/L), the risk is comparable to having heterozygous familial hypercholesterolemia — a genetic disorder that has historically warranted aggressive intervention.

Here is the critical and infuriating part: Lp(a) levels are almost entirely determined by genetics. You are born with a level and it barely changes throughout your life. Diet doesn't meaningfully lower it. Exercise doesn't lower it. Statins — the backbone of modern cardiovascular therapy — do not lower Lp(a). In fact, some data suggests statins may modestly increase Lp(a) in some patients. Existing cholesterol drugs simply miss this target entirely.

Until now, there was nothing to do about it. Which is exactly why fewer than 1 in 500 adults has ever been tested.

The Market Opportunity: Why 2026 Is the Inflection Point

The Lp(a) drug story has been building for years but is now hitting a series of converging catalysts that make this the most commercially significant juncture in the field's history.

Catalyst #1: The AHA Just Changed Everything

On March 13, 2026, the American College of Cardiology and American Heart Association released updated dyslipidemia management guidelines that included a landmark ruling: a Class I recommendation — the strongest possible — for universal Lp(a) screening at least once in all adults.

Class I means "is recommended." Not "should be considered." Not "may be useful." Is recommended. This replaces a decade of vague guidance that left Lp(a) testing as an afterthought and created the widespread physician mindset of "why measure what I can't treat?"

The guidelines establish clear risk thresholds:

- ≥125 nmol/L (~50 mg/dL): Risk-enhancing factor, ~1.4× ASCVD risk increase

- ≥250 nmol/L (~100 mg/dL): Greater than 2× higher ASCVD risk

- 300–400 nmol/L: Risk equivalent to familial hypercholesterolemia

Family cascade screening is now also recommended when elevated Lp(a) is found — meaning one positive test can trigger testing across an entire family.

The current testing reality makes the scale of this opportunity starkly clear. An analysis of 300 million patient records from Epic Cosmos found that only 728,550 distinct U.S. patients were tested for Lp(a) between 2015 and 2024 — roughly 0.2% of the population. Globally, the numbers are even worse. A survey of physicians found that only 31% test for Lp(a) regularly. The dominant barrier? "Why measure what I can't treat."

Once a drug is approved, that barrier collapses. The infrastructure being built right now — screening programs, physician education, insurance reimbursement pathways — is the commercial runway that awaits a positive HORIZON trial result.

The addressable patient population is enormous. Roughly 20% of adults have Lp(a) above 50 mg/dL (125 nmol/L). In the United States alone, that is approximately 65 million people. Many of these patients already have established cardiovascular disease and are on maximally tolerated LDL-lowering therapy — yet remain at residual risk that statins cannot address. This is a drug company's dream profile: patients with unmet need, identifiable by a simple blood test, with a compelling rationale for treatment.

The Science Gap: Mechanism Is More Complex Than Assumed

Before diving into specific players, it's worth flagging a mechanistic debate that has important implications for how we think about this class.

The long-assumed logic was: high Lp(a) → high OxPL-apoB → systemic inflammation (elevated hs-CRP and IL-6) → cardiovascular events. Lower Lp(a), lower inflammation, lower events. Simple.

Except it isn't that simple.

In May 2025, data published in JAMA Cardiology from the OCEAN(a)-DOSE trial showed that olpasiran — which achieved greater than 95% Lp(a) reduction and over 89% reduction in OxPL-apoB — produced no significant reduction in hs-CRP or IL-6 at any dose. None. Muvalaplin's Phase 2 KRAKEN trial showed the same thing.

This is a genuinely important finding. It doesn't mean Lp(a) lowering won't benefit patients — it means the mechanism of benefit is probably not primarily through the systemic inflammatory cascade measured by CRP. The current hypothesis is that Lp(a)'s damage occurs through local, vascular effects — direct plaque deposition, localized inflammatory signaling within the artery wall, and prothrombotic activity — rather than the systemic markers we routinely measure in blood.

In practical terms, this means standard inflammatory biomarkers cannot be used as surrogate proof-of-concept for cardiovascular benefit in Lp(a) trials. The field needs actual outcomes data — which is exactly what HORIZON is designed to provide.

The Competitive Landscape: Four Mechanisms, Five Serious Programs

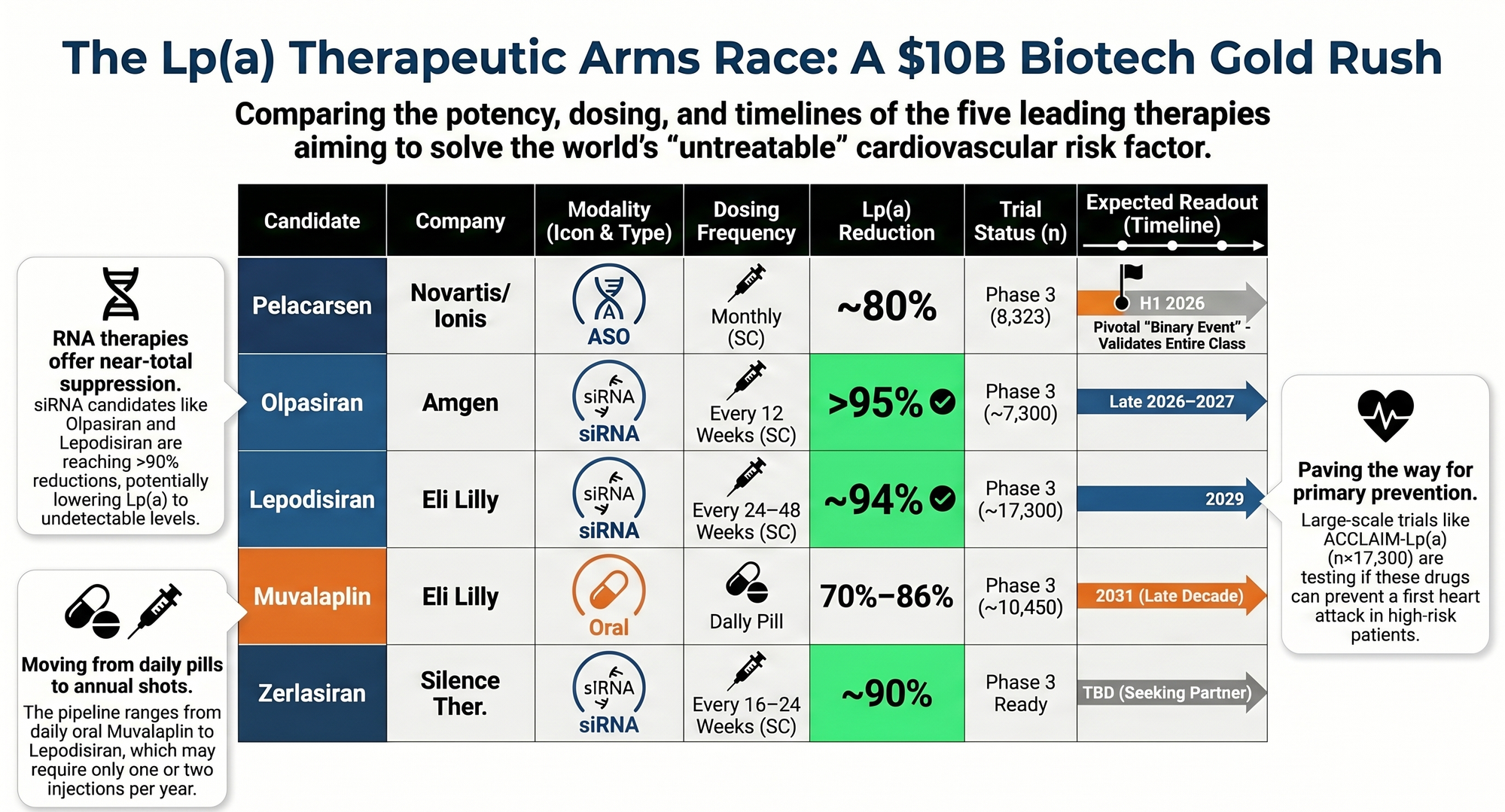

1. Pelacarsen (Novartis / Ionis Pharmaceuticals) — The Catalyst That Changes Everything

Mechanism: Antisense oligonucleotide (ASO). A synthetic piece of genetic code that binds to the liver cells' messenger RNA for apo(a), telling the cell to stop producing the protein. Less apo(a) produced → less Lp(a) assembled and released into the bloodstream. Given as a monthly subcutaneous injection.

Where things stand: The Phase 3 Lp(a)HORIZON trial (NCT04023552) has enrolled 8,323 patients across 797 sites in 42 countries — one of the largest and most rigorous cardiovascular outcomes trials ever run. The primary endpoint is a 4-component MACE: cardiovascular death, non-fatal MI, non-fatal stroke, and urgent coronary revascularization.

The trial was originally expected to read out in H1 2025 but was delayed roughly one year due to slower cardiovascular event accrual than assumed. This sounds alarming — but the reason is actually positive signal about background care quality: 77.5% of enrolled patients were on high-intensity statins, with many also on ezetimibe and PCSK9 inhibitors. The assumed placebo event rate of 4.6% annually was too high for a population this well-controlled. The drug is not failing — the control arm is performing better than expected.

Results are now expected H1 2026, with NDA submission planned for H2 2026 if positive. William Blair analysts have called this "the biggest biotech event of the entire year."

Phase 2b data (NEJM, 2020) showed dose-dependent Lp(a) reductions of up to 80% with a clean safety profile — no thrombocytopenia signal (a feared ASO class effect), no liver toxicity, and no adverse platelet effects confirmed in dedicated sub-studies.

Commercial structure: Novartis owns commercialization rights. Ionis receives tiered royalties in the mid-teens to low-20% range on net sales, of which it retains 75% after selling a 25% slice to Royalty Pharma for up to $1.125 billion. Ionis is also eligible for up to $650 million in development and commercial milestones from Novartis. At analyst consensus peak sales of $4–8 billion, Ionis's retained royalty stream would generate approximately $525M–$1.05 billion annually. Ionis (ticker: IONS) trades around $75–77, well below its recent 52-week high of $86.74, with consensus analyst target of ~$98 and recent upgrades from BofA ($111) and Barclays ($106).

Verdict: HORIZON is the binary that either validates the entire class thesis or sends it back to the drawing board. A positive readout would be transformative for Novartis, Ionis, and arguably every other Lp(a) program listed below.

2. Olpasiran (Amgen) — The Best-Funded Secondary Prevention Program

Mechanism: siRNA (small interfering RNA). Where ASOs bind to mRNA, siRNA exploits the cell's natural RNA interference pathway to degrade the apo(a) mRNA — think of it as programming the cell's own demolition crew to target and destroy the instruction manual for making apo(a). Delivered via GalNAc conjugate — a sugar molecule that acts as a liver-targeting GPS — allowing infrequent dosing. Amgen's Phase 2 dose selected: 75 mg every 12 weeks (quarterly injection).

Data: The OCEAN(a)-DOSE trial demonstrated >95% Lp(a) reduction at the selected dose — essentially ablating Lp(a) from the bloodstream. The OxPL-apoB reductions were similarly dramatic at up to −93.7%.

Phase 3: The OCEAN(a)-Outcomes trial (NCT05581303, TIMI 75) has completed enrollment of over 7,200 patients (target ~7,297) with established ASCVD and Lp(a) ≥200 nmol/L. Primary completion is estimated December 2026, with results likely in 2026–2027.

Amgen has also initiated OCEAN(a)-PreEvent (NCT07136012), a primary prevention Phase 3 trial enrolling 11,000 patients aged ≥50 with no prior cardiac events but Lp(a) ≥200 nmol/L — the first dedicated primary prevention outcomes trial in the class. This significantly expands the eventual addressable market, potentially doubling the eligible population.

Commercial position: Amgen's balance sheet and commercial infrastructure give it an enormous advantage in the race to market. With Lilly's programs, olpasiran represents the second-generation challenge to pelacarsen's first-mover potential.

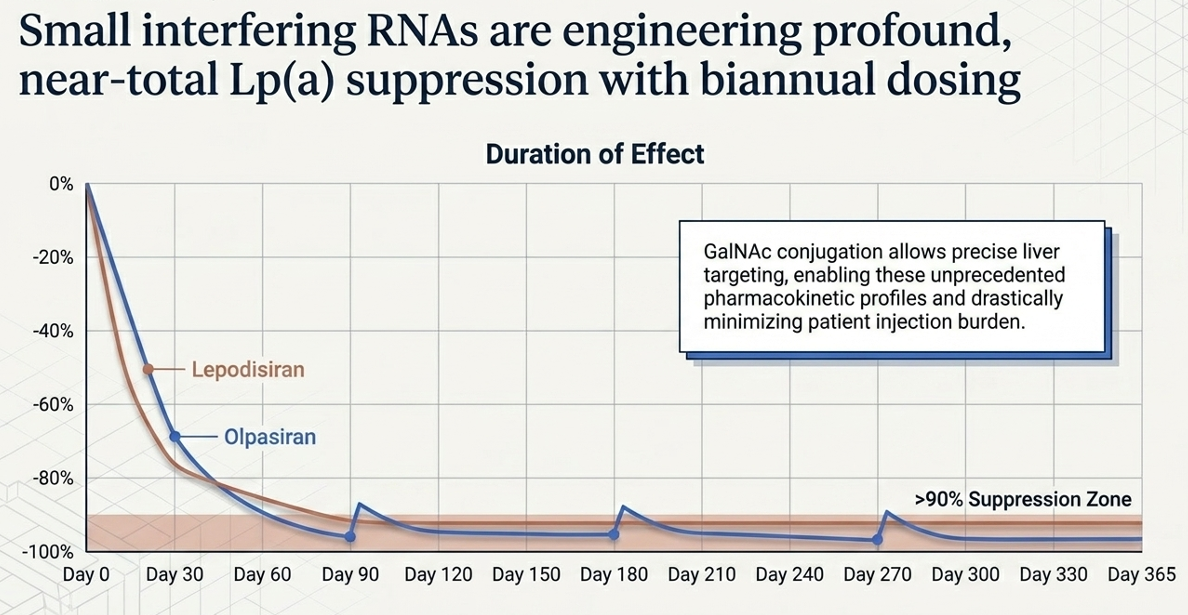

3. Lepodisiran (Eli Lilly) — The Once-Every-Six-Months Disruptor

Mechanism: GalNAc-siRNA with a unique tetraloop Dicer-substrate structure. This engineering innovation gives lepodisiran something no other drug in the class can claim: exceptional pharmacologic durability. Think of it as an siRNA that, once delivered to liver cells, persists and remains active far longer than conventional siRNA molecules.

Data: The Phase 2 ALPACA trial (NEJM, 2025) is striking. At the 400 mg dose tested, placebo-adjusted Lp(a) reduction was −93.9% over days 60–180. After two 400 mg doses (given 6 months apart), Lp(a) remained 94.8% below baseline at 1 year and 74.2% below baseline at 18 months. A single 400 mg dose maintained 53.4% reduction at 18 months.

This data supports a twice-yearly dosing schedule — injected in your doctor's office twice a year, full stop. In a market where adherence is the perennial killer of cardiovascular drug real-world effectiveness, this is a potential differentiation that commands commercial attention.

Safety was acceptable with generally mild and transient liver enzyme elevations (all resolved without intervention, no serious drug-related events).

Phase 3: The ACCLAIM-Lp(a) trial (NCT06292013) is the largest in the class, targeting 12,500–16,700 patients and the first to formally include a primary prevention arm. This is Lilly's statement of intent — they are building the broadest evidence base in the field.

The Lilly thesis: Lilly is simultaneously running two Lp(a) programs with complementary profiles — lepodisiran (injectable, ultra-durable, twice yearly) and muvalaplin (oral, daily pill). This dual-mechanism strategy positions Lilly as the most formidable long-term competitor, with the potential to serve different patient preferences and clinical settings.

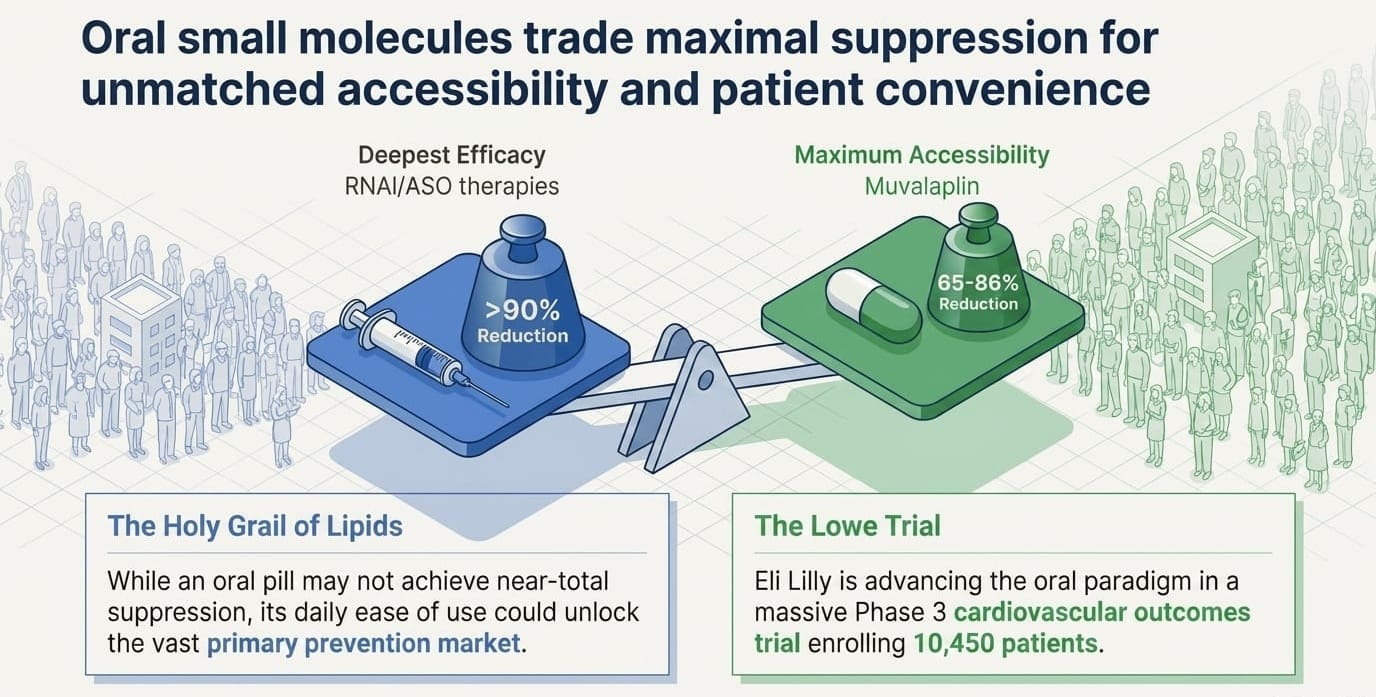

4. Muvalaplin (Eli Lilly) — The Oral Wild Card

Mechanism: First-in-class oral small molecule. This is conceptually different from all the others. Instead of lowering apo(a) gene expression in the liver (like ASOs or siRNAs), muvalaplin works outside cells — it physically blocks the protein-protein interaction between apo(a) and apoB-100, preventing Lp(a) particles from being assembled in the first place. No assembly, no Lp(a). Critically, it does not interfere with plasminogen (the structurally similar clotting protein), which was a key safety concern in early development.

Why oral matters: In cardiovascular medicine, oral drugs have historically outsold injectables — patient preference, prescription behavior, and reimbursement all favor pills. If muvalaplin's efficacy proves sufficient in outcomes trials, the oral route alone could carve out a significant market share.

Data: The Phase 2 KRAKEN trial (JAMA, 2025) in 233 patients tested three daily oral doses. Using the intact Lp(a) assay (the correct measurement for this mechanism), placebo-adjusted reductions at 12 weeks were:

- 10 mg/day: −47.6%

- 60 mg/day: −81.7%

- 240 mg/day: −85.8%

At 60 mg and 240 mg doses, 95.9% and 96.7% of patients achieved Lp(a) below 125 nmol/L — the threshold for elevated risk. ApoB and LDL-C also decreased modestly. Safety was clean with no liver enzyme abnormalities and no plasminogen interference.

Phase 3: The MOVE-Lp(a) outcomes trial (NCT07157774) targets 10,450 patients, with estimated completion in March 2031.

5. Zerlasiran (Silence Therapeutics) — The Science Is Strong, the Strategy Is Not

Mechanism: GalNAc-siRNA targeting LPA gene expression in liver cells. Same broad mechanism class as olpasiran and lepodisiran, but Silence Therapeutics' proprietary AtuRNAi chemistry platform claims advantages in potency and durability.

Data: Genuinely impressive. The Phase 2 ALPACAR-360 trial (JAMA, 2024) in 178 patients demonstrated placebo-adjusted time-averaged Lp(a) reductions of −81% to −86% over 36 weeks at preferred dosing schedules, with median point-in-time reductions of up to −96% at week 36. Earlier Phase 1 APOLLO data showed near-total Lp(a) ablation (−97% to −99% at peak) with reductions of −60% to −90% persisting at 201 days. Safety was favorable.

The science is not the problem.

The headwinds are serious: As of April 2026, Silence Therapeutics is navigating a constellation of challenges that would test any company. CEO Craig Tooman departed in December 2025, with the chair serving as interim executive while the search continues. AstraZeneca returned the rights to SLN312 (Silence's ANGPTL3 siRNA) in March 2026, eliminating a meaningful revenue and partnership validation signal. The Hansoh Pharma collaboration was also terminated. Cash stood at $85.1 million at end of 2025, burning at roughly $20–22 million per quarter — implying a runway to approximately mid-2027 even after stated cost savings.

Most critically: Silence has explicitly stated it will not initiate a Phase 3 cardiovascular outcomes trial for zerlasiran without a partner. No partner has been announced.

With pelacarsen, olpasiran, and lepodisiran all in Phase 3 already, zerlasiran would be fourth to market at best. The company's near-term value driver has effectively shifted to divesiran in polycythemia vera (Phase 2 SANRECO data expected Q3 2026).

The stock trades at $7.60 (market cap ~$358M), with analyst price targets ranging from $4 (Goldman Sachs, Sell) to $75 (H.C. Wainwright, Buy) — the dispersion tells you everything about how differently sophisticated investors are reading the situation.

SLN represents one of two things: either a deeply discounted acquisition target with validated platform technology and clinical-stage Lp(a) asset, or a cautionary tale about running out of runway in a competitive race. That binary is unresolved as of today.

Competitive Landscape Summary

Key Risks to the Thesis

1. HORIZON could miss. This is the single most important risk in the entire space. If pelacarsen fails to reduce cardiovascular events in HORIZON, the entire class thesis faces a crisis — regardless of how well any drug lowers Lp(a) in blood tests. The mechanism of benefit remains unproven at the clinical outcomes level. A negative result would not necessarily kill every program (the argument that different mechanisms or different patient populations might still succeed), but it would be a severe setback.

2. Effect size uncertainty. The trial is powered to detect a hazard ratio of approximately 0.80 — a 20% reduction in events. Given the heavily treated background population (many on statins, ezetimibe, AND PCSK9 inhibitors already), even a statistically positive result might show modest absolute risk reduction, complicating commercial pricing and payer negotiations.

3. The inflammatory biomarker disconnect. As noted above, neither olpasiran nor muvalaplin lowered hs-CRP or IL-6 despite massive Lp(a) reduction. This doesn't disprove the concept, but it does mean we cannot use surrogate biomarker responses as leading indicators — the class is entirely dependent on hard outcome data. There is no interim confidence signal.

4. Competitive crowding. If HORIZON succeeds, Novartis and Ionis have a first-mover advantage — but Amgen's olpasiran won't be far behind, and Lilly's dual portfolio is building the broadest clinical data set in the class. Pricing pressure and market segmentation will follow.

5. Screening infrastructure takes time. The AHA Class I recommendation is a tailwind, but physician behavior change and insurance coverage expansion don't happen overnight. The real commercial ramp may be slower than optimistic models assume.

The Bottom Line: Why 2026 Defines This Market

The Lp(a) landscape is converging on a single point: the HORIZON readout.

If pelacarsen reduces cardiovascular events in 8,323 patients over years of follow-up, it will prove that Lp(a) is a validated, actionable therapeutic target — and unlock a cascade of consequences: FDA approval of the first Lp(a)-specific drug, a wave of physician screening adoption accelerated by the new AHA guidelines, insurance coverage expansion, and commercial validation that signals to the market that every Phase 3 program behind it is worth its investment.

The market being contested is not small. Roughly 1.4 billion people worldwide have elevated Lp(a). With Class I screening now mandated in the U.S., the pipeline of diagnosed, treatment-eligible patients will grow substantially over the coming years. Analyst consensus peak sales estimates for the class range from $4–8 billion — and that may prove conservative if multiple drugs succeed across both secondary and primary prevention indications.

The race is real, the science is sound, the mechanism is finally within reach of proof — and we are weeks to months away from the most consequential readout in cardiovascular medicine in a generation.

This is one of the few spaces in biotech where the question isn't "could this work?" It's "how big does it get when it does?"

Furthermore, it might be worthwhile to check your own Lp(a) level on your next blood test.

The author holds no positions in any securities mentioned in this article. This article is for informational and research purposes only and does not constitute financial advice. Investing in clinical-stage biotechnology companies carries significant risk, including total loss of invested capital. BiostockInfo.com is an independent research publication and is not a registered investment advisor.