Artiva Biotherapeutics (ARTV): Cell Therapy Efficacy. Biologic Safety. And A Commercial Opportunity That's Larger Than The Current Price Implies.

The Setup

Between late March and early May 2026, two private biotechs were acquired by Big Pharma for a combined $3.7B in upfront cash. Gilead paid $1.675B for Ouro Medicines and its BCMAxCD3 T-cell engager. UCB paid $2.0B for Candid Therapeutics and its dual CD19/BCMA TCE pipeline. Both assets were early clinical stage. Both targeted B-cell depletion for autoimmune disease. I flagged both as watchlist names in my March TCE piece. The prices surprised me in their scale and speed.

That backdrop makes Artiva Biotherapeutics (NASDAQ: ARTV) worth a thorough look — because at a current enterprise value of roughly $170M, this company has more disclosed autoimmune clinical data than either acquisition target did at the time of their deals, a safety profile neither can match, a fully-funded Phase 3 with FDA alignment, and early signals across four rheumatological diseases.

This article tries to be honest about what that data actually says — where it is strong, where it is preliminary, and what the range of commercial outcomes looks like depending on how the next 18 months of data evolve. The conclusion is bullish. I want to make sure it earns that.

Disclosure: I hold a long position in ARTV. BSI is a research platform, not an advisory service.

TL;DR — Four Bullets

- The efficacy signal is genuinely unusual. 71% ACR50 at 6 months in the company-sponsored Phase 2a and 83% ACR50/mACR50 in the investigator-initiated trial — in a poly-refractory RA population where every approved therapy achieves ACR50 in 11–19% of patients at the same treatment line. Zero CRS. Zero ICANS. 2% Grade 3+ infections across 55 patients. All outpatient. Zero hospitalisations attributable to AlloNK.

- Approval does not depend on durability — and even the most conservative durability scenario produces a commercially compelling product. Every approved RA therapy requires chronic dosing with zero disease modification. A therapy that produces ACR50 in 50%+ of patients after a single treatment course — regardless of whether re-dosing is eventually needed — is already beyond anything approved. The H1'27 12-month update tells investors which version of a good story this is, not whether the story survives.

- The pipeline is a series of embedded call options currently priced at zero. SjD signals that benchmark numerically above every competing agent in a disease with no approved therapy. SSc data in 4 patients that warrants continued investigation in a competitive vacuum. SLE/LN as the logical next indication. A label expansion roadmap from 3rd-line to 2nd-line to eventually 1st-line high-risk RA that could multiply the addressable market several times over. None of this is in the $170M EV.

- The May 2026 $300M raise — anchored by a $100M concentration bet from RA Capital that takes their total position to ~38% of pro forma outstanding — funds the programme through H2'28 Phase 3 readout. The syndicate composition suggests multi-year value-creation conviction, not a binary trade.

Section 1: What We're Actually Evaluating

Most commentary on ARTV conflates two separate questions: will AlloNK get approved, and how durable is the response? These have different answers and different time horizons. On approval: ARTV's Phase 3 primary endpoint is ACR50 at 6 months versus rituximab-only. If AlloNK delivers ≥50% ACR50 at 6 months with an acceptable safety profile, it gets a BLA. Durability is not an FDA criterion — every approved RA drug was approved on 6-month response data without any requirement for disease modification. On commercial upside: even the most conservative durability scenario produces a product that is better than everything currently approved in the target population. The open question is whether it's very good or transformational.

Section 2: The Mechanism — Why This Version Is Different

The $20B annual US RA market is built on a dirty secret: none of the drugs in it actually modify the disease. They suppress inflammation while you take them. Stop a JAK inhibitor and the disease returns within days. Stop a TNF inhibitor and you're back to baseline within weeks. The reason sits in the biology. Pathogenic B-cells — the immune cells producing autoantibodies attacking joint tissue — don't just circulate in blood. They home to lymph nodes, synovial tissue, the spleen, forming organised inflammatory aggregates. Suppressing this systemically with a JAK inhibitor or TNF blocker is like turning down the volume on a fire alarm without addressing the fire.

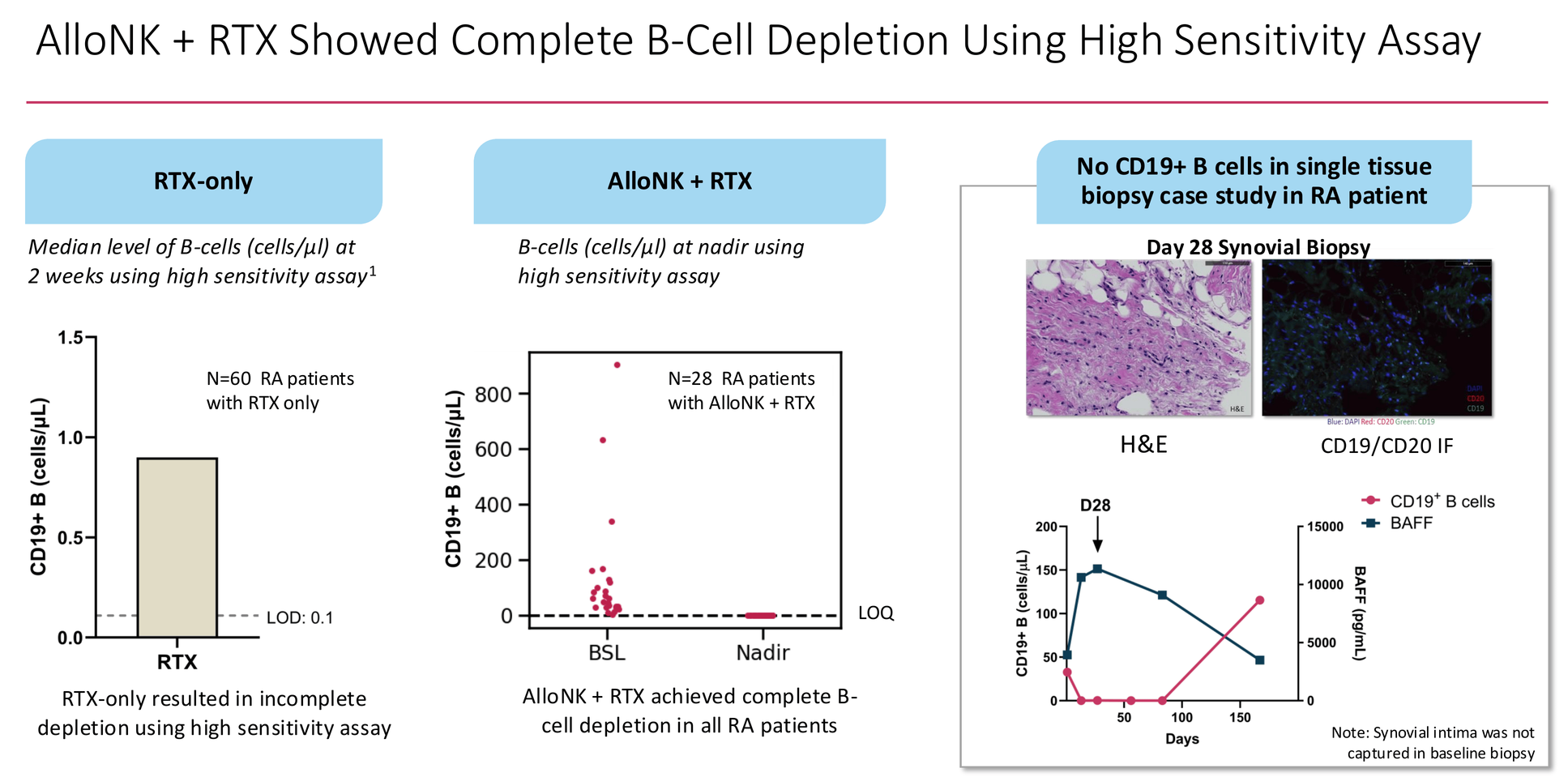

Rituximab is closer to the right idea. It binds CD20 on B-cells and flags them for immune-mediated destruction. In theory, clear the B-cells and the immune system can reconstitute cleanly. In practice, rituximab achieves ACR50 in only 27% of refractory RA patients — because it depletes B-cells efficiently from peripheral blood but consistently leaves residual cells in tissues. A published dataset of 60 RA patients treated with rituximab alone showed median residual B-cell counts of ~0.9 cells/µL at two weeks by high-sensitivity assay. The survivors are enough to repopulate the disease.

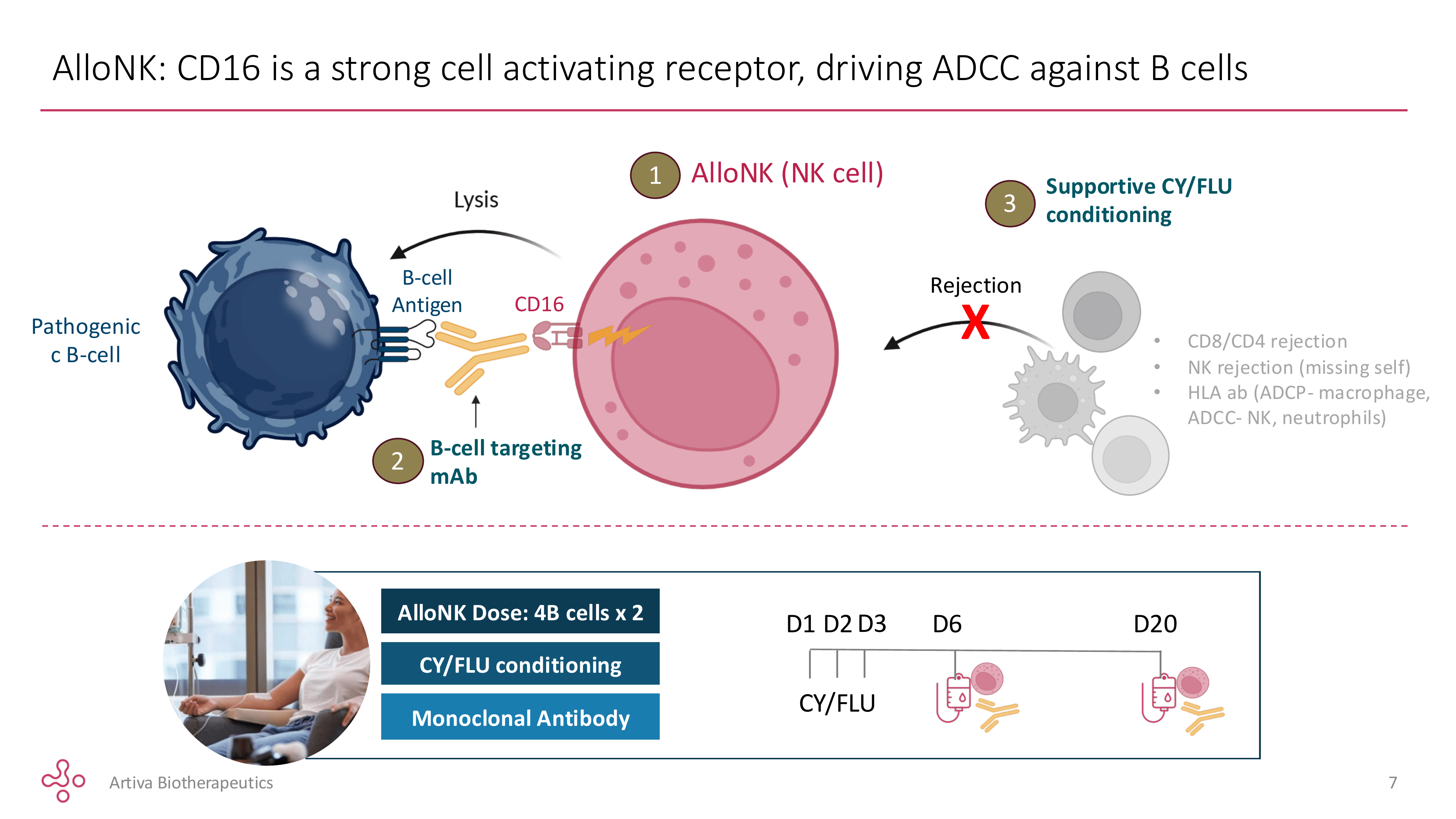

AlloNK is an off-the-shelf frozen preparation of natural killer cells derived from umbilical cord blood, pre-selected from donors carrying two specific genetic features: the high-affinity CD16 158V/V variant — the receptor NK cells use to grab rituximab and direct their killing activity, binding it 5–10× more tightly than the common F/F variant — and the KIR-B haplotype, associated with more aggressive NK cell activation. Only a small fraction of donors carry both. That narrows the manufacturing pool but concentrates the potency.

When infused alongside rituximab, these NK cells use the antibody as a targeting beacon to find and destroy B-cells that rituximab alone cannot clear — including the tissue-resident survivors. Artiva's high-sensitivity assay data shows every one of 28 RA patients driven below the limit of quantitation at nadir, compared to ~0.9 cells/µL residual with rituximab alone. A single Day-28 synovial biopsy in one RA patient showed no detectable CD19+ B-cells in the joint tissue. That is a different category of depletion.

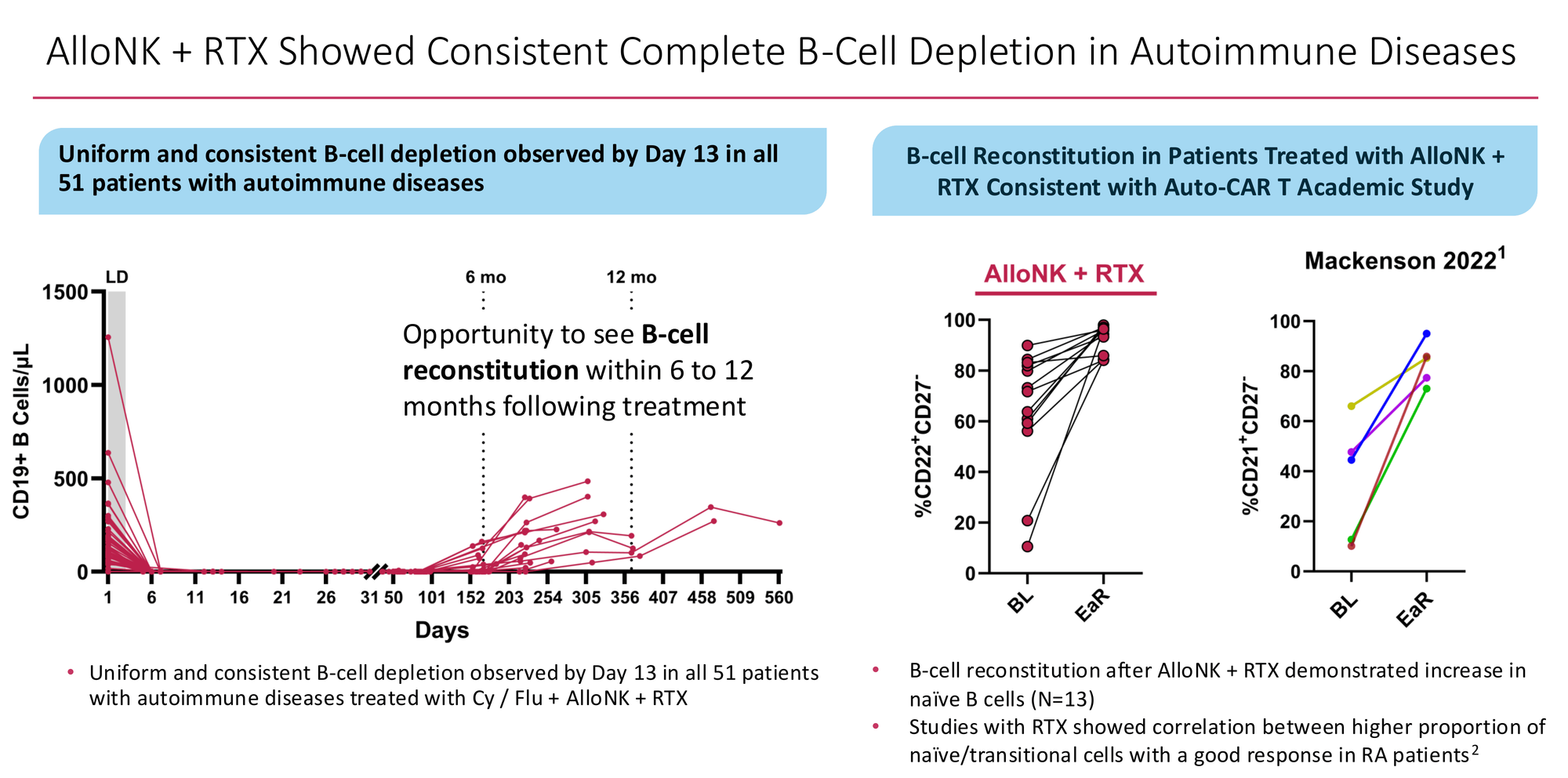

Crucially, the reconstituting B-cell population returns with a naive and transitional phenotype — the immunological clean slate that Mackensen et al. observed in their landmark 2022 CAR-T lupus paper, and that Adlowitz et al. showed correlates with better clinical outcomes in rituximab-treated RA. The immune system isn't just depleted. It restarts.

AlloNK achieves this without activating T-cells. The NK cell mechanism — antibody-dependent cellular cytotoxicity via the CD16 receptor — bypasses CD3 entirely. That single distinction explains the entire safety advantage over T-cell engagers: no T-cell activation means no cytokine release syndrome, no neurotoxicity, and no narrow therapeutic window requiring careful dose titration. The AlloNK NK cells clear circulation within roughly a week of infusion, which is worth understanding — I will address what that means for durability in Section 6.

Section 3: The RA Evidence — Honest Read

The Numbers in Context

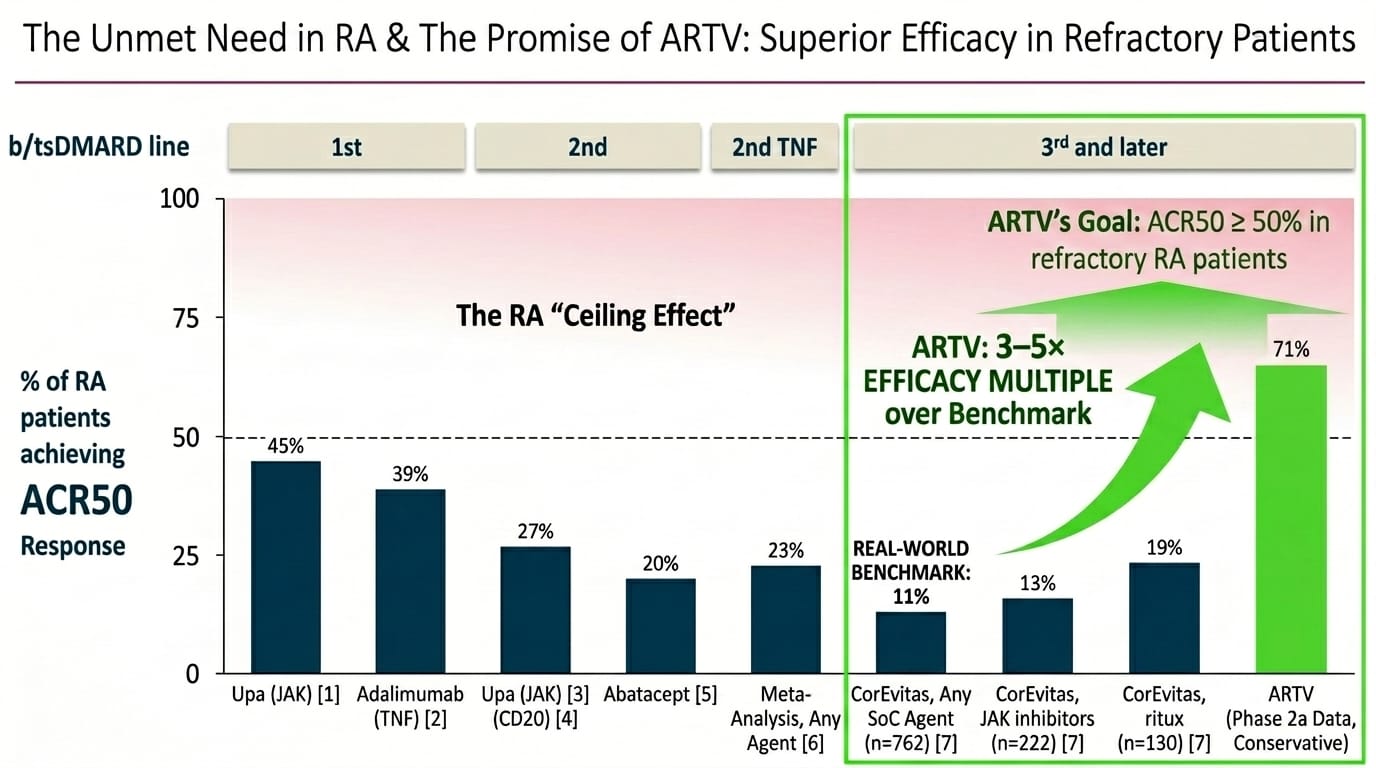

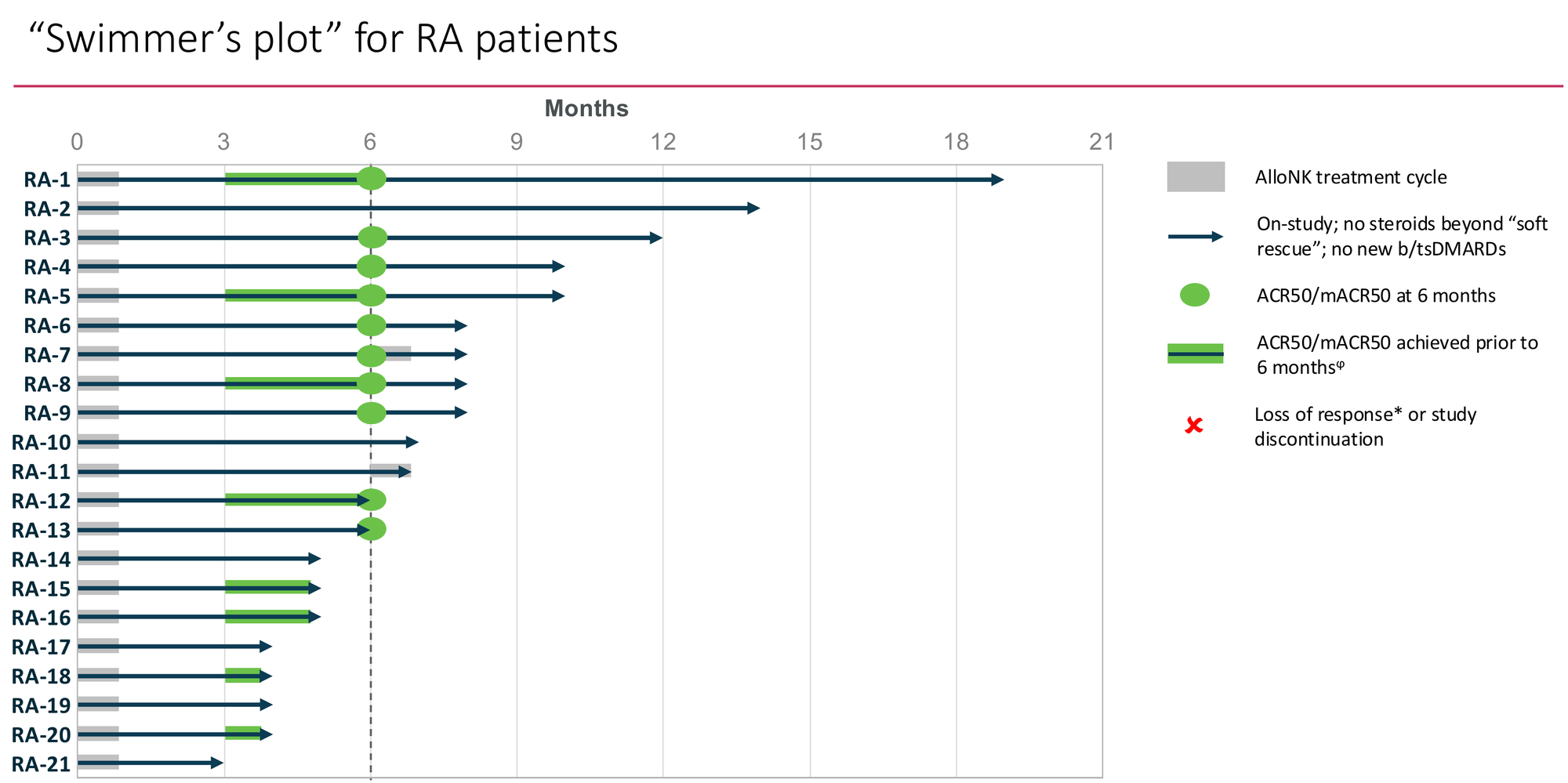

The pooled Phase 2a dataset as of April 3, 2026: 21 RA patients with 12+ weeks of follow-up across two trials. 71% ACR50 at 6 months in the basket study (5 of 7 evaluable patients). 83% ACR50/mACR50 in the IIT (5 of 6), using a modified calculation because HAQ-DI and pain scores weren't collected in that study.

I'll state the sample sizes plainly: 71% is 5 patients and 83% is 5 patients. One additional non-responder in each study moves the headlines to 57% and 67%. These are directional signals, not statistical estimates with meaningful confidence intervals.

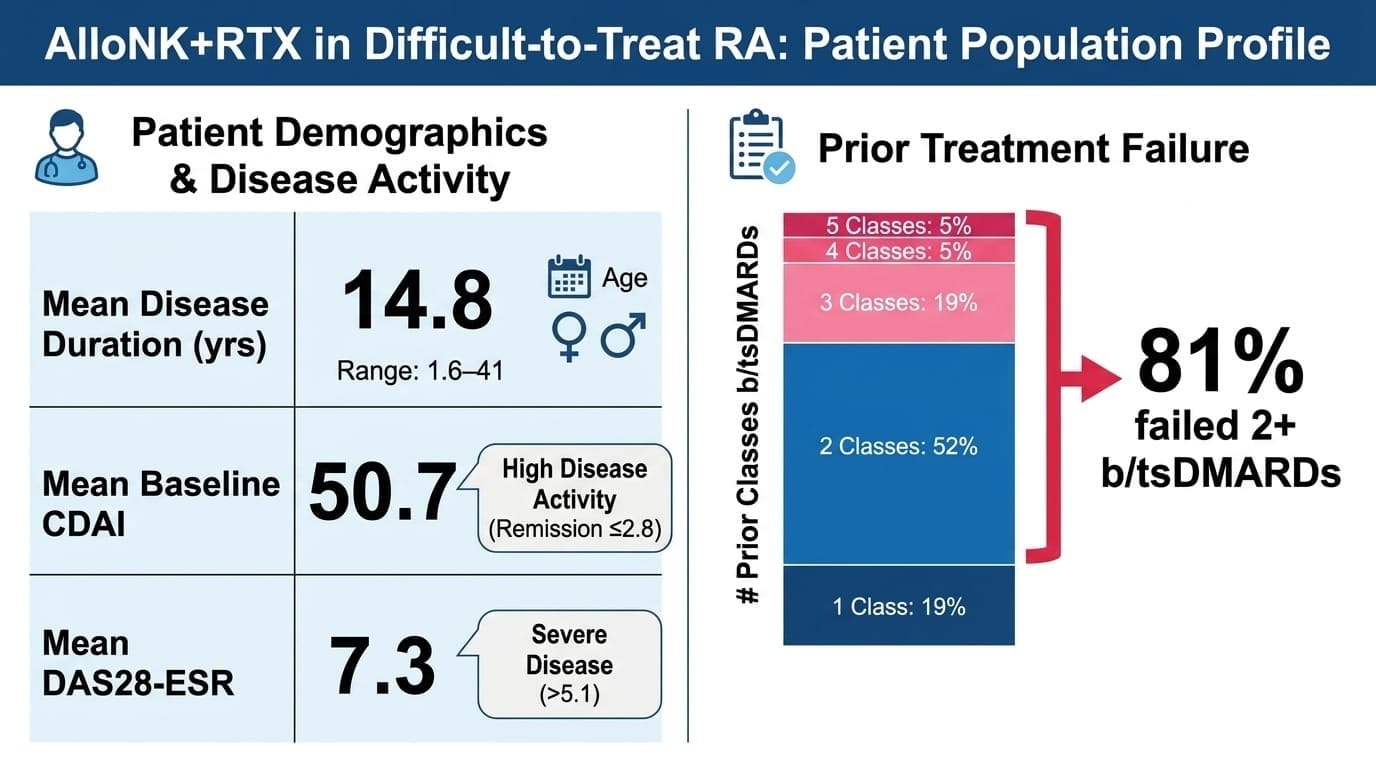

Mean disease duration 14.8 years. 81% failed two or more prior b/tsDMARD classes — five patients had cycled through four or five. Mean baseline CDAI of 50.7 (anything above 22 is high activity; remission is ≤2.8). Mean DAS28-ESR of 7.3. These are patients for whom medicine has largely run out of options.

The CorEvitas real-world registry provides the honest comparison point. In 762 patients on standard-of-care agents at 3rd line and beyond, ACR50 rates are 11% for any agent, 13% for JAK inhibitors, 19% for rituximab. Even with a generous reading of the Phase 2a data — say, 57% rather than 71% if the signal regresses in Phase 3 — we are talking about an efficacy multiple of 3–5× against the real-world benchmark. In the most refractory RA population.

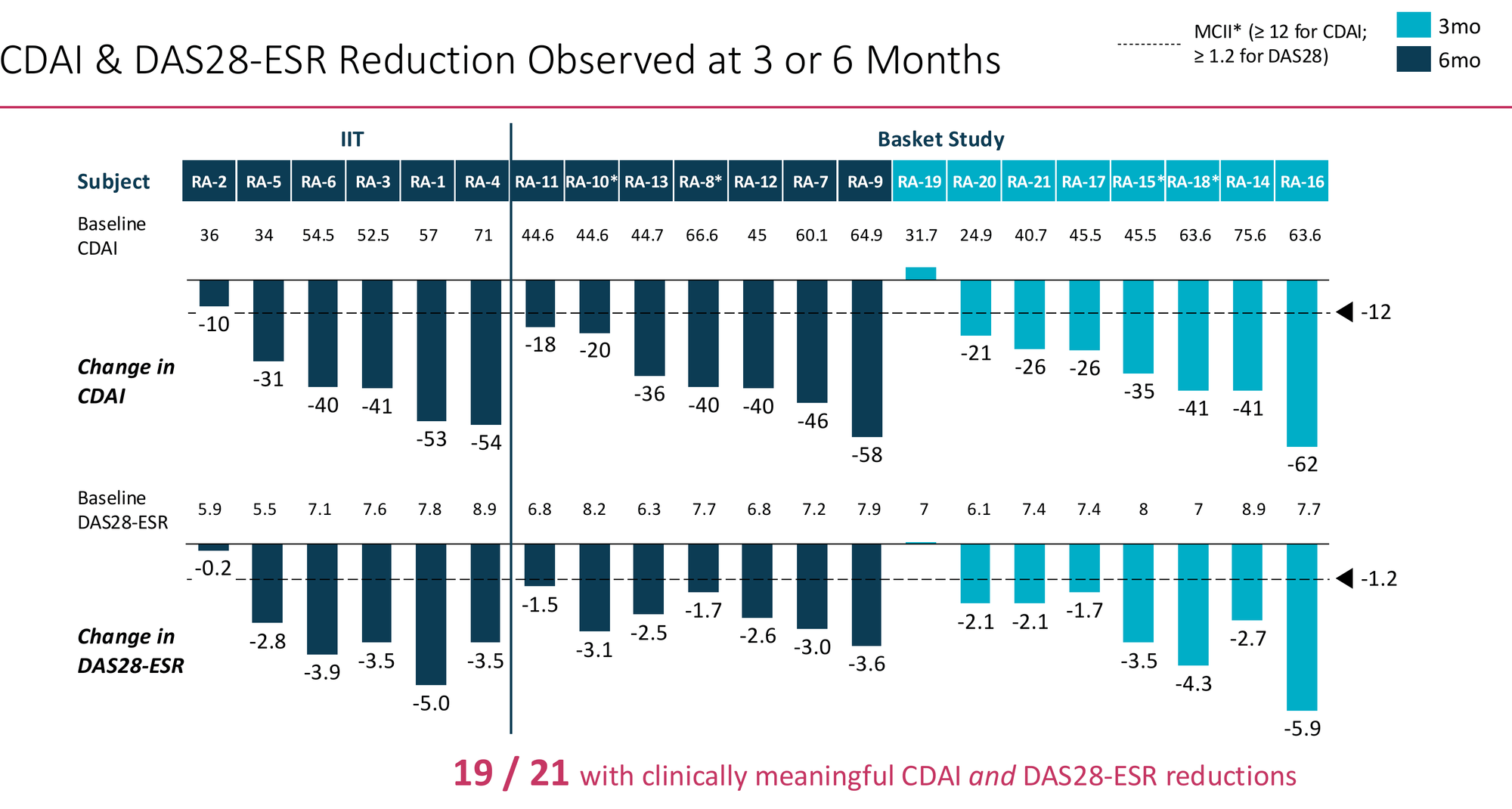

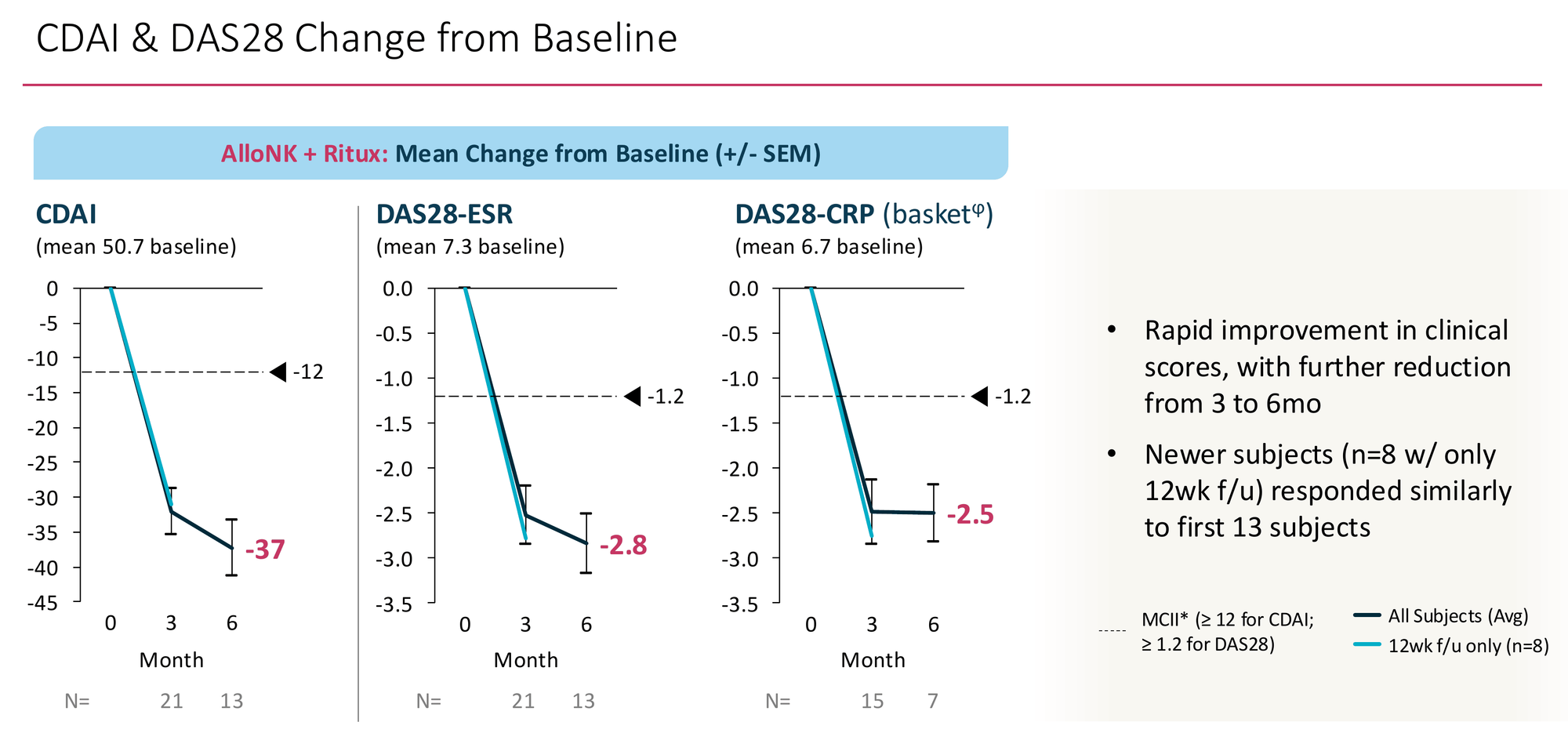

19 of 21 patients showed clinically meaningful reductions in both CDAI and DAS28-ESR. Mean CDAI reduction at 6 months: -37 points from a baseline of 50.7 — a 73% relative reduction. The individual patient waterfall shows broad distribution of response, not one or two outliers pulling the average. Critically, the 8 newer subjects with only 12-week follow-up responded similarly to the original 13 — the signal isn't narrowing as enrolment expands, which is the early failure mode of many Phase 2 programmes.

What Phase 3 Is Testing

150 RA patients, 2:1 randomisation to AlloNK + RTX versus RTX-only, both arms receiving the same Cy/Flu conditioning. Primary endpoint ACR50 at 6 months. Management's assumed split: AlloNK arm 50%+, control arm 20–25%. RTX non-responders at 6 months can cross over to the AlloNK arm — the right ethical design, though it closes the controlled comparison window after the primary readout.

One independent risk worth naming: Cy/Flu conditioning itself has immunomodulatory effects. Transient lymphodepletion can reduce inflammatory tone temporarily. If this elevates the control arm to 30–35%, AlloNK needs ~60%+ to maintain convincing statistical separation. The Phase 2a signal provides cushion, but Phase 2-to-3 regression in autoimmune disease is well documented and should be assumed. Management's ≥50% target is conservative relative to the Phase 2a data — that conservatism is appropriate.

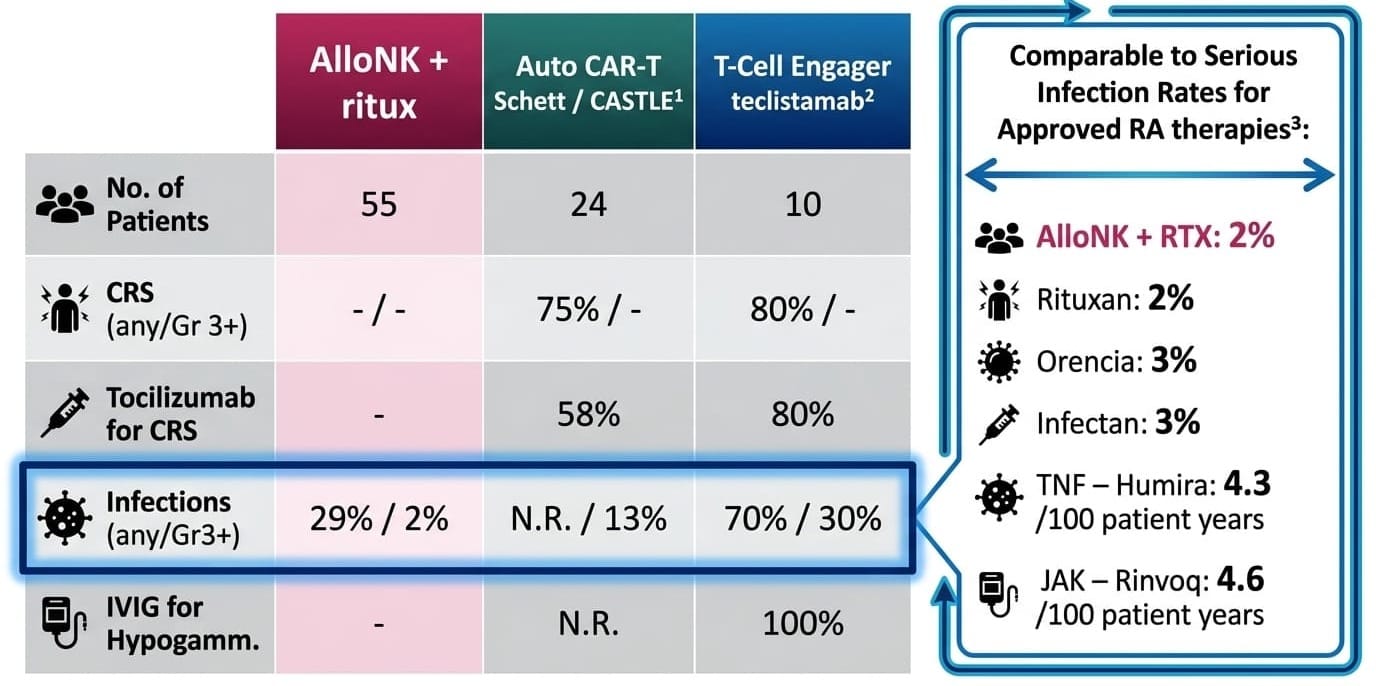

Section 4: The Safety Profile — The Most Defensible Part of The Thesis

Across 55 autoimmune patients treated with Cy/Flu + AlloNK + rituximab as of April 3, 2026:

Zero CRS in 55 patients is not a small-sample result. It is a mechanistic finding. CRS is driven by T-cell activation. AlloNK does not activate T-cells. The CD16/ADCC mechanism bypasses CD3 entirely. This safety advantage cannot erode with scale because it is structural, not statistical.

The full adverse event picture deserves honest presentation: nausea (53%), headache (36%), leukopenia (22%), neutropenia (22%), alopecia (20%), lymphopenia (20%) — all attributable to the Cy/Flu conditioning regimen, not AlloNK. Grade 3+ events were limited to lymphopenia and neutropenia at 5.5% each, self-resolving. No patient discontinued due to any adverse event. No SAEs related to AlloNK. Neutrophil counts drop to Grade 2/3 territory around Day 13 and recover to normal by Day 28 in most RA patients — transient and predictable, not the prolonged cytopenia that drives chronic infection risk in autologous CAR-T.

The real-world validation came at TCT 2026. Veomett et al. published measured costs from 9 patients treated at Integral Rheumatology & Immunology Specialists — a private community rheumatology practice in Plantation, Florida. Total non-drug cost per patient: $18,301. Total adverse event management costs across all 9 patients combined: $409. Zero AlloNK-related hospitalisations. This is not a projection. It is a peer-reviewed cost audit of a community practice running this regimen safely — proof that delivery outside academic medicine is current reality, not future aspiration.

Section 4b: The Commercial Architecture

The physician workflow. A frozen vial of AlloNK arrives at the clinic on dry ice. Stored in a standard commercial freezer. Thawed at bedside on treatment day. Infused in under 10 minutes. Patient walks out the same day. Forty sites are already operating this workflow in the Phase 3 build-out. Compare that to autologous CAR-T: 4-week manufacturing lead time, apheresis, inpatient admission, ICU adjacency, mandatory overnight observation. AlloNK's operational footprint is closer to administering Rituxan than running a CAR-T programme.

The patient experience. Most refractory RA patients have spent years on daily pills or biweekly injections that have stopped working, watching their joints erode while their pharmacy costs compound. Even AlloNK's most conservative commercial outcome — re-dosing every 12–18 months — is a qualitatively different experience from any approved alternative. One treatment course, followed by a year or more of remission off immunomodulatory drugs. That narrative drives formulary pressure and patient advocacy in ways clinical trial data alone does not.

The gross margin structure. Drug COGS below $8K per treatment course. Real-world administration cost $18,301. Total cost of delivery approximately $26K. At a commercial price of $250–400K — reasonable given the $373K CAR-T pricing floor and AlloNK's dramatically simpler administration — gross margins exceed 90%. Higher than any approved biologic. No other cell therapy in development can claim this cost structure.

The payer conversation. Standard of care in refractory RA costs approximately $25K per patient per year with ACR50 rates of 11–19% — roughly $75K over three years for a therapy that is statistically unlikely to work, before accounting for monitoring visits, infusion costs, and downstream joint damage management. AlloNK at $300K one-time or 18-monthly with 50%+ ACR50 delivers comparable cost-per-responder over a 3-year horizon while potentially eliminating the compounding cost of failed therapy cycles. As durability extends toward Tier 2 and 3, the payer math improves further. This is the conversation ARTV's commercial team will be having with formulary committees in 2029.

Section 5: The Durability Question — Properly Understood

Against that backdrop, 0 of 13 evaluable patients relapsing at 6 months after a single AlloNK course is already beyond anything approved in RA. The Swimmer's plot tells an early story that is genuinely encouraging...

The blinatumomab counter-evidence — correctly framed.

The most cited bearish data point is Bucci et al. (Nature Medicine, 2024): 15 RA patients treated with blinatumomab, 9 of 15 relapsing by 3 months and 13 of 15 by 6 months. This is real data. But it is a mechanistic argument about depth of depletion, not a commercial death sentence. Blinatumomab cleared peripheral blood B-cells but left tissue-resident cells intact — exactly the same limitation as rituximab, via a different mechanism. AlloNK + rituximab drives complete depletion below the limit of quantitation in all 28 RA patients tested, including complete synovial clearance in one tissue biopsy case study. The comparison is not TCE versus AlloNK. It is incomplete depletion versus complete depletion. The blinatumomab data is actually Artiva's strongest argument for why depth of depletion matters.

The three commercial tiers.

The durability question determines which version of a good story this is — not whether the story survives.

Tier 1 — Periodic reset (re-dosing every 12–18 months): Still dramatically better efficacy than any approved alternative, outpatient delivery, and — as Section 4b establishes — commercially viable margins even at frequent re-dosing. The conservative scenario. Still a highly attractive product.

Tier 2 — Extended remission (2–3 years): No approved comparator exists. Premium pricing power. The Swimmer's plot trajectory is consistent with this tier. Commercial model shifts from periodic therapy to rare-event treatment.

Tier 3 — Durable drug-free remission (3+ years): What the CAR-T literature and management's commercial objectives both point toward. If this is the reality, AlloNK is the first therapy in RA history to produce genuine disease modification from a single treatment course. Valuation implications are transformational.

The H1'27 durability update — management projects 50+ total patients, 40+ with ACR50 at 6 months, 20+ with 12–18 months of follow-up — will tell us which tier we are in. That is a valuation calibration event, not a binary survival signal. All three tiers produce an approved, commercially meaningful product. The question is how good.

Section 6: The Pipeline — Signals Worth Taking Seriously

Sjögren's Disease: A Neglected Disease With A Compelling Signal

Sjögren's Disease is systematically underrepresented in investment analysis of ARTV — which is strange, because the commercial opportunity may be comparable in size to the RA wedge and the competitive dynamics are more favourable.

SjD affects roughly 4 million Americans. The systemic form — present in approximately 400,000+ patients with meaningful organ involvement — produces debilitating fatigue that patients describe as "living inside sand," joint disease, skin involvement, vasculitis, peripheral neuropathy, and an elevated lymphoma risk. There are no FDA-approved therapies for the underlying systemic disease. Hydroxychloroquine and rituximab are used off-label with modest and inconsistent effect.

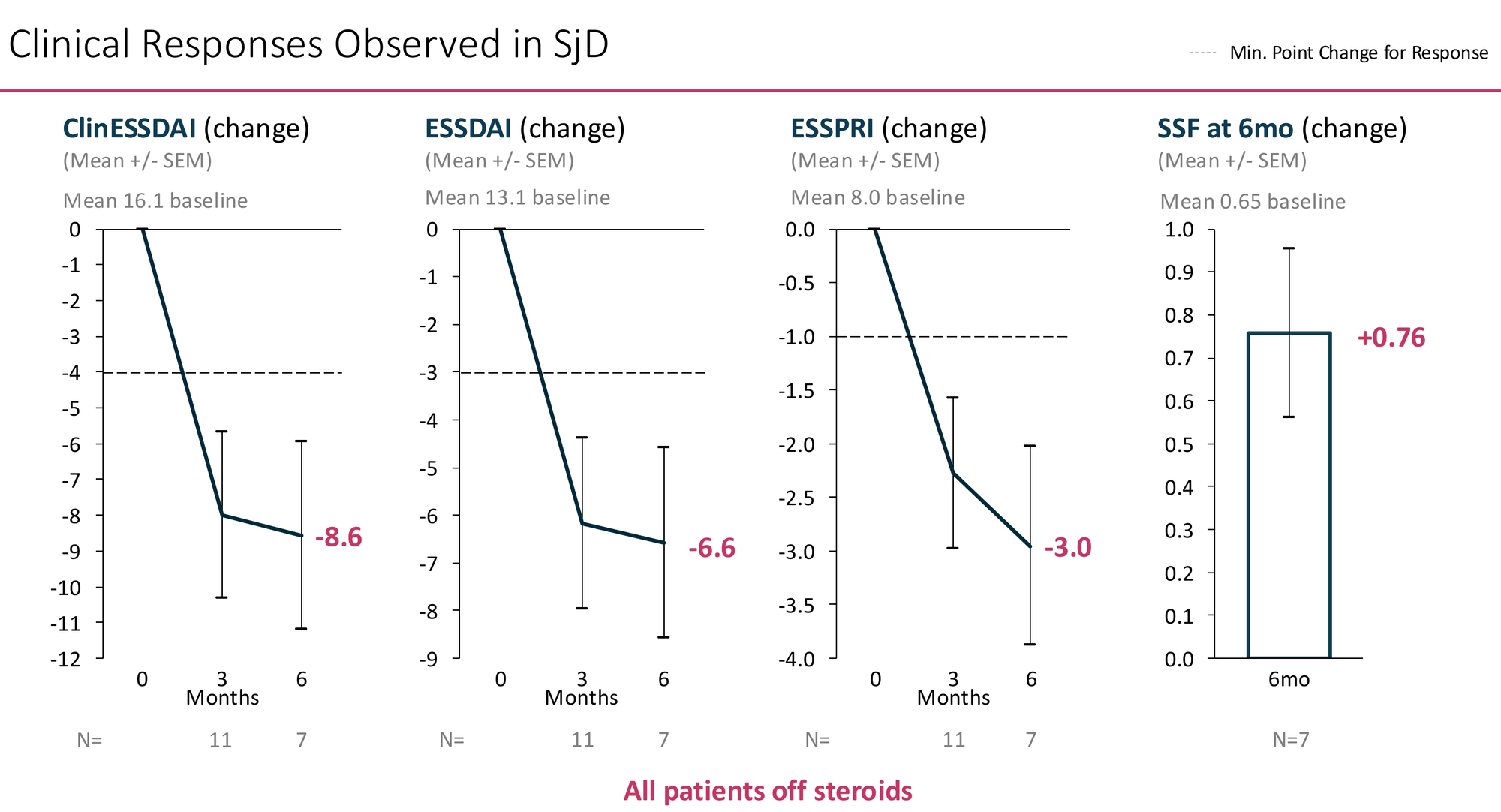

AlloNK's results in 11 SjD patients with 3+ months of follow-up:

All 7 patients with 6-month data were off steroids at that timepoint.

The ClinESSDAI and ESSDAI reductions — composite indices capturing systemic organ involvement across lymphadenopathy, joints, skin, lungs, kidneys, and haematological domains — exceed the response threshold by approximately 2×. The ESSPRI reduction of -3.0 from a baseline of 8.0 represents a substantial improvement in the patient's own daily experience of their disease.

The stimulated salivary flow finding is the most striking individual data point: +0.76 mL/min from a baseline of 0.65 — a near-doubling of salivary output. If real and reproducible, this suggests actual restoration of gland function, not just systemic inflammation suppression. This is what Sjögren's patients most want, and no approved or late-stage therapy has consistently demonstrated it.

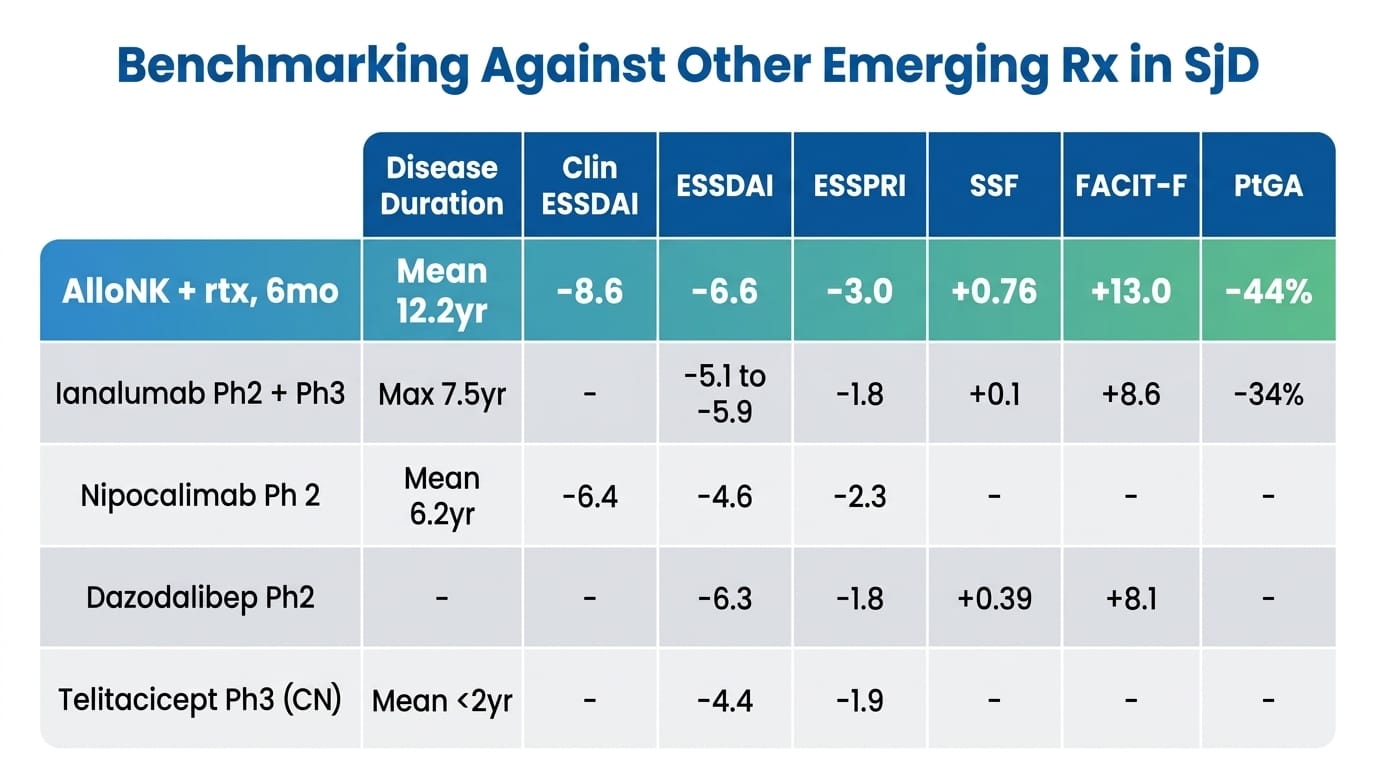

Artiva's deck benchmarks these results against ianalumab (Novartis, Phase 2+3), nipocalimab (J&J, Phase 2), dazodalibep (Amgen, Phase 2), and telitacicept (RemeGen/Vor Bio, Phase 3 China):

No head-to-head trial conducted. Cross-trial comparisons are inherently limited.

AlloNK looks numerically superior across almost every endpoint. But before drawing conclusions from this table, I want to flag the most important confound: disease duration. AlloNK's patients had a mean disease duration of 12.2 years. Ianalumab's patients: maximum 7.5 years. Nipocalimab's: mean 6.2 years. Telitacicept's Phase 3 patients: mean less than 2 years. Established, long-duration Sjögren's is harder to treat — glandular architecture is more destroyed, autoantibody titres are more entrenched, patient-reported scores are systematically lower. This confound systematically disadvantages AlloNK in every cross-trial comparison. The fact that AlloNK still shows the strongest signals across most endpoints — in the most refractory patients — is what makes the table interesting, but it is not a substitute for controlled data.

What the SjD signal does justify: a dedicated Phase 2 programme. The unmet need is severe, the regulatory path has no approved comparator to design around, the B-cell biology is directly applicable, and ianalumab's likely upcoming approval will establish physician familiarity with the indication rather than create a ceiling. A treatment-naive regulatory environment with ~400,000 eligible patients and no incumbent therapy is a commercially rare situation.

Systemic Sclerosis: Extreme Unmet Need, Very Early Data

SSc — scleroderma — is a disease of progressive immune-driven fibrosis of skin and internal organs. Ten-year survival in diffuse SSc is approximately 60%. Two FDA-approved therapies — nintedanib and tocilizumab — address lung function decline in SSc-ILD specifically. Neither modifies the systemic fibrotic disease or skin involvement. For skin-dominant or systemic disease, no approved disease-modifying option exists.

AlloNK in 5 SSc patients (4 with 6-month data): mean disease duration 4.1 years, mean baseline mRSS 19.8, 3 of 5 rituximab-refractory. mRSS change -9.5 points, rCRISS25 100%, rCRISS50 50%. All patients off steroids.

The rCRISS25 threshold Artiva uses (≥0.25 overall improvement probability) sits below the standard clinical trial benchmark of ≥0.60 — so 100% rCRISS25 is a lower bar than it appears. The 50% rCRISS50 is more informative: tocilizumab's Phase 3 achieved 51% standard CRISS in 210 patients versus 37% placebo. AlloNK sitting in that neighbourhood, in rituximab-refractory patients off steroids, is directionally meaningful. The most mechanistically relevant mRSS comparator is inebilizumab — same CD19 depletion target — which produced -5.4 from a single Phase 1 dose. AlloNK's -9.5 from a full regimen in rituximab-refractory patients is coherent against that benchmark.

N=4 is a hypothesis, not a result. The competitive field is also more active than a "vacuum" — AstraZeneca's DAISY Phase 3 (anifrolumab) reads out October 2026, inebilizumab is in Phase 3, and romilkimab met statistical significance in a 97-patient Phase 2. A positive DAISY readout would validate the indication commercially while establishing the endpoint framework AlloNK would use — a tailwind as much as a competitive headwind.

SLE/LN and IIM — The Logical Next Steps

The IIT (NCT06581562) in the TCT poster explicitly includes SLE/LN patients — yet SLE is conspicuously absent from the May 2026 corporate deck's indication breakdown. SLE is arguably the strongest biological case for deep B-cell depletion: it was a CAR-T lupus paper that launched the entire immune reset field in 2022 (Mackensen et al., Nature Medicine), and autologous CAR-T has produced some of the most striking autoimmune remission data ever published in SLE. If AlloNK's depth of depletion is comparable to CAR-T — which the high-sensitivity assay data supports — lupus nephritis may be the highest-value indication expansion available. The "second indication TBD" language in the May 2026 deck may well refer to SLE.

Idiopathic inflammatory myopathies — the fourth basket indication — have no efficacy data yet. The biological rationale is sound. Worth tracking for future readouts.

Section 7: The Expansion Roadmap — Embedded Call Options At Current Price

This is the section of the ARTV thesis that receives the least analytical attention and arguably represents the most significant underpricing at current levels.

The $170M enterprise value is built on one scenario: AlloNK approved in refractory RA patients who have failed 2+ b/tsDMARD classes. That is the appropriate conservative base for an asset that hasn't read out Phase 3. But it means every step beyond that initial approval contributes zero to the current stock price. These are free options that the market is not pricing.

The Label Expansion Ladder

Step 1 (base case): 3rd line+, failed 2+ b/tsDMARDs ~150,000–200,000 US patients. ~$5B annual spend on therapies that statistically won't work. This is the BLA target.

Step 2: Second-line, failed 1 b/tsDMARD A materially larger population — roughly 375,000+ patients cycling through second-line therapy each year. Second-line ACR50 rates for the best available agents are still only 36% (upadacitinib, SELECT-BEYOND). If AlloNK's efficacy holds in a less refractory population — biologically it should, since deeper B-cell depletion becomes more, not less, effective when pathogenic B-cell burden is lower — a second-line expansion study could roughly triple the addressable market. The Phase 3 infrastructure — 80+ sites, 40 already active — makes a parallel or sequential expansion study operationally tractable.

Step 3: First-line in high-risk subpopulations This is a 2032+ story but not a fantasy. Certain RA subpopulations — high-titer seropositive patients, those with early aggressive erosive disease, extra-articular manifestations — have poor long-term outcomes on conventional therapy and strong biological rationale for earlier intervention. The academic literature on early aggressive B-cell depletion in RA is growing. AlloNK's safety profile — 0% CRS, outpatient delivery, biologic-comparable infection rates — is the only cell therapy profile that could plausibly support a first-line argument to rheumatologists and the FDA. This is a long-dated option, but it's real.

The Safety Profile Is The Expansion Enabler

AlloNK's 0% CRS and peer-reviewed community delivery record are what make all three steps plausible — a therapy with 75% CRS rates cannot move earlier in the treatment line.

The Indication Pipeline As Optionality

Assigning rough probability-weighted commercial value to the pipeline optionality that is currently unpriced:

- Second-line RA label: Requires additional trial, probably 2031 approval if pursued immediately post-Phase 3. Incremental TAM roughly 2–3× the initial indication.

- SjD approval: 400,000 eligible US patients, no incumbent approved therapy, strong biological rationale. Comparable commercial size to refractory RA at appropriate pricing for a first-approved agent.

- SSc approval: Smaller population (~100,000), but orphan-adjacent pricing power in a competitive vacuum could generate $800M–$1.5B peak revenue.

- SLE/LN: Potentially the largest single indication. High-value, mechanistically compelling, but data doesn't yet exist.

None of this is in the base case model. All of it becomes meaningfully probable over a 4–6 year horizon if Phase 3 succeeds.

Section 8: The Competitive Landscape — An Honest Assessment

T-Cell Engagers: The Most Relevant Near-Term Competition

TCEs deserve honest treatment because their advantages are real. No Cy/Flu conditioning — patients get an injection and leave, no nausea, no neutrophil nadir, no alopecia. Subcutaneous formulations from Amgen and Cullinan narrow AlloNK's site-of-care advantage meaningfully. And if re-dosing turns out to be required at similar frequency, the overhead of another Cy/Flu cycle is a genuine disadvantage.

The structural ceiling is physics, not an engineering problem. To avoid CRS, TCE developers must detune the CD3 binding affinity — less T-cell activation means less tissue penetration, less clearance of tissue-resident B-cells, and less complete depletion. This is precisely why blinatumomab produced 13 of 15 relapses by 6 months. The field's response — sequential CD19/BCMA strategies, re-dosing protocols — implicitly acknowledges that single-target TCEs cannot reach the reset threshold. AlloNK's ADCC mechanism via CD16 has no such tradeoff: there is no fundamental tension between killing depth and cytokine safety. CRS events have nonetheless been reported in TCE autoimmune programmes even with de-tuned binding — Amgen's subcutaneous blinatumomab Phase 2a and Cullinan's CLN-978 dose-escalation both show CRS requiring management, which requires monitoring infrastructure that doesn't fit most rheumatology practices.

TCEs may win the early commercial race through delivery simplicity. AlloNK's deeper depletion targets the durable remission market TCEs cannot structurally reach. These modalities are more likely to serve different patient segments than compete head-to-head — a multi-winner market, as the RA biologic field before them. Cullinan's EULAR 2026 data and Amgen's subcutaneous blinatumomab Phase 2a readout are the two most important competitive events for ARTV outside its own programme.

Autologous CAR-T: Structurally Constrained

The efficacy data in autoimmune disease is remarkable — Schett/CASTLE showed drug-free remission in SLE and other diseases. The structural barriers are severe and do not improve with scale: 75% CRS rates, inpatient management requirements, 4-week manufacturing turnaround, a site-of-care network that fits oncology centres but not rheumatology. Auto-CAR-T and AlloNK are not competing for the same patients or the same physicians. They are different products for different settings.

In Vivo CAR-T: The Long-Term Wildcard

AbbVie's $2.1B acquisition of Capstan (CPTX2309) brought in vivo CAR-T — mRNA-LNP delivery to generate CD19 CAR-T cells in the patient's own body without manufacturing — into late-stage development. Phase 1 autoimmune data is probably 2028–2029. If this validates, it removes every manufacturing and site-of-care constraint that currently differentiates AlloNK from auto-CAR-T. This is a genuine long-term competitive ceiling and should be acknowledged rather than dismissed. AlloNK's 2030 launch window provides a meaningful market-entry lead, but long-range peak penetration assumptions should reflect the eventual competitive landscape.

Section 9: Management — Honest Assessment

CMO Subhashis Banerjee brings development experience across nine approved drugs: Humira, Orencia, Sotyktu, Taltz, Olumiant, Xeljanz, Uplizna, Naglazyme, and Aldurazyme. That is an exceptional biologics and rare disease track record — and specifically relevant, because his approvals include multiple drugs in exactly the rheumatology and immunology indication space AlloNK is targeting. He understands how the FDA evaluates RA efficacy data, how rheumatologists think about new therapies, and how to design registrational trials that succeed.

What that track record does not include is a novel allogeneic cell therapy IND and BLA. The specific challenges of cord blood donor selection, GMP manufacturing consistency across tens of thousands of vials, and the regulatory novelty of a non-genetically modified NK cell product are different from anything in his previous approvals. The single-trial registrational design — efficient and appropriate given FDA alignment — concentrates risk in a way that leaves no second study to fall back on if the data package has gaps. This is a real execution risk that the team's biologics experience does not fully mitigate.

CEO Fred Aslan has been the right operator at each inflection: the strategic pivot from oncology to autoimmunity in 2023–2024, the July 2024 IPO, and the $300M May 2026 follow-on at 7.9% discount to spot in a difficult market. The financing track record is strong.

The GC Cell dependency is worth flagging explicitly. GC Cell — subsidiary of GC Holdings Korea, one of the world's largest cord blood banks — is both the primary manufacturing partner and an equity participant in the May 2026 offering. The equity alignment is meaningful. But initial cGMP manufacturing in Korea creates supply chain exposure that becomes material as the programme scales toward BLA preparation and commercial launch. A validated US facility is the operational milestone to watch.

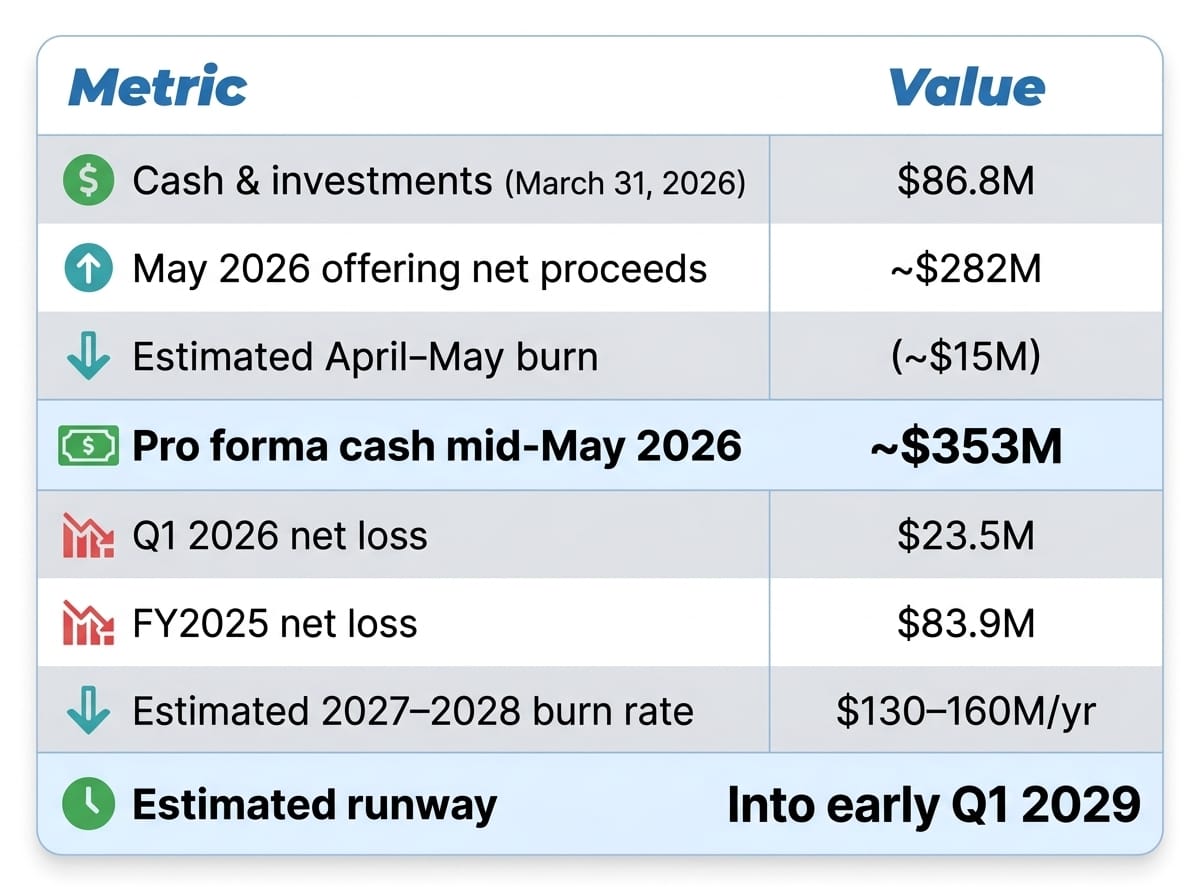

Section 10: The Financial Position

This funds Phase 3 enrolment, the H2'28 readout, and BLA preparation. It does not fund commercial launch. A 2029 capital raise of $200–400M will be necessary. At a successful Phase 3 valuation, that raise is opportunistic and non-threatening. If Phase 3 disappoints, it is existential. That asymmetry is intrinsic to the model.

The RA Capital Signal

The institutional investor list includes Caligan, Venrock, Adage, Samsara, EcoR1, RTW, Viking Global, Blackstone Multi-Asset, Blue Owl Healthcare Opportunities, and GC Cell. The Blackstone and Blue Owl participation is noteworthy — these are value-creation-oriented multi-year holders, not binary-event traders.

But the single most analytically meaningful data point in the financing is a Form 4 filed by RA Capital Management on May 11, 2026. RA Capital purchased 6,510,416 shares and 2,170,138 pre-funded warrants in the offering for a total outlay of approximately $100M. Their total beneficial ownership across all managed accounts: approximately 18.5 million shares and warrants — roughly 38% of pro forma outstanding. At cost, their aggregate ARTV position exceeds $200M.

RA Capital is a dedicated healthcare fund with deep scientific diligence capability and board representation through Laura Stoppel. A $100M concentration bet on top of an already substantial pre-existing position is not a diversification move. It reflects internal scientific conviction about the depth-of-depletion hypothesis, the durability data trajectory, and the pipeline optionality at current prices. When the most analytically rigorous dedicated biotech fund in the space stakes this level of concentration in a single clinical-stage company, that is an independent data point that retail investors — without RA Capital's internal scientific staff — should weight accordingly.

One balancing point: concentration of this magnitude creates overhang risk. If RA Capital needs to reduce their position for any portfolio management reason, there is limited market liquidity to absorb that selling without price impact. Both the signal and the risk are real.

Section 11: Valuation

The Independent Frame

At $10.90, ARTV represents: ~$353M cash plus ~$170M for a Phase 3-ready FDA-aligned autoimmune cell therapy, plus zero for any pipeline indication, zero for any label expansion, and zero for any ex-US partnership. That is the base case you are implicitly accepting at current price.

For context, Kyverna carries ~$280M cash in small neurology indications. Nkarta carries $295M cash with no autoimmune clinical data. Cullinan carries $393M cash with early Phase 1 TCE data. Allogene carries $375M+ cash with preclinical-to-Phase-1 autoimmune programmes. In each case ARTV has substantially more clinical evidence for a comparable or lower enterprise value.

The M&A comp argument — Capstan at $2.1B, Ouro at $1.675B, Candid at $2.0B versus ARTV at $170M EV — is Artiva's framing. I will note its limitation: those acquisitions were for platform technologies (bispecific antibody engineering, in vivo LNP delivery) with inherently broad applicability. AlloNK is mechanism-specific. But the comparison is still directionally valid as evidence that Big Pharma is paying 10× or more of ARTV's current EV for earlier-stage assets in the same therapeutic space.

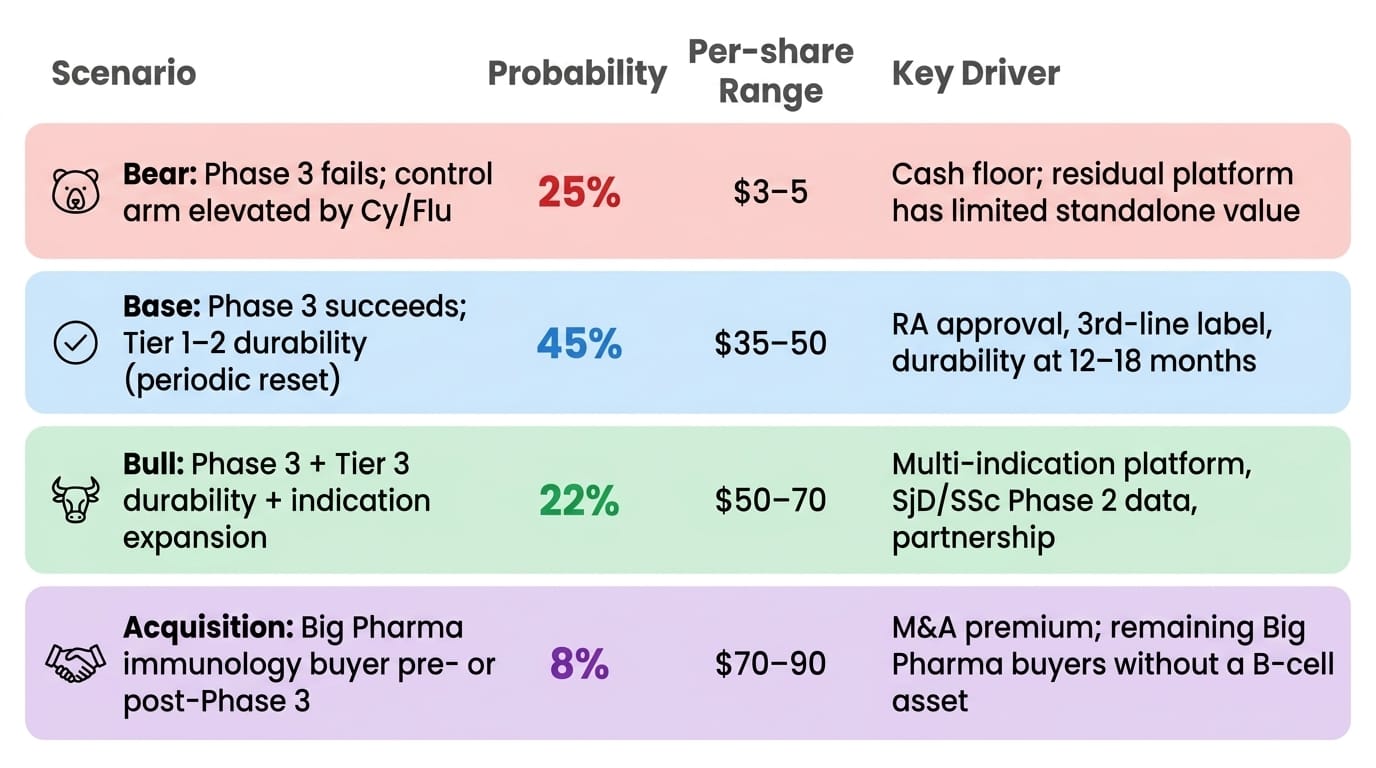

Scenario Framework

Probability-weighted expected value: approximately $33–40 per share — roughly 3–4× current price.

The 25% bear probability reflects the empirical Phase 3 failure rate in autoimmune indications (~30–50%), adjusted modestly downward for FDA single-trial alignment, the conservative ≥50% efficacy target against an observed 71% Phase 2a signal, and a clean 55-patient safety record that reduces the probability of a late-breaking tolerability surprise. The bear floor of $3–5 reflects near-depleted cash at a H2'28 readout after Phase 3 spending, with limited residual platform value.

The base case $35–50 assumes RA approval with Tier 1–2 durability — periodic re-dosing, not one-and-done — which still produces a first-in-class approved cell therapy in a $5B annual market with no comparable approved competitor. Even the conservative commercial scenario is a strong product. The H1'27 durability update is the genuine opportunity to revise probabilities upward before the Phase 3 binary — a clean 12-month dataset would shift meaningful probability mass from base to bull.

What Changes The Math

- H1'27 durability update (clean 20+ patient 12-month dataset): highest-asymmetry near-term event. Probable re-rating toward $30–40 range if maintained ACR50 with no relapses.

- Phase 3 enrolment pace: slow enrolment signals physician hesitancy and compresses rNPV.

- Ex-US partnership: $150–300M upfront plausible; validates platform, extends runway to commercial launch.

- Competitive data: Cullinan CLN-978 EULAR 2026 and Amgen subcutaneous blinatumomab Phase 2a results could re-rate the TCE vs AlloNK relative positioning.

- SjD/SSc Phase 2 initiation decision: signals management's conviction about platform breadth.

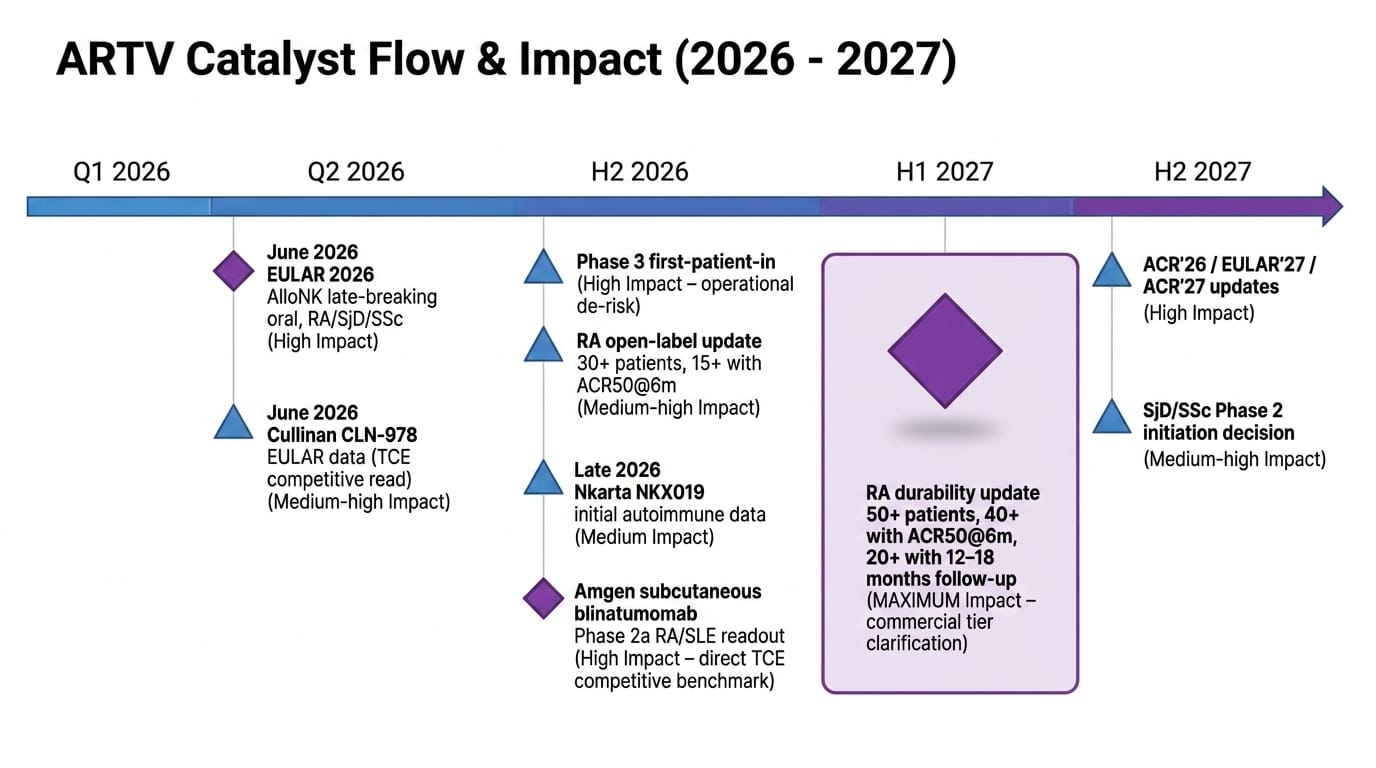

Section 12: Catalyst Calendar

The BSI Take

I spent a long time with this company's data trying to find reasons to be less convinced than the headline numbers suggest. Some of what I found is in this article: The SjD benchmarking table is constructed to persuade, not to prove. The SSc data is four patients. The management team has never navigated a cell therapy BLA. The Cy/Flu conditioning requirement is a real friction cost for community adoption. The TCE field offers genuine convenience advantages that shouldn't be dismissed.

And yet.

The efficacy signal in poly-refractory RA — 71% ACR50 from 7 patients, yes, but in a population where every approved therapy fails 80–90% of patients — is unlike anything in the existing treatment landscape. The safety profile is not statistically clean, it is mechanistically clean: AlloNK cannot cause CRS because it does not activate T-cells. The community practice delivery record from Florida is peer-reviewed reality. The B-cell reconstitution phenotype mirrors the CAR-T literature in a way that supports the durability hypothesis without proving it.

What I find most compelling is not any single data point but the convergence. The mechanism makes biological sense. The depletion depth is demonstrably greater than rituximab. The clinical responses are deep, broadly distributed, and stable at 6 months without re-dosing in a patient population for whom stable at 6 months on any therapy is exceptional. The safety is clean in a way that enables everything else — earlier treatment lines, multiple indications, community delivery — that the current price gives you for free.

The durability question will be answered by H1'27 data. Not resolved — answered well enough to know which commercial tier we're in. Even the most conservative answer — re-dosing every 12–18 months — produces a product that is better than everything currently approved in the target population. The optimistic answer is a product with no comparable precedent in RA history.

At $170M enterprise value, the market is pricing in a very narrow version of this story. The RA approval case alone — assuming Phase 3 executes — looks undervalued by 2–3× at current price. The pipeline optionality, the label expansion roadmap, and the ex-US partnership potential are all unpriced. The RA Capital's additional $100M investment provides independent institutional validation that the scientific analysis supports the thesis.

This is a name for patient capital that understands it is buying a story at a chapter where the ending isn't written yet. The H1'27 durability update will tell us how good the ending is. The current price appears to assume it's mediocre.

I don't think it will be.

Disclaimer

This article reflects independent analysis as of May 12, 2026, based on publicly available company filings, the Artiva May 2026 corporate presentation, the TCT 2026 Veomett et al. pharmacoeconomics poster, SEC Form 4 filings, peer-reviewed literature referenced throughout, and competitor disclosures. BiostockInfo.com is a research and commentary platform, not an investment advisory service. Clinical-stage biotechnology stocks carry substantial risk including total loss of capital. Phase 3 trials fail approximately 30–50% of the time in autoimmune disease. Always conduct your own due diligence and consult a registered investment advisor before making investment decisions.

Related reading: T-Cell Engagers (TCE): The Race to Reset the Immune System — And the Biotechs Positioning to Win (March 11, 2026)