Four Ways to Kill a B-Cell: Why In Vivo CAR-T Just Became Biotech's Hottest Autoimmune Bet

In vivo CAR-T just became biotech's hottest autoimmune bet: $14B committed, zero human readouts. We break down all four B-cell depletion modalities, the leaders, the risks, and what's buyable.

Moderna spent five years teaching the world's immune systems to recognize a spike protein. Its next act: teaching your own T-cells and NK cells to erase your B-cells, from the inside, using the same lipid nanoparticle technology that carried its COVID vaccine. At its Science Day on June 25, 2026, Moderna named mRNA-6007 — nicknamed "007" — as its first in vivo CAR-T candidate, aimed first at lupus. The ambition is explicit: a nanoparticle that reprograms circulating immune cells to hunt down disease-causing B-cells, with no cell harvesting, no chemotherapy conditioning, and — in theory — no reason it couldn't be given at an ordinary infusion clinic. It's still preclinical, with the clinic targeted for 2027.

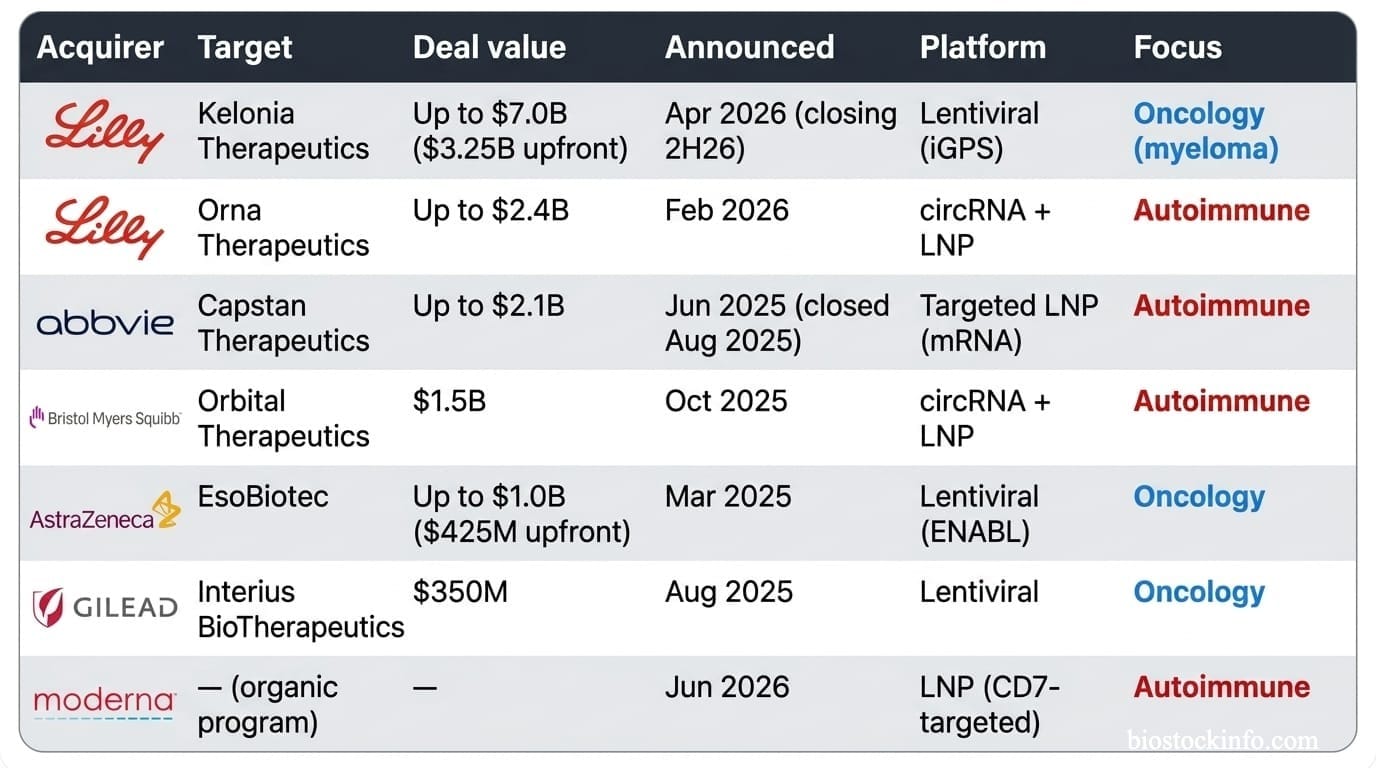

Moderna is not an outlier chasing a fad. It's the sixth major pharmaceutical company to make this exact bet in about fifteen months. AbbVie, Eli Lilly (twice), Bristol Myers Squibb, AstraZeneca, and Gilead have collectively committed more than $14 billion to platforms that do a version of the same thing: generate CAR-T cells inside a patient's body instead of in a lab. That is a staggering amount of capital chasing one delivery idea — a mechanism that, as we'll show, has yet to produce a single human autoimmune efficacy readout, from anyone.

This piece maps the whole terrain: how deep B-cell depletion actually works, the four mechanisms competing to deliver it, which is furthest along, and why in vivo CAR-T is absorbing the most capital despite being the least clinically proven. A quick framing note the title invites — the four ways to kill a pathogenic B-cell are four mechanisms: antibodies, CAR-T, NK cells, and T-cell engagers. "Ex-vivo" and "in vivo" CAR-T aren't two of the four; they're two delivery routes to the same CAR-T mechanism, and they sit at opposite ends of the maturity spectrum. That gap is the story.

The Old Playbook Was Never Built to Cure Anything

To see why an entire industry is racing toward cell therapy, you have to see exactly where antibodies fall short — because the shortfall is mechanical, not a matter of dose.

B-cells mature through stages: naive, then memory, then finally plasma cells — the fully differentiated factories that actually secrete antibodies, including the autoreactive ones that drive disease. The surface marker CD20, targeted by rituximab, sits on naive and memory B-cells but is effectively absent on the long-lived plasma cells that matter most. That's the whole problem in one sentence: rituximab clears the "workers" while leaving the "factories" — tucked into protected bone marrow niches — untouched and still shipping product. Relapse isn't the drug failing; it's the drug doing exactly what it was designed to do against a target that was only ever half the story.

This is why the next generation switched markers. CD19 appears both earlier and later in a B-cell's life than CD20, catching the plasmablasts that CD20 drugs miss — so nearly every platform in this article, from T-cell engagers to CAR-T, targets it. For diseases driven almost entirely by mature plasma cells, developers go one step further to BCMA, found almost exclusively on the antibody-secreting cells themselves. Hold that CD19-versus-BCMA distinction; it returns when we reach Cartesian.

The antibody ceiling is real, but it isn't nothing — and the last year delivered the clearest proof yet. Genentech's obinutuzumab (Gazyva), a Type II anti-CD20 antibody glyco-engineered to kill B-cells harder than rituximab, won full FDA approval for lupus nephritis in October 2025 (Phase 3 REGENCY: 46.4% complete renal response on top of standard therapy), then followed with an accepted SLE filing in April 2026 built on Phase 3 ALLEGORY data — 76.7% of patients hit the SRI-4 responder threshold versus 53.5% on placebo (p<0.001), with an FDA decision due December 2026.

The mechanistic detail is the point. Rituximab — same CD20 target — failed its two big randomized lupus trials years ago (EXPLORER in SLE, LUNAR in lupus nephritis). Obinutuzumab's engineering drives deeper depletion from the identical target, and that alone flipped the outcome. It's a preview of the entire thesis: against B-cell disease, depth of depletion is the variable that separates winners from losers — before you even leave the antibody class.

So sit with the counterintuitive anchor for everything below: the most clinically advanced B-cell therapy in autoimmune disease today is a plain antibody that doesn't achieve deep plasma-cell depletion at all. Regulatory maturity and mechanistic ambition are pointing in opposite directions right now, and that gap is the subject of this piece.

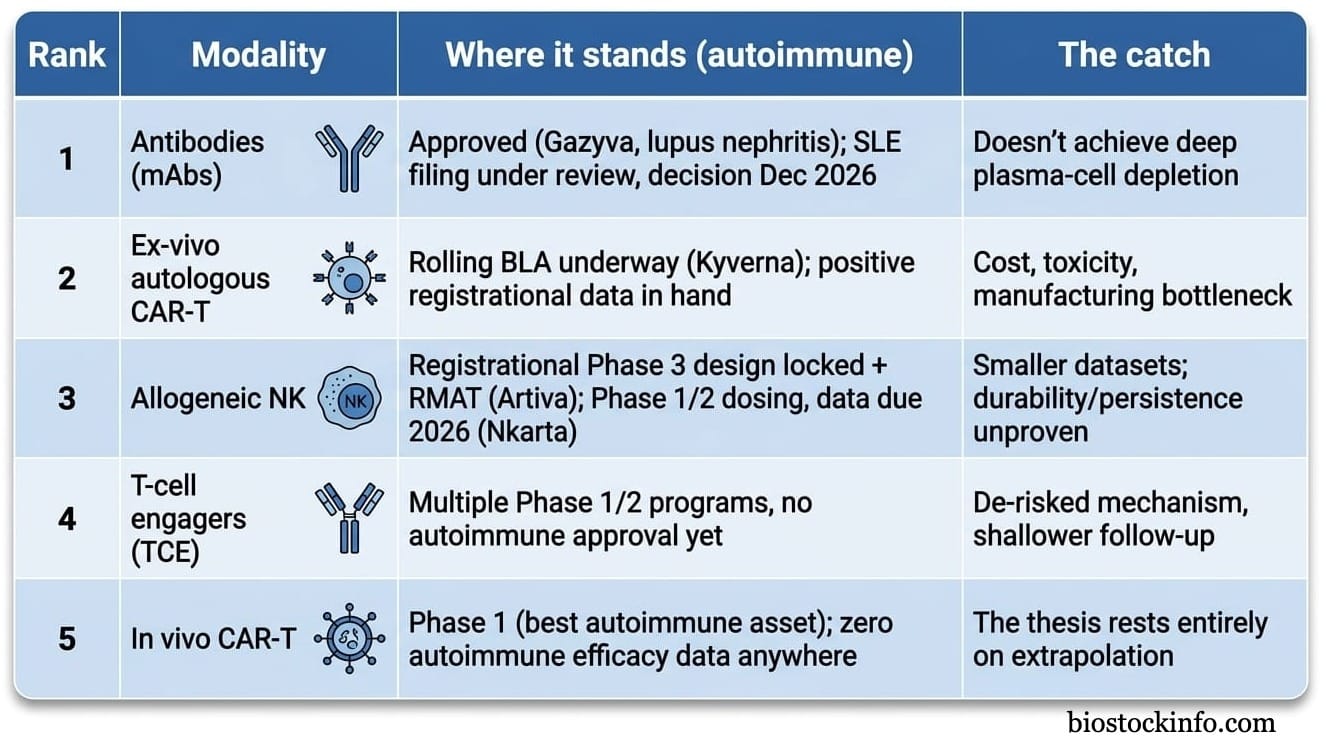

The Maturity Ladder: Who's Actually Furthest Along

Every modality below calls itself "the future." Here's what's been shown in humans — in autoimmune disease specifically, not oncology, which is a further-along and separate conversation — ranked most to least advanced in terms of clinical progress.

Every dollar of the $14 billion wave below is a bet on that fifth row: that in vivo delivery can replicate what ex-vivo CAR-T has already proven — not a confirmation that it has.

First, Respect the Incumbent

One thing the ladder understates: the modality at the top is also the cheapest and most entrenched on it. The anti-CD20 antibody class is the practical benchmark everything else has to clear — rituximab is now generic, outpatient, trusted by every rheumatologist, and workhorse therapy across rheumatoid arthritis, ANCA-associated vasculitis and pemphigus, with its CD20 cousins ocrelizumab and ofatumumab owning multiple sclerosis. Decades of safety data, a fraction of a cell therapy's cost, no specialized center required: that is a formidable moat, and it means a challenger has to win on practicality, not just potency.

So the question every modality below has to answer isn't "can you deplete B-cells?" — rituximab already does, cheaply and at scale. It's "can you deplete them deeply and durably enough to justify more cost, more toxicity, or more novelty than an antibody the whole field already trusts?" That is the bar the rest of this piece is measured against.

Ex-Vivo CAR-T: The Depth Champion With a Scalability Problem

To see what "deep" depletion actually looks like in a patient, look at autologous CD19 CAR-T. A patient's own T-cells are extracted, engineered to carry a CAR, expanded, and reinfused. Unlike an antibody drifting through the blood, these are living cells that traffic into lymph nodes, spleen, and bone marrow, tearing up the germinal centers antibodies can't reach. When the CAR-T cells fade, a fresh, naive, non-autoreactive B-cell population repopulates — the closest thing autoimmune medicine has to a genuine reset button, and the origin of the "drug-free remission" data in refractory lupus that put this whole field on the map.

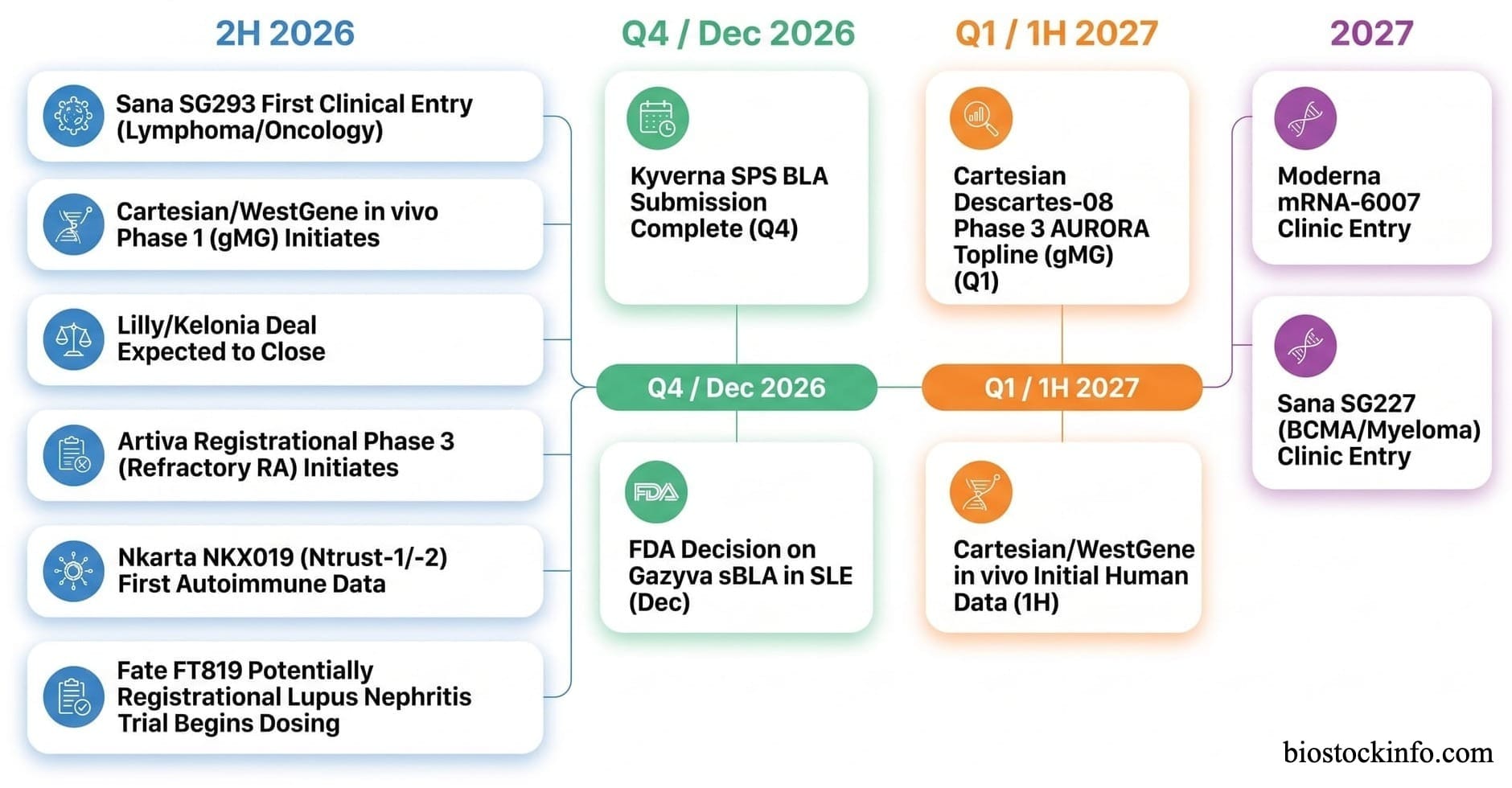

Kyverna Therapeutics (Nasdaq: KYTX) is the name furthest along, and worth using as the worked example. Its CD19 CAR-T, miv-cel (formerly KYV-101), hit statistical significance across all endpoints in a registrational Phase 2 (KYSA-8) in stiff person syndrome — 26 patients, no high-grade CRS or ICANS — and in May 2026 began a rolling BLA targeting completion in Q4 2026, a credible shot at the first FDA-approved CAR-T for any autoimmune disease, with a Phase 3 in myasthenia gravis behind it. Note the paradox: that first approval would land in one of the rarest diseases imaginable. Stiff person syndrome is a beachhead and proof-of-mechanism, not the commercial prize — that sits in the larger follow-on indications, and Kyverna looks equipped to chase them, funded into 2028 (~$236M at Q1), building a commercial team under new Executive Chair Christi Shaw (ex-Kite), with only early-stage competition (Cabaletta, BMS, Novartis) behind it.

The reason this article exists is what even a well-run Kyverna can't fix — a burden that belongs to the modality, not the company. Autologous CAR-T inherits everything oncology CAR-T carries: weeks of centralized manufacturing, toxic lymphodepleting chemotherapy to clear space for the cells, and CRS/ICANS risk that demands inpatient monitoring at specialized centers. A relapsed-leukemia patient facing a terminal prognosis accepts that trade. A 28-year-old with lupus, not facing imminent death, often will not. That mismatch — between the treatment's burden and the population's risk tolerance — is precisely why capital went hunting for alternatives, and why almost none of it went toward more autologous platforms. It went toward removing the apheresis and the chemo altogether.

Two Cheaper Attempts at Depth

Before the modality soaking up the capital, be clear-eyed about the two approaches already trying to solve that access problem — both are live in the clinic, and one has fresh data.

T-cell engagers (TCEs) are the off-the-shelf answer: bispecific antibodies that clamp one arm onto a B-cell target (CD19, CD20, BCMA) and the other onto a patient's own T-cell via CD3, forcing the two together so the T-cell kills — no manufacturing at all. We mapped this whole category — the CD19-versus-BCMA target debate, the CD3/CRS bottleneck, and a tier-by-tier company map — in a dedicated piece. Its bellwether, Cullinan (CGEM), has since delivered the class's first company-sponsored autoimmune readout — at EULAR 2026, deep B-cell depletion in blood and tissue plus remissions in refractory SLE and RA, CRS mostly Grade 1 — broadly de-risking the modality. Two other things have moved. First, the immune-reset land-grab outran the public markets: two names we flagged as pre-listing were bought before they got there — Candid Therapeutics (then set to list via a RallyBio reverse merger) went to UCB for up to $2.2B, and Ouro Medicines (a 2026–27 IPO candidate) went to Gilead and Galapagos for ~$2.2B for its BCMAxCD3 engager gamgertamig. Big Pharma is buying the immune-reset thesis across every modality, not just in vivo CAR-T. Second, IN8bio (Nasdaq: INAB) — which we cover in depth — is advancing INB-619, a CD19 pan-γδ T-cell engager that recruits both tissue-resident Vδ1+ and circulating Vδ2+ γδ cells instead of conventional αβ T cells, matching approved engagers on B-cell killing in vitro while releasing far less of the cytokines that drive CRS. It's still preclinical — IND-enabling now, animal data due 2026, IND expected 2027, the earliest-stage name here — but a December 2025 financing tied a milestone tranche directly to it and pushed runway into 2Q 2027, resolving the cash overhang that long defined the stock; see our INAB update for the full thesis.

Allogeneic NK cell therapy takes a different route: off-the-shelf donor natural killer cells that, because they work outside the T-cell/MHC system, carry essentially none of CAR-T's signature toxicities and can be given on an outpatient basis. The two public leaders illustrate a genuine design split — and it's the fork that corrects a common oversimplification, because "allogeneic NK" is not one thing. Artiva Biotherapeutics (Nasdaq: ARTV) uses unengineered cord-blood NK cells and borrows its targeting from a co-administered antibody (rituximab or obinutuzumab), letting the NK cells kill via ADCC; at EULAR 2026 the combination showed a 71% ACR50 at six months in refractory RA — though that headline is 5 of 7 patients, an encouraging signal on a single-digit denominator, not a registrational result — with deep depletion across RA, Sjögren's and systemic sclerosis and no CRS or ICANS. Nkarta (Nasdaq: NKTX) takes the opposite tack, engineering a CD19 CAR directly into the NK cell plus a membrane-bound IL-15 to boost persistence; its Ntrust-1/-2 trials span lupus nephritis, systemic sclerosis, myositis, vasculitis and RA, and in April 2026 it won FDA agreement for outpatient dosing and re-dosing, with first clinical data due at a 2026 medical meeting. (A third off-the-shelf flavor — iPSC-derived allogeneic CAR-T, led publicly by Fate Therapeutics' FT819, now Phase 1 in SLE and heading into a potentially registrational lupus nephritis trial in 2H 2026 — chases the same accessibility goal from the CAR-T side.) The shared open question is persistence: NK cells don't build the lasting memory compartment CAR-T does, which is precisely why Artiva leans on re-dosing and antibody support while Nkarta engineers in IL-15. Net, this is the strongest evidence in the landscape that "deep" and "accessible" need not be mutually exclusive — see our ARTV due diligence for the full breakdown.

Both are genuinely de-risking alternatives today. Neither is what's pulling in $14 billion. That's the modality we haven't reached yet.

The Main Event: In Vivo CAR-T

The idea in one sentence: instead of removing a patient's T-cells to engineer them in a lab, you inject a vector that finds and reprograms those T-cells while they're still inside the body — no apheresis, no manufacturing wait, and in most designs no lymphodepleting chemo. If it works, a $300,000-plus, multi-week, specialist-center procedure becomes something deliverable like an ordinary biologic infusion.

How it works, in plain terms

Two delivery vehicles exist, and the choice defines almost everything else.

Lipid nanoparticles (LNPs) — the mRNA-vaccine delivery tech — are dressed with a targeting molecule that acts as an address label, steering the particle to a chosen cell type (several programs aim at CD8+ T-cells; Moderna's 007 targets CD7 across T-cells and NK cells). Inside, the LNP releases mRNA that the cell translates into a CAR. Because it's mRNA, the effect is transient — the CAR-T cells the body makes fade within days to weeks as the mRNA degrades. A practical bonus of leaving nothing behind: re-dosing is straightforward — one partner's early clinical experience includes a patient given up to 14 infusions with a single mild CRS event.

Engineered viral vectors (usually lentivirus, re-coated to target T-cells) deliver DNA that permanently integrates into the genome — mimicking the durability of conventional ex-vivo CAR-T, but carrying the classic integrating-vector risks: insertional mutagenesis, and a stronger immune reaction to the viral particle that complicates re-dosing.

Now the split that matters. Read the deal table by disease and the biology explains itself: permanence is an asset in cancer, where you want lasting surveillance, and a liability in autoimmune disease, where the goal is a temporary, catastrophic hit to the pathogenic B-cells followed by a clean reset — no lifelong B-cell aplasia, no permanent infection risk. That single distinction sorts the entire field. The transient LNP/circRNA camp (Capstan, Orna, BMS's Orbital, Moderna) is aimed at autoimmune disease; the integrating lentiviral camp (Kelonia, EsoBiotec, Interius, Umoja) is aimed at oncology.

The In Vivo CAR-T M&A wave

One deal to keep out of the tally: AstraZeneca's earlier Gracell buyout ($1.2B, Feb 2024) was a different animal — an ex-vivo, next-day-manufacturing CAR-T (FasTCAR), not in vivo. Two separate bets, thirteen months apart.

What's actually been shown in humans

This is the most important paragraph in the article. The most informative in vivo data so far comes from oncology, not autoimmune disease. EsoBiotec's ESO-T01 (an in vivo lentiviral BCMA CAR-T, now AstraZeneca's) produced striking results in a five-patient myeloma study in Nature Medicine: four of five heavily pretreated patients responded, three with stringent complete remissions, all without chemo conditioning or apheresis. It also produced a real safety scare — every patient had grade 3-or-higher adverse events, four had CRS, and one died from spinal-cord compression by a pre-existing tumor before the first efficacy check (AstraZeneca attributes the death to aggressive underlying disease; the small cohort and the severity of events drew immediate scrutiny). Kelonia's KLN-1010 — Lilly's $7 billion bet, featured in the 2025 ASH plenary — showed comparably deep myeloma responses without the same safety signal, the data point that appears to justify Lilly's price.

Both are genuine human in vivo CAR-T efficacy signals. Neither is in autoimmune disease. Capstan's CPTX2309 — the most advanced autoimmune asset in existence, a targeted-LNP construct that turns CD8+ T-cells into a CD19 CAR — sits in Phase 1 with no interim data reported. Cartesian Therapeutics has layered an in vivo bet onto its ex-vivo franchise: a June 2026 deal with WestGene Biopharma pairs Cartesian's clinically validated mRNA payload — notably a BCMA-directed one, the plasma-cell angle rather than the crowded CD19 lane — with WestGene's LNP for a Phase 1 in myasthenia gravis in 2H 2026, data in 1H 2027. Moderna's 007 is preclinical.

So the mechanism — systemic delivery, in-body transduction, functional CAR-T without a lab — is proven in humans. The specific promise underwriting $14 billion — that it replicates ex-vivo CD19 CAR-T's autoimmune results — is an extrapolation, not a confirmed result. The biological logic for transfer is sound, given how strong the ex-vivo autoimmune data is. But readers should be clear how much of today's excitement is pattern-matching rather than data, because that is exactly where the next 18 months of surprises — good and bad — will come from.

The Bear Case, Both Sides

On ex-vivo CAR-T: the efficacy is the best in the field, but the cost-and-toxicity structure caps its reach at the sickest, most refractory patients who can tolerate an inpatient procedure. Every dollar spent fixing that — allogeneic cells, non-integrating mRNA, lighter conditioning — is an admission of the limitation.

On in vivo CAR-T:

- Vector immunogenicity isn't solved. The envelope-engineering work across the lentiviral field exists because current vectors provoke an immune response strong enough to threaten safety and re-dosing — a viral-vector problem more than an LNP one, which is part of why autoimmune programs lean LNP.

- There's no quality-control step. Ex-vivo CAR-T is tested before it goes back in. In vivo transduction happens inside the body with no equivalent checkpoint, leaving potency and batch-to-patient consistency genuinely open.

- The ESO-T01 death is a data point, not noise. "No conditioning" is a real win, but it isn't "no systemic risk" — a vector triggering hyperacute inflammation is its own hazard. Every patient in that study had grade 3+ events.

- "Off-the-shelf" doesn't mean cheap. LNP and vector production swaps cell-manufacturing cost for biologics/vector cost — probably a better trade, but not a free one.

- Nearly every credible pure-play is now owned by a company for which it's immaterial. Which leads straight to the next section.

What You Can Actually Buy

This is the most useful thing an investor can take from this piece: the technology narrative and the investable universe have decoupled.

Capstan, Orna, Kelonia, EsoBiotec, Interius, and Orbital — essentially the entire first wave of credible in vivo pure-plays — now sit inside AbbVie, Lilly, AstraZeneca, Gilead, and BMS, where an autoimmune cell-therapy program is a rounding error against revenue in the tens of billions. When a credible pure-play nears the public market in this field, Big Pharma has consistently been there first (Candid's aborted Rallybio listing is the cleanest example). What's genuinely left to buy:

- Cartesian Therapeutics (Nasdaq: RNAC) — the cleanest direct optionality. Public on its ex-vivo Descartes-08 franchise (Phase 3 AURORA in gMG, topline Q1 2027), now adding in vivo via WestGene on a validated BCMA payload — a plasma-cell-directed angle distinct from the CD19 crowd. Two shots on goal in one indication; ~$150M non-dilutive financing from K2 HealthVentures guides runway through 2028.

- Sana Biotechnology (Nasdaq: SANA) — its fusogen-delivered, CD8-targeted CD19 candidate SG293 is a differentiated approach with clean primate depletion data, but mind the near-term reality: SG293's first clinical entry is in lymphoma (oncology), targeted for 2H 2026, with B-cell autoimmune disease a stated second step. Cash of ~$129M (including a ~$25M Mayo Clinic equity investment tied to its diabetes program) runs only into 2027, so financing risk is part of the thesis.

- Moderna (Nasdaq: MRNA) — direct organic exposure, but 007 is one line in a vast pipeline and won't move the stock alone for years.

- Otherwise, diluted exposure through ABBV, LLY, AZN, GILD, BMY — plus, for the antibody incumbent, Roche/Genentech trades OTC as RHHBY.

Meanwhile, the modality capital is fleeing is where the public pure-plays actually are: KYTX, CABA, AUTL (ex-vivo CAR-T); FATE (off-the-shelf iPSC CAR-T, well-funded into 2027); ARTV, NKTX (allogeneic NK); CGEM, JANX, INAB, and others (TCEs). If you want public-equity exposure to deep B-cell depletion working in patients today, it still runs disproportionately through the "old" modality — not the one generating the headlines.

Catalyst Calendar

The Bottom Line

Deep B-cell depletion works. Ex-vivo CD19 CAR-T proved it years ago, and Kyverna is a quarter or two from turning it into the first approved autoimmune cell therapy in history. The field's real question isn't whether the mechanism helps patients — it's whether it can be delivered without the cost, toxicity, and access constraints that currently confine it to the sickest, most specialist-adjacent patients. TCEs and allogeneic NK are live, de-risking answers today. In vivo CAR-T is the most ambitious answer, backed by more capital than the other three combined — and, for now, the only one with no autoimmune patient data to show for it. That's not a reason to dismiss it. It's the reason to watch Capstan's Phase 1 and Cartesian's 2027 readout far more closely than any headline about deal size.

Disclosure: I hold long positions in ARTV and INAB. Assume that gives me a financial interest in a favorable outcome with some of companies mentioned in this article and weigh this analysis accordingly. My positions may change at any time without notice. This article is for informational and educational purposes only. It does not constitute financial or investment advice. BiostockInfo receives no compensation from any company discussed. Always conduct your own due diligence before making investment decisions.